Is Your 401(k) Too Expensive & Complicated? We Believe There's a Better Way.

Discover Pooled Employer Plans (PEPs): A modern 401(k) solution for businesses that can reduce costs, simplify administration and lower your fiduciary risk.

See What’s Available in the Marketplace with a Complimentary Benchmark

As an Employer, You're Likely Facing One of These 401(k) Challenges:

You're not alone. These are the most common frustrations we hear from business owners every day.

High Fees

"My current 401(k) costs a fortune. Between admin fees, audit costs, and investment expenses, I'm losing thousands every year."

Admin Burden

"I spend hours every month on plan administration, compliance testing, and employee questions. I have a business to run!"

Fiduciary Risk

"I'm worried about my personal liability. What if I make a mistake? What if I get sued? The risk keeps me up at night."

Complexity

"I don't even know where to start. The regulations are confusing, and I don't have an HR department to handle this."

A Simple Solution to Your 401(k) Problems

Our Pooled Employer Plan is designed specifically for businesses like yours. We handle the complexity so you can focus on running your business.

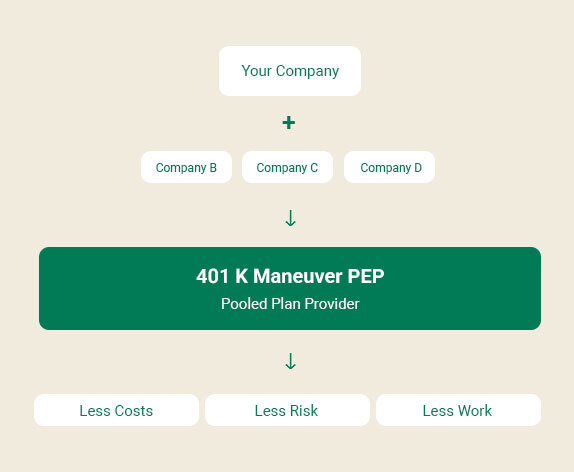

What is a Pooled Employer Plan (PEP)?

A Pooled Employer Plan (PEP) is a type of 401(k) retirement plan created by the SECURE Act 2.0 implemented in 2021 that allows multiple unrelated employers to participate in a single plan managed by a Pooled Plan Provider (PPP).

Think of it as a "401(k) co-op" where businesses pool their resources to access the same benefits, pricing, and professional management that large corporations enjoy.

- Lower Costs: Save 20-40% through economies of scale

- Less Work: We handle all administration and compliance

- Lower Risk: Transfer most fiduciary liability to us

- No Audit: Eliminate the costly annual plan audit

Getting Started is Simple

We've streamlined the process to get you up and running.

Get Your Benchmark

Fill out our simple form and we'll send you a personalized cost comparison showing exactly how much you can save with our PEP.

Customize Your Plan

We'll work with you to design a plan that fits your needs—matching contributions, vesting schedules, and investment options.

Launch & Relax

We handle the setup, employee enrollment, compliance, and ongoing management. You just upload payroll files, if needed — we do the rest.

Start Your Complimentary Benchmark to have it on file for one of your Investment Committee Meetings

The 401k Maneuver Difference

Not all PEPs are created equal. Here is what we believe sets us apart.

Active Management

We don't just "set it and forget it." Our team actively manages investments and rebalances quarterly based on market conditions.

Unlike passive index PEPs, we personalize risk tolerance for each participant—not just age-based target date funds.

Personalized Service

You get a dedicated advisor who knows your company by name—not a call center where you're just a number.

Boutique service, competitive pricing. We're big enough to offer economies of scale, small enough to care.

Transparent Pricing

No hidden fees. No surprises. We provide a clear, all-in cost structure from day one.

What you see is what you pay. We believe transparency builds trust.

Typical 401(k) vs. Our PEP: Who Does What?

See how much responsibility (and liability) you can transfer to us.

Typical 401(k)

- Overall Plan Compliance

- Document Compliance

- Mandatory Interim Reinstatements

- IRS Form 5500

- Plan Audits (estimated at 15K plus annually)

- All Annual & Required Notices

- Recordkeeping Emails Daily

- Eligibility Tracking & New Hire Tracking

- Respond To All Participant Inquiries

- Year End Testing

⚠️ You're responsible for all of this and more (and liable if something goes wrong)

Our 401(k) Maneuver PEP

- Upload Payroll Files*

- Year-end Data Collection*

That's it! We handle everything else.

*With one of our 473 payroll integrations, we can automate these services too.

Why Trust Us With Your 401(k)?

When your employees' retirement is on the line...

And YOUR personal liability is at stake...

We recommend you consider partners with serious skin in the game.

Industry Leaders Helping Support Your Financial Confidence.

Because we think we have the best fiduciaries in the industry:

Our Recordkeeper

Fiduciary Protection

"We stand behind our online plan tools and security."

Our PPP TPA 402(a) 3(16)

Legal Compliance

"Our goal is for your plan to meet every DOL requirement."

3(38) Investment Manager

Investment Management

"Professional portfolio management from a 130-year-old institution."

These aren't just your vendors; they are your fiduciary shield, your compliance team, and your investment lineup professionals.

Get Your Complimentary Benchmark

If nothing else, you can have it on file for Compliance Reasons. What do you have to lose?

Frequently Asked Questions

Get answers to the most common questions about Pooled Employer Plans.

A Pooled Employer Plan (PEP) is a type of 401(k) retirement plan created by the SECURE Act 2.0 implemented in 2021 that allows multiple unrelated employers to participate in a single plan. This pooled structure enables businesses to offer competitive retirement benefits while reducing costs, simplifying administration, and lowering fiduciary liability through shared economies of scale.

Unlike a traditional 401(k) where each employer sponsors their own plan, a PEP is sponsored by a Pooled Plan Provider (PPP) who assumes most fiduciary responsibilities. This means less administrative burden, lower costs through economies of scale, no annual audit requirements, and significantly reduced personal liability for business owners.

In a PEP, the Pooled Plan Provider (PPP) assumes most fiduciary responsibilities including investment selection, plan administration, and compliance. This dramatically reduces your personal liability compared to a traditional 401(k).

PEP costs vary by provider and plan size, but all plans are priced based on the average participant account balance. Many businesses save 20-40% compared to traditional 401(k) plans due to economies of scale, elimination of audit fees, and reduced administrative costs and burden. Get your complimentary benchmark to see exact savings for your company.

Most businesses with W-2 employees are eligible to join a PEP, regardless of industry or size. PEPs are particularly beneficial for companies with 10 or more employees. There are no commonality requirements—unrelated businesses from different industries can participate in the same PEP.