401(k) Maximization Strategies in Your 30s

There is no better time to put a serious dent in your 401(k) savings than in your 30s.

Sure, some of you may have young families to feed or you aren’t at peak earning potential yet, but the amount you save now provides a golden opportunity to accumulate a serious amount of retirement wealth.

Keep reading for 5 401(k) maximization strategies if you’re in your 30s.

#1 Don’t Wait to Create a Retirement Plan

Think you’re TOO young to have a retirement plan? Think again.

Having a plan guides you, helps you stay on track, and ensures you’ve properly planned for retirement.

We’re guessing the last thing you want is to retire with a $250,000 401(k) balance when you were used to making $65,000 per year at your job prior to retirement.

Sure, you have quite a few years ahead of you to save more, but is this where you want to end up at retirement age? Probably not because those funds aren’t going to give you much to live on.

The first step in creating a plan is to know when you plan to retire, how much you want to have saved, and then take a good hard look at where you are now.

According to Vanguard’s How America Saves 2021 report, the average 401(k) balance for ages 25-34 is $33,272 and the median balance is $13,265. For ages 35 – 44, the average 401(k) balance is $86,582 and the median balance is $32,664.¹

By age 30, Fidelity recommends having the equivalent of 1 year’s salary saved in your 401(k).² That means if you make $47,000, your balance should be $47,000 by the time you reach 30.

How do your 401(k) savings measure up?

If you are behind in how much you need saved to date, don’t sweat it – you have quite a few years ahead of you to save.

Plus, with a plan in place, you should go much further now than you did without one. Here’s what you can do today to turn things around: Sit down and create a plan for retirement. If you created a plan years ago, but haven’t followed it, then hit the reset button and start planning.

At what age do you want to retire?

What type of lifestyle do you want?

How much money will you need, not to just scrape by, but have a fulfilling, comfortable retirement?

This is what you need to figure out. Write it down.

Once you have this info, take a look at the amount currently in your 401(k) and figure out how much you need to start saving to get on track.

If you need help planning, reach out to an advisor and get advice sooner rather than later.

#2 Increase Your 401(k) Contributions

Now that you know how much you need to save each year to reach your retirement savings goals, it’s time to increase your contributions.

The 2022 annual contribution limit for 401(k), 403(b), most 457 plans, and the federal Thrift Savings Plan are $20,500 – up from $19,500.

The ideal scenario would be to max out your yearly contributions, but that isn’t always feasible for investors in their 30s. For many, they aren’t at peak earning potential. Others have young families.

Whatever your situation, do what you can this year to increase contributions. What may not seem like much – say 3 or 5% more – may have more of an impact on your 401(k) savings than you think.

#3 Make Sure You Get the Company Match

A big help in increasing your 401(k) balance is to make sure you contribute at least the minimum of what your company will match because it’s basically FREE money to you.

Depending on what your company matches, it may double the amount of what you’re already saving.

Let’s say your company matches 100% up to 6% of your pay. With a $55,000 salary, you could put in 6% or $3,300 for the year, and the company would match this at 100%.

That’s an extra $3,300 per year of free money – money that’s yours to keep, providing you’re fully vested. Each employer has its own requirements for vesting. Should you leave your job before you’re fully vested, depending on the vesting schedule, you will have to return part or all of the money your company matched.

This additional $3,300 doesn’t include the compounding of investment returns or your earnings. This is just about the additional money you could be saving with your company match.

[Related Read: 4 Ways to Potentially Maximize Your 401(k) Company Match]

#4 Regularly Make Changes to Your Investments

Why is it that so many people who are putting away a substantial amount of money for the future don’t really pay that much attention to what they’ve invested in, or how those funds are performing?

Well, with the rise in popularity in recent years of target date funds (i.e., 2020, 2030, 2040 funds), also called lifestyle funds or retirement date funds, there’s a growing trend to set up a 401(k), fund it, but not make regular changes.

Following the popular “buy-and-hold” strategy with 401(k) accounts doesn’t take into consideration changing market conditions, nor does it take into account your level of risk tolerance or your unique retirement goals.

The stocks or mutual fund you initially chose to help you meet your retirement goals may no longer be the best investment choice for you now.

This is why we encourage 401(k) investors to rebalance their account allocations.

They know that unmanaged allocations may experience much larger losses in down markets and may miss the opportunity for growth during good markets.

A study conducted by Morningstar shows the importance of regularly rebalancing. The study monitored the top 100 best-performing mutual funds between January 1, 1998, and December 31, 2013. It revealed that, in any given year of top best-performing 100 mutual funds in any of those years, in the next year, about half of the time, 8 out of 100 remained in the top 100 the very next year.³

If you aren’t rebalancing your account allocations, you may be missing out on earning more and keeping more of your hard-earned retirement savings. Because unmanaged allocations may experience much larger losses in down markets and may miss the opportunity for growth during good markets.

Check out the video below to learn more about how rebalancing may help you safeguard your retirement savings.

#5 Get Help Sooner Rather Than Later

If you want to jumpstart your 401(k) savings in your 30s, don’t wait to seek expert advice.

In fact, doing so sooner rather than later may have a significant impact on your retirement lifestyle. Not to mention, it will reduce stress and worry later in life as you near retirement.

A recent Morningstar report shows that participants who received expert guidance had as much as 40% more income during retirement versus those who received no Help at all.⁴

Check out our retirement calculator to see how professional help may improve your future retirement income.

Even if you have a couple thousand dollars saved, it’s worth finding an advisor who can help guide you.

Say HELLO to the Future of Retirement Saving

Want to grow your 401(k), but don’t want to drive to an appointment, meet an advisor in person, or spend hours preparing for a meeting?

Welcome to 401(k) Maneuver. We help employees just like you grow and protect their 401(k) accounts through independent, personalized professional account management.

And we do it without in-person meetings. Everything we do is virtual.

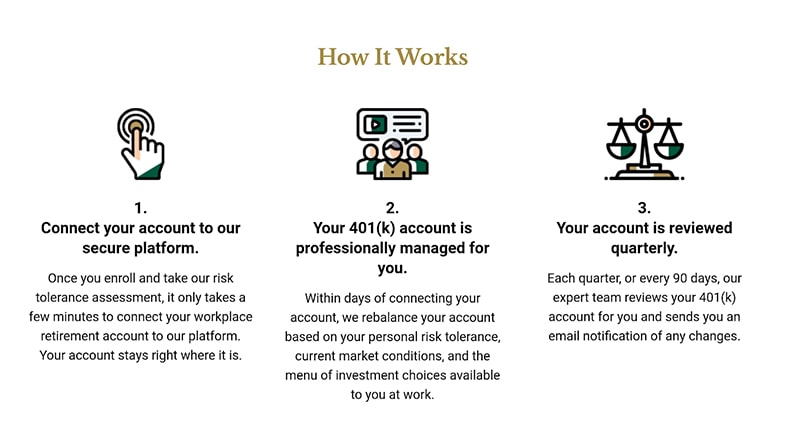

Our virtual service allows you to keep your 401(k) right where it is while we review and rebalance your account based on your risk tolerance and current market conditions.

All you need to do is to connect your account to our secure platform, and we manage your account for you.

There’s no need to move your account – you can keep it right where it is.

As a fiduciary, we are bound by law to put your interests first, and we do not receive commissions on transactions.

Don’t wait to start accumulating your retirement savings. Book a complimentary 15-minute 401(k) Strategy Session with one of our advisors today.

Book a 401(k) Strategy Session

Sources:

- https://institutional.vanguard.com/content/dam/inst/vanguard-has/insights-pdfs/21_CIR_HAS21_HAS_FSreport.pdf

- https://www.bankrate.com/retirement/average-401k-balance-by-age/

- Morningstar, 2013

- Morningstar, 2013