#1 401(k) Mistake That May Cost More Income at Retirement

As an investor, the only thing guaranteed is changing market conditions.

So why would you invest your hard-earned savings into your 401(k) or other workplace retirement account and then forget about it?

After all, the investments you initially chose to help you meet your retirement goals–whether that was 20 years ago or 2 years ago–may no longer be the best alternatives for you now (especially with changing market conditions).

In the past, traditional investors have been told to follow a “buy and hold” strategy with 401(k) or other workplace retirement accounts. After all, retirement saving is a long-term game.

This buy and hold philosophy is the #1 mistake 401(k) account holders make…and a potentially costly one that may be doing more harm than good.

If you aren’t regularly rebalancing your account allocations, then keep reading for more information on what the heck rebalancing is, why it’s critical to your future retirement income, and what to do moving forward .

How Rebalancing Works

Rebalancing is the process of realigning the weightings of the assets (your investments) in the portfolio. This can involve periodically buying and/or selling assets in the portfolio in order to maintain the initial desired level of asset allocation.

Maintaining an even distribution of assets–such as 50% stocks and 50% bonds–is also a key objective.

Therefore, a rebalancing of the portfolio may need to take place from time to time throughout each year.

Let’s look at this example…

If your original asset allocation target was to have 50% stocks and 50% bonds, and the stocks performed well over a given period of time, then this may have increased the weighting of stocks to 60% or 70%–reducing the weighting of the bonds. In this case, in order to return to your initial target 50/50 weighting, you would need to sell off some of the stocks and purchase more bonds.

Rebalancing Is NOT the Same As Account Allocation

It’s important here to note that rebalancing is not the same thing as asset allocation, though the two can be related.

Account allocation is a type of investment strategy that attempts to balance risk versus reward by adjusting the percentage of each asset in a portfolio, based on investment time frame, tolerance to risk, and overall goals and objectives.

In order to help investors grow their account, while at the same time keeping risk in check, an asset allocation strategy is often put in place.

Why It’s Vital You Rebalance Your 401(k)

Few people rebalance their 401(k) account, and even those who do, fail to manage risk through proper asset allocation. Rebalancing only the percentages of current holdings does not consider current market and economic conditions.

This often results in more significant losses during bad markets.

So, if you aren’t rebalancing your account allocations, you may be missing out on earning more and keeping more of your hard-earned retirement savings.

Unmanaged allocations may experience much larger losses in down markets and may miss the opportunity for growth during good markets.

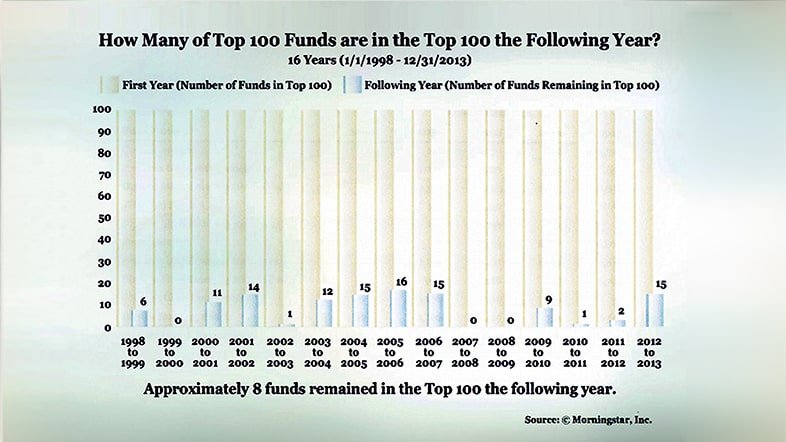

Morningstar conducted a study that monitored the top 100 best-performing mutual funds between January 1, 1998, and December 31, 2013.

This study revealed that, in any given year of top best-performing 100 mutual funds in any of those years, in the next year, about half of the time, 8 out of 100 remained in the top 100 the very next year!

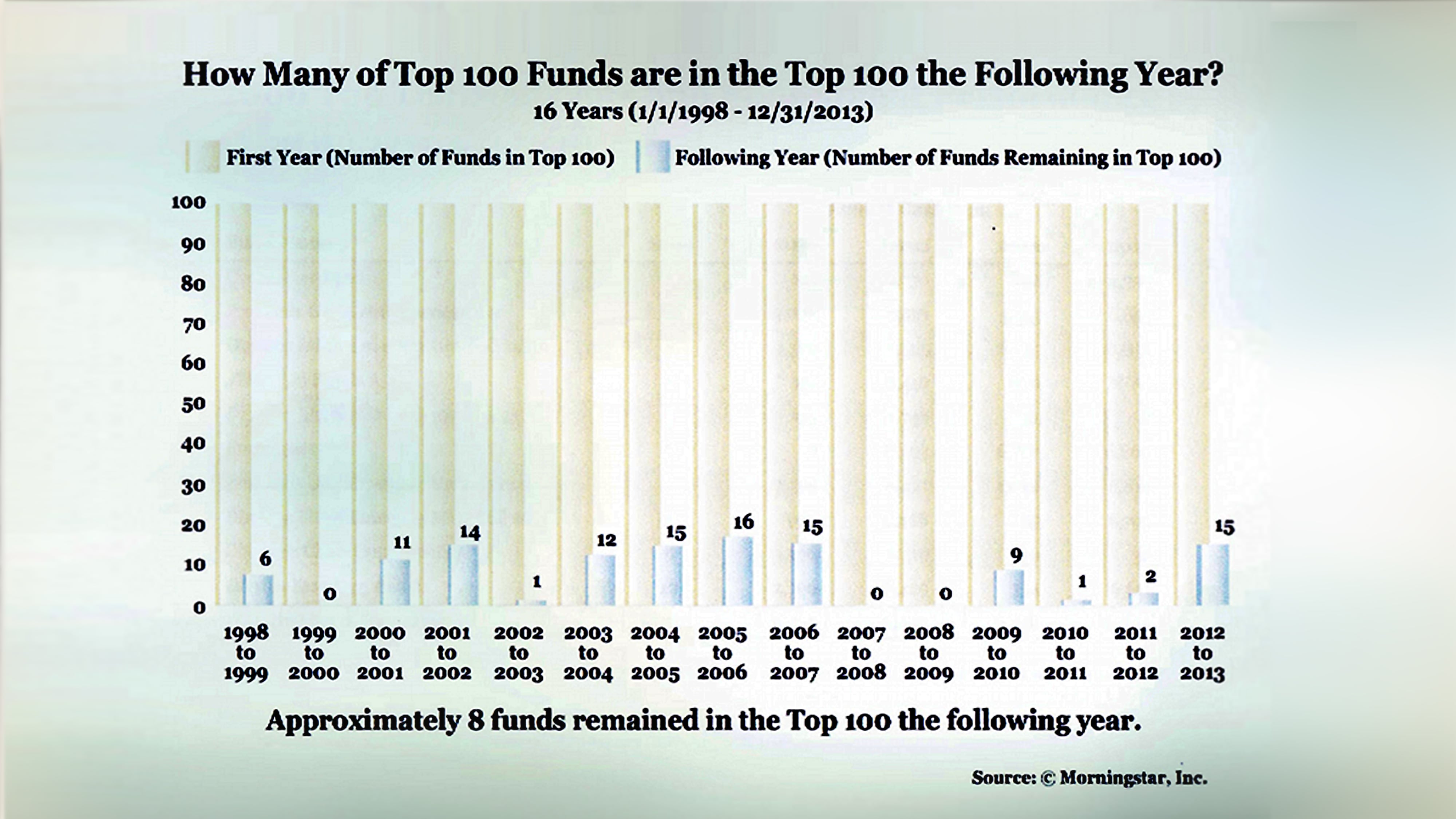

Take a look at the chart below. This 18 year chart illustrates the potential better performance when properly rebalancing your 401(k) or other workplace retirement account on a quarterly basis with third-party help.

The gold line below represents the hypothetical account allocations using the “buy and hold” philosophy.

The green line represents the potential increase in account performance using third-party advice and proper quarterly rebalancing.

To the right of the graph are the ending values of the initial investments of $100,000 shown in the green and gold lines.

The red box to the right shows the potential differences of assets in the account.

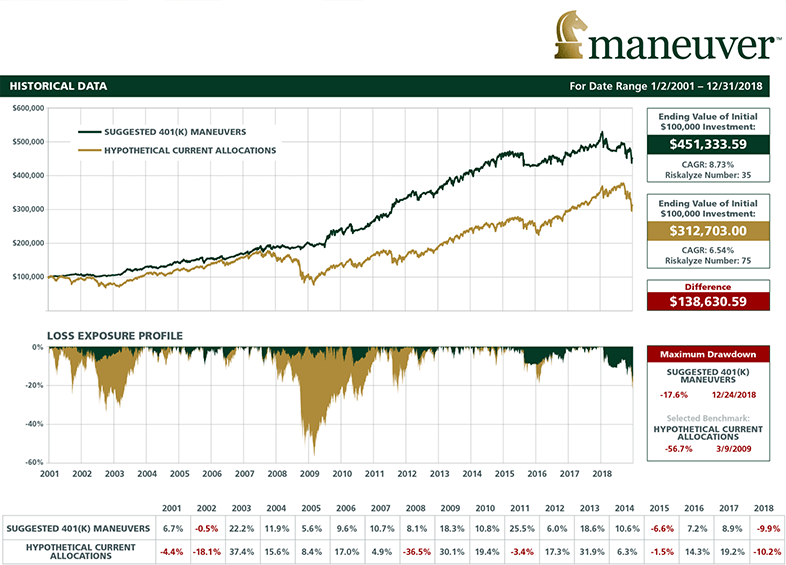

Let’s dive a little deeper, and look at the Loss Exposure Profile. This graph shows how each account would have performed during down markets.

It’s clear that unmanaged allocations experienced much larger losses during these periods.

To the right of the profile is the red box titled Maximum Drawdown. This represents the maximum percentage of loss experienced by each of these accounts–and the day it actually happened.

This shows the difference that third-party advice and proper quarterly rebalancing may have.

Remember…

It’s not only important what you earn in return.

It’s also important what you keep that may have a big impact on future

account value and your ability to reach your retirement goals.

Click here for more expert advice. Download our guide that shows you how to Supercharge Your 401(k) performance.

401(k) Rebalancing Recommendations

At 401(k) Maneuver™, we recommend rebalancing your account allocations every quarter, or four times a year.

Rebalancing can take time and effort. This is why, throughout the years, many employer-sponsored retirement plans have touted the benefits of Life Cycle, or target date funds (2020, 2030, 2040 funds).

In fact, many companies resort to these types of funds as the “default” option simply based on a person’s retirement date.

But just because something is easy, it doesn’t mean that it’s the right option for everyone.

In fact, using a “standardized” portfolio allocation can actually be detrimental to investors. Individual investors should ideally have customized solutions that are based on their specific goals and risk tolerance.

Simply rebalancing to your original target percentages isn’t good enough.

Click here to download our guide 5 Ways Target Date Funds Fail to Live Up to Their Promise.

Sources

The Impact of Expert Guidance on Participant Savings and Investment Behaviors•: David Blanchett, Morningstar Investment Management Group, 2014.

- BNY Melon Retirement Report “Time To Get Personal” 2015

- Over 90% of Americans make this 401(k) mistake by Maurie Backman for The Motley Fool

- http: / / aon.mediaroom.com/ news-releases?item=l36959