22 Financial Steps to Take before the End of the Year

Fourth quarter is here, which means there are important financial steps to take before the end of the year. Taking the time now to work through this checklist may help end the year strong and start 2021 with a bang.

We recommend printing off this list and scheduling time to work through it in the coming weeks. Your future self will thank you!

Keep reading for our top 22 financial steps to take before the end of the year.

#1 Review Year-to-Date Progress

Review your 2020 financial goals and assess your progress.

Take note of what you still need to accomplish by the end of the year. Don’t beat yourself up if you’re off target – it wasn’t an easy year for many of us. Do what you can to adjust your budget to meet these goals.

#2 Review Current Cash Flow

Fourth quarter is the perfect time to sit down and analyze your spending habits. If you’re spending more than you’re saving, see what you can cut and apply it toward your retirement savings or your emergency savings fund.

#3 Assess Your Debt

A smart financial step to take before the end of the year is to review your debt level and ensure you are on track to meet your debt-payoff goals for the year.

See where you can cut back on ancillary expenses and, instead, put that money toward paying off more debt before the year’s end. While you’re at it, go ahead and create your debt elimination goals for 2021.

#4 Fund an Emergency Savings Account

If there’s anything this year has taught us, it’s the importance of having an emergency fund to cover unexpected expenses.

If you have one already, are you on track to meet your savings goals by the end of the year? If not, see what expenses you can cut to put more into your rainy day fund.

If you don’t currently have one, make a plan to set aside some money before the end of the year. Even a few hundred dollars can make a big difference if your car breaks down or the dog gets sick.

#5 Pay Down Federal Student Loans

On Aug. 8, 2020, President Trump signed an executive order to continue to suspend loan payments, stop collections, and waive interest on ED-held student loans until December 31, 2020.

With interest rates on federal loans at 0%, see how much you can pay down on the principal before the end of the year.

#6 Review Credit Reports

According to the Insurance Information Institute (III), “In 2020 through April 10, the ITRC tracked 269 breaches that exposed 3.3 million records.”¹

With data breaches happening more often, there’s no better time to review your credit reports and confirm the information is accurate.

It’s a good practice to regularly check your credit reports, credit card statements, and bank accounts. In addition to monitoring your statements regularly, it may be wise to invest in an identity theft monitoring service.

[Related Read: Data Breaches: 6 Things Consumers Can Do to Protect Privacy and Online Data]

#7 Plan and Budget for 2021

Fourth quarter is the perfect time to review your 2020 budget and evaluate what can be done better. Then, create an improved budget for 2021. Be sure to budget your 401(k) and IRA account contributions. If possible, budget the maximum deposit amounts.

Also, if you know you’ll be making a big purchase in 2021, such as a house or car, plan for it now. Take the steps to improve your credit score and save for the down payment now.

#8 Review Your Retirement Plan or Get One In Place

This financial step to take before the end of the year is critical to your future. There’s no better time than now to sit down and review your retirement plan or get one in place.

Ask yourself:

- At what age do you want to retire?

- What do you want your retirement to look like?

- How much money will you need, not to just scrape by, but have a fulfilling, comfortable retirement?

From there, take a look at how much you’ve already saved and figure out what you need to do to get back on track. Or, if you don’t already have a plan, figure out how much you need to save each month to meet your retirement goals.

We can’t overemphasize how important this first step is.

Because, if you show up and work the plan, you may find that a lot of anxiety and stress over your retirement savings may subside. You are more likely to feel in control and on the way to achieving your goals.

Check out our retirement calculator to see how much you may need at retirement, and calculate how professional help may improve your future retirement income.

#9 Max Out Your 401(k) or IRA Contributions

This financial step to take before the end of the year is critical because it may affect your future retirement income…and help you take advantage of tax deductions.

The 2020 contribution limit for 401(k), 403(b), most 457 plans, and the federal Thrift Savings Plan is $19,500. If you are 50 and over, your contribution limit is $26,000.

For individual retirement accounts (IRA), the limit for 2020 is $6,000. If you are 50 and over your limit is $7,000.

Assess where you are and see if you can’t contribute a little bit more out of each paycheck now through the end of the year.

If you can’t max out the contribution limit for your 401(k), at least contribute your employer’s match contribution. It’s like getting free money!

Also, if you received a pay raise this year, increase the contribution toward your retirement savings.

[Related Read: New Retirement Plan Contribution Limits for 2020 ]

#10 Read Your Investment Statements

Opening and reviewing your statements helps you determine whether or not you’re on track to meet your financial goals.

Too often, when 401(k) or IRA statements come in the mail each month, people toss them in the trash. Others try to read them, but don’t understand what they’re reading.

It’s important you understand what is happening with your hard-earned money. Open your statements and read them.

If you don’t understand what you’re receiving, then reach out to an expert for help. Doing so may have a big impact on your overall returns and confidence about achieving your goals for retirement.

Watch the video below to see how to read a 401(k) statement.

#11 Rebalance Your 401(k)

An important financial step to take before the end of the year is to rebalance your 401(k).

If you aren’t rebalancing your account allocations, you may be missing out on earning more and keeping more of your hard-earned retirement savings.

Because unmanaged allocations may experience much larger losses in down markets and may miss the opportunity for growth during good markets.

We recommend rebalancing your account allocations every quarter, or four times a year. This way, you can make the appropriate changes in order to stay on course with your savings goals.

If you’d like more tips on how to have more income at retirement, check out our guide on How to Supercharge Your 401(k) Performance Today.

#12 Roll Over Old 401(k)s

If you have old 401(k)s from past employers just sitting, plan to consolidate or roll over before the end of the year.

Moving an old 401(k) may help reduce fees and create more investment flexibility with more choices that are offered outside of a 401(k).

We recommend you speak with a third-party expert before deciding whether you roll over an old 401(k) into your new employer’s retirement plan or into an IRA.

But first, check out our guide on the 5 irreversible and costly rollover mistakes.

#13 Cash In on Investment Losses

If you hold losing positions in the market, consider selling them to offset stock market gains.

The IRS allows you to claim up to $3,000 in capital losses per year or $1,500 for a married individual filing separately. If you exceed this, you may carry over unused losses into future years.

#14 Plan for Year-End Profit Sharing

If your company offers profit sharing and you know you’ll be getting paid out at the end of the year, now is the time to develop a plan for what you will do with the money.

Decide now if you will save it, pay off debt, or invest it into your retirement savings.

#15 Check Your Flexible Savings Account (FSA)

Many FSAs must be used by the end of the year. Do you have unspent money you need to use or you will lose it? If so, go ahead and make those doctor appointments you’ve been putting off.

Whether it’s getting a vision checkup, buying new glasses, or going to the doctor for a checkup, use your pretax dollars you put in your FSA account to get this done before you lose the money.

#16 Prepare for Healthcare Open Enrollment

The 2021 open enrollment period runs from Saturday, November 1, to Tuesday, December 15, 2020. Coverage Starts January 1, 2021.

Be prepared with updated lists of doctors and prescriptions before enrollment begins so you aren’t scrambling during the holiday season to gather key information needed to enroll.

#17 Review Insurance Policies

Fourth quarter is a good time to evaluate whether your home and auto insurance coverage still makes sense for your needs and if you can lower your rates to save money.

If your home has increased in value due to updates or additions, make sure to change the replacement value amount to reflect the new value increase.

For auto insurance, if you have any prior tickets or accidents that have fallen off this year, be proactive and get a new quote to see if you can save money.

#18 Review Life Insurance Policies

Have you stopped smoking or lost weight in 2020? If so, review your life insurance policies and see if these life changes may help you get a better quote to save money.

Also, look for gaps in your policies. If you recently got married or had a baby, it’s important to make sure the payout amount covers your spouse or child should something happen to you.

#19 Update Beneficiaries

When is the last time you reviewed your accounts and made sure your beneficiary information is accurate? If it’s been a while, now is the time to make the necessary updates.

This means checking the beneficiaries for your life insurance policies, investment accounts, 401(k)s, IRAs, and checking and savings accounts.

#20 Review Estimated Taxes

If you are self-employed, have you made all your quarterly tax payments this year? Will you purchase equipment or other investments by year-end that can offset profits this year?

We recommend you talk with your accountant to make sure you’re on track with estimated taxes for 2020, and ensure you won’t get stuck with a large tax bill come spring.

#21 Review and Update Tax Exemptions

This fourth quarter financial tip can make a big difference come tax time next year. Take the time now to review your tax exemptions to see if you’re paying too much in taxes or not enough.

If you’re not paying enough, making the change now may prevent you from owing the IRS for underpayment.

If you’re overpaying, you’ll be able to keep more each paycheck or apply the additional amount to your 401(k) or IRA contributions.

If you receive bonuses or large sums of money toward the end of the year, taking a look at your exemption now may also help keep you from owing the IRS come tax time.

#22 Seek Third-Party Help

This financial step to take before the end of the year may have a big impact on your overall finances, tax situation, and retirement future.

It doesn’t matter how far away or close to retirement you are or how much money you’ve saved.

Speaking to an advisor now can help you get on track and stay on track with your financial goals.

Think about it this way: Even the best athletes in the world have coaches! Find a coach to help you be successful with your money!

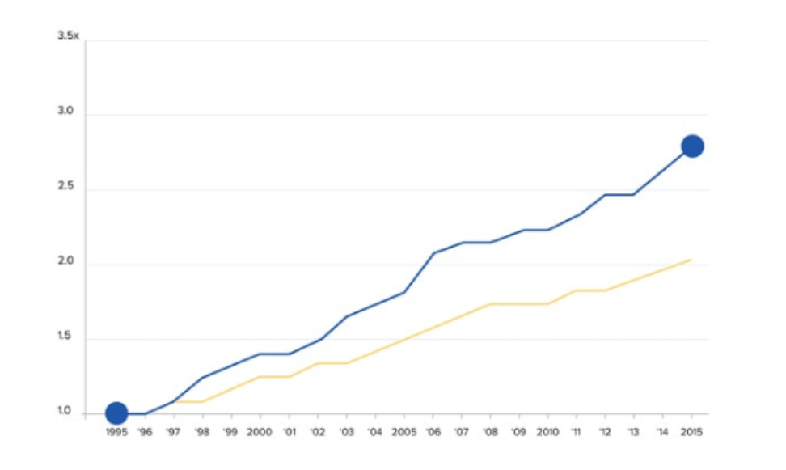

A May 2014 study conducted over a 6-year period compared those who had help with managing their 401(k) and those who did not. The study revealed…

“On average, the median annual returns for participants in the study who got Help were more than 3% (332 basis points, net of fees) higher than people who didn’t get Help.”²

From the graph above, you can see getting expert help with your 401(k) savings can be beneficial to life at retirement.

Have questions or concerns about your 401(k) performance? Click below to book a complimentary 15-minute 401(k) Strategy Session with one of our advisors today.

Book a 401(k) Strategy Session

Sources:

- https://www.iii.org/fact-statistic/facts-statistics-identity-theft-and-cybercrime

- AON Hewitt “Help in Defined Contribution Plans: 2006 through 2012” Published May 2014