3 Strategies That May Maximize Your 401(k) in Third Quarter 2020

While 2020 has left many investors concerned about their retirement accounts, there are things you can do today to ensure you stay on track to meet your retirement goals. Keep reading for 3 strategies that may maximize your 401(k) in third quarter.

#1 Keep Contributing to Your 401(k)…and Don’t Panic

2020 has been a bumpy ride for the stock market, which has made some 401(k) investors nervous about their retirement future.

Couple this with the uncertainty brought about by the lockdown, and it’s understandable investors are nervous about what they do with their hard-earned money.

While it’s important to focus on the near future and be mindful of where we allocate each paycheck, it’s equally important to not to forget about our future.

Saving for retirement should be put on the back burner.

If you’ve been wondering, Should I pause or cut back on 401(k) contributions? the answer is No.

One day you will need all the retirement money you can save.

With pensions all but gone and the future of social security uncertain, that leaves your personal savings to carry the heavy load come retirement.

If you are able, continue contributing regularly to your 401(k).

You should contribute the maximum amount that your company will match.

The employer-matched money effectively doubles your contribution and might help you achieve your retirement income goals. Don’t miss out on the gift of money!

If you can, increase the amount you’re contributing each pay period to help maximize your 401(k) in third quarter.

Even putting 1% more of your salary into your 401(k) each paycheck may make a big difference over time.

The reason is dollar-cost averaging–an investment technique that you’re already doing when you invest in a 401(k).

Dollar-cost averaging is a strategy that allows an investor to buy a fixed-dollar price of an investment at regular intervals.

The purchases occur regardless of the asset’s price.

With dollar-cost averaging, you need not worry about timing the market.

In fact, with dollar-cost averaging, market volatility can be your friend. And, if managed properly, it can help you build wealth and enter retirement with more income.

Here’s how dollar-cost averaging works…

Let’s say you bought $1,000 worth of stock each month in ABC fund over the course of 4 months.

- Month 1, the stock price is at $31 a share, so you buy 32 shares.

- Month 2, shares drops to $26 a share, so you buy 38 shares.

- Month 3, shares drop to $18 a share, and you buy 55 shares.

- Month 4, the price goes up to $33 a share, and you buy 30 shares.

By the end of month 4, you’ve purchased 155 shares at $4,000, with the average price being $25.80.

Based on the current price of shares, your investment of $4,000 has turned into $5,115.

Had you purchased 155 shares on month 1, you would have purchased them at $31 a share, and only own 129 shares.

Understanding how dollar-cost averaging works is what helps informed investors to not panic when the market takes a downturn.

They understand the power of this strategy (and #2 below) and know they may gain more shares when the market takes a dip and, thus, accumulate more for retirement.

Remember, short-term pain may equal long-term gain!

#2 Rebalance Your 401(k)

Another strategy that may maximize your 401(k) in third quarter is to rebalance.

401(k) investors often suffer from poor account performance and less than optimal results because they fail to rebalance.

Rebalancing is one of the best ways to ensure your 401(k) is on track and your contributions are invested according to your asset allocation target.

Over time, the performance of certain funds in your account may cause your asset allocation to look different from your original plan…and may expose you to more risk than you’d like.

Adjusting your investment allocations back to their original targets throughout the year helps you stay in line with your risk tolerance and timeline for retirement.

Let’s say your original asset allocation target was to have 50% stocks and 50% bonds.

If your selected stocks performed well over a 10-year period, your 50/50 plan may have increased the weighting to 72% stocks/28% bonds.

In this case, in order to return to your initial target 50/50 weighting and decrease your risk, you would need to sell off some of the stocks and purchase more bonds.

Or, in other words, you would need to rebalance your portfolio.

Failing to regularly rebalance has the potential to do real harm over time to your retirement account performance.

In down or volatile markets, rebalancing your 401(k) helps you stay within your risk level and protect against potential losses.

On the flip side, rebalancing may help you take advantage of opportunities for growth during good markets.

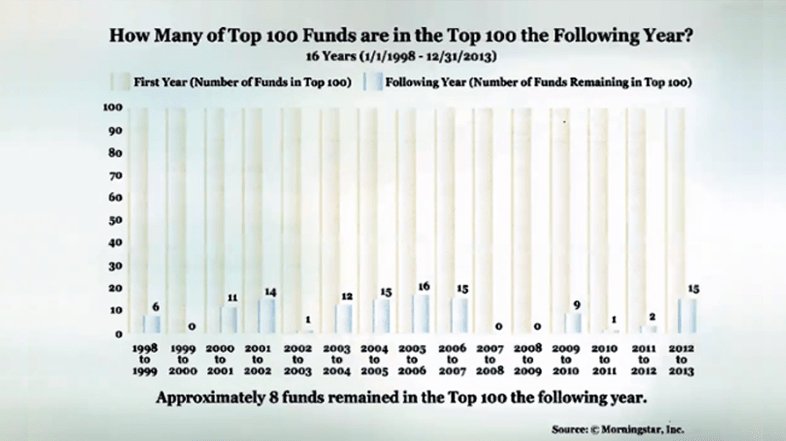

Morningstar conducted a study that monitored the top 100 best-performing mutual funds between January 1, 1998, and December 31, 2013.

This study revealed that, in any given year of top best-performing 100 mutual funds in any of those years, in the next year, about half of the time, only 8 out of 100 remained in the top 100 the very next year.¹

This study illustrates it’s not wise to use a buy-and-hold strategy, and why quarterly rebalancing your account is important.

If rebalancing has the potential to help maximize 401(k) account performance, why do 80% of 401(k) investors fail to rebalance their accounts?²

It could be because many people are told to follow a buy-and-hold strategy with their 401(k) accounts.

Some may believe their employer rebalances their accounts for them, which they do not.

Some may not know rebalancing is an option or understand how it may boost 401(k) returns. Others may find it too difficult.

Whatever the case, setting up your 401(k), contributing to it each pay period, and “letting it do its thing” may cause you to potentially miss out on earning more and keeping more of your hard-earned retirement savings.

#3 Get Professionally Managed Help

An underutilized strategy you can do to potentially maximize your 401(k) in third quarter is to seek professional help.

Although you might have basic investment knowledge, utilizing an expert to do the in-depth market research could change the performance of your account from good to great.

In fact, a Morningstar report shows that participants that received expert guidance had as much as 40% more income during retirement versus those who received no help at all.³

Another study revealed rebalancing your retirement account each quarter, with professional help, may improve account performance by 3%+ annually.⁴

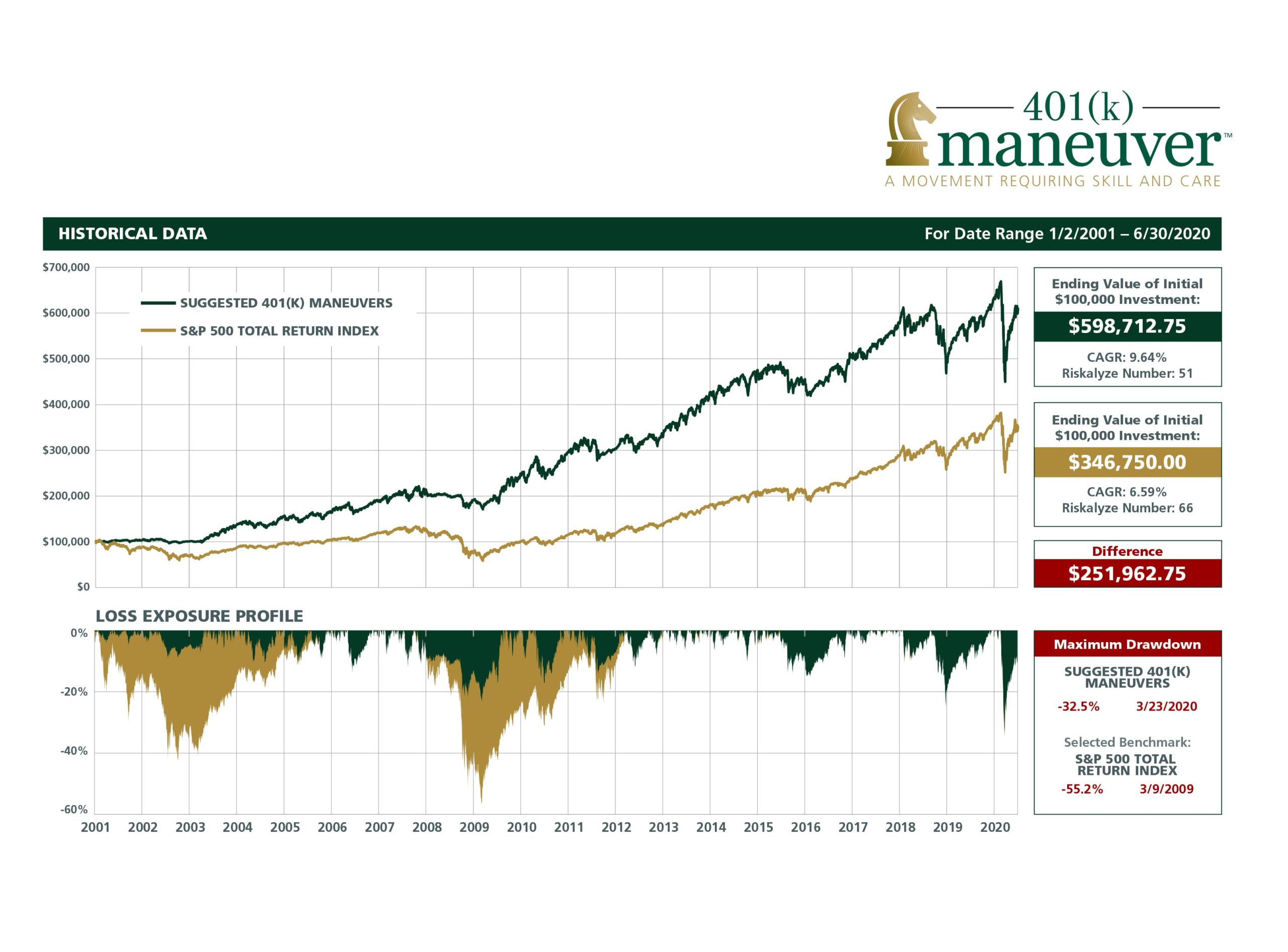

Take a look at how professional help managing your 401(k) may help your account balance.

As you can see from the chart above, a 3%+ annual difference can add up to a lot of money.

This is why we recommend turning to an expert for help with rebalancing your 401(k) account.

Even though your 401(k) is employer-sponsored, it does not mean your employer is making changes on your behalf. It’s your account. It’s your money. And it’s your job to look out for your future.

If you’re hesitant to reach out for advice because you think your account balance isn’t big enough, or you think you’re too close to retirement to get help, don’t let that stop you!

401(k) Maneuver provides professional account management to help you grow and protect your 401(k).

Our goal is to increase your account performance over time, manage downside risk to minimize losses, and reduce fees that harm your account performance.

There are no time-consuming in-person meetings and nothing new to learn, and you don’t have to move your account.

Simply connect your account to our secure platform, and we regularly rebalance your account for you.

If you have questions about your 401(k) or if you need help, we’re here for you. Click below to book a complimentary 15-minute 401(k) Strategy Session with one of our advisors.

Book a 401(k) Strategy Session

Sources:

- Morningstar, 2013

- “Over 90% of Americans make this 401(k) Mistake.” Mauri Backman, The Motley Fool.

- The Impact of Expert Guidance on Participant Savings and Investment Behaviors. David Blanchett, Morningstar Investment Management Group, 2014.

- https://aon.mediaroom.com/news-releases?item=136959