Can I Boost My 401(k) Savings without Contributing More?

Maxing out yearly 401(k) contribution limits is the best way to ensure investors boost 401(k) savings and have enough money to retire comfortably.

But, this isn’t always feasible.

Consistently contributing as much as you can and meeting the company match may also make a huge difference in your retirement lifestyle.

There is one thing you can do today that may potentially have a significant impact on your 401(k) savings: seeking third-party advice.

In the age of low-cost robo advisors and financial DIY tools you can access on your smartphone, many 401(k) investors overlook the importance and value of third-party expert advice.

Although you might have basic investment knowledge, utilizing an expert to make the moves that require skill and care may change the performance of your account from good to great.

And potentially boost retirement savings.

In fact, studies continue to show that working with a financial advisor may increase your 401(k) savings and greatly impact the type of retirement lifestyle you can afford.

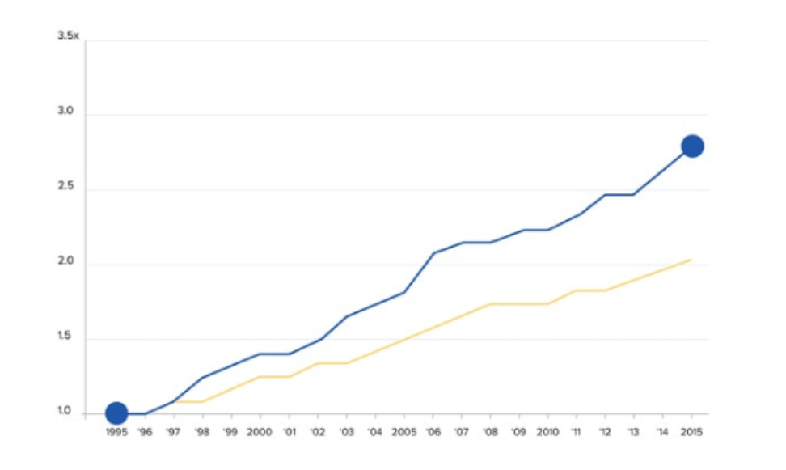

3% Potential Higher Annual Return

From 2006 to 2012, Aon Hewitt and Financial Engines conducted a study where they compared the returns of investors who sought help in the form of online sources or managed accounts to those who managed their 401(k)s themselves.

The study, which examined the 401(k) investing behavior of 723,000 workers at 14 large US employers, concluded that people who got professional help earned higher median annual returns than those who invested alone.

In fact, “Participants who got Help received, on average, 3.32% (net of fees) more in return annually” than those who managed their own portfolios.¹

“If two participants—one using Help and one not using Help—both invest $10,000 at age 45, assuming both participants receive the median returns identified in the report, the Help participant could have 79 percent more wealth at age 65 ($58,700) than the Non-Help participant ($32,800).”²

In a 2019 study titled Advisor’s Alpha, The Vanguard Fund Group, Inc., also reported a 3% average increase in the value of portfolios of clients who work with a good financial advisor.³

The study does point out that this return depends on the client’s situation and it will vary from year to year.

“The majority of this increase will come during periods of heightened greed and fear in the markets when advisors can step in and help their clients maintain an even keel and keep their long-term objectives in sight.”⁴

Morningstar’s David Blanchet, Head of Retirement, CFP, CFA, published a 2014 study titled, The Impact of Expert Guidance on Participant Savings and Investment Behaviors.

Expert guidance provides investors with additional investment benefits and savings, “such as increased savings levels and diversified investment allocation, which may lead to greater potential returns and more income in retirement, even after accounting for potential fees.”⁶

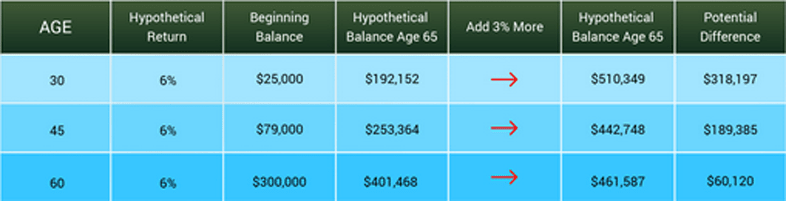

Take a look below to see the potential of adding 3% more to your 401(k) over time.

What impact would a potential 40% increase in 401(k) savings have on your retirement future?

Would it mean you could travel more and not have to take on a part-time job or side hustle?

Would you be less worried about running out of money?

Would you be able to spend more time with family and friends or pursuing hobbies and crossing off items on your bucket list?

We’re betting the answer is yes.

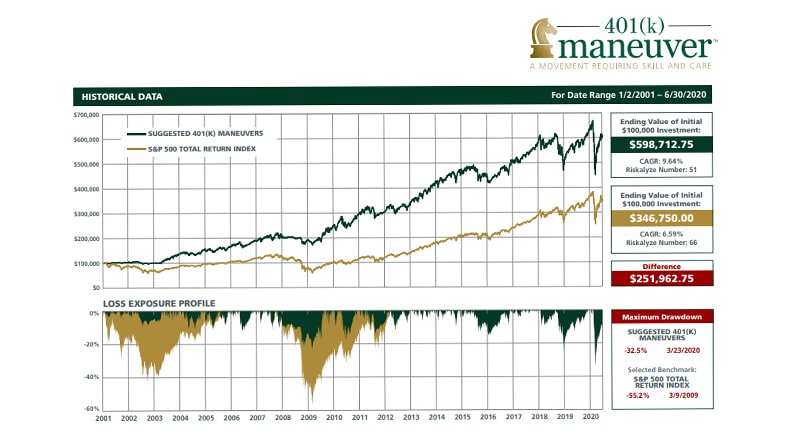

With 401(k) Maneuver, you can see the potential advantage of having professional account management to help manage your 401(k) account in the example below.

Our goal is to increase your account performance over time, manage downside risk to minimize losses, and reduce fees that harm your account performance.

Check out our retirement calculator to see how professional account management may improve your 401(k) account performance.

Third-Party Experts: More Than a Money Manager

One of the biggest reasons people’s 401(k) investments underperform in good or bad markets is due to human emotion.

The fear of losing money should the market drop.

The sense of being powerless.

The dread of retiring without adequate savings.

The anxiety over what happened in 2008, and the fear of something similar happening again.

No one wants to lose money, but making investment decisions based on emotions may negatively impact your retirement savings.

In addition to managing your investments, good financial advisors act as a behavioral coach.

They help you wade through rough markets and make decisions based on data and trends, not fear and worry.

With expert advice, you’ll make better financial decisions. And, thus, potentially earn more to boost 401(k) savings.

Before you reach out for help, check out our guide on how to understand The Different Types of Licenses Financial Advisors Have and What They Mean to You.

If you have questions about your 401(k) or if you need help, we’re here for you. Click below to book a complimentary 15-minute 401(k) Strategy Session with one of our advisors.

Book a 401(k) Strategy Session

Sources:

- https://www.edelmanfinancialengines.com/press/2014/financial-engines-aon-hewitt-find-401k-participants-who-use-professional-help-are-better-off

- https://www.edelmanfinancialengines.com/press/2014/financial-engines-aon-hewitt-find-401k-participants-who-use-professional-help-are-better-off

- https://www.investopedia.com/articles/personal-finance/102616/how-much-can-advisor-help-your-returns-how-about-3-worth.asp

- https://www.edelmanfinancialengines.com/press/2014/financial-engines-aon-hewitt-find-401k-participants-who-use-professional-help-are-better-off

- David Blanchet, Head of Retirement, CFP, CFA, Morningstar 2014, “The Impact of Expert Guidance on Participant Savings and Investment Behaviors”

- David Blanchet, Head of Retirement, CFP, CFA, Morningstar 2014, “The Impact of Expert Guidance on Participant Savings and Investment Behaviors”