How Rebalancing May Boost 401(k) Returns in 2020

If you’re looking for a way to boost 401(k) returns in 2020, rebalancing may help you do just that.

Rebalancing is the process of realigning the weightings of the assets (your investments) in the portfolio to stay in line with your risk tolerance and your timeline for retirement.

This can involve periodically buying and/or selling assets in the portfolio in order to maintain the initial desired level of asset allocation.

Maintaining an even distribution of assets–such as 50% stocks and 50% bonds–is also a key objective.

Let’s say your original asset allocation target was to have 50% stocks and 50% bonds.

If your selected stocks performed well over a given period of time, then this may have increased the weighting of stocks to 60% or 70%–reducing the weighting of the bonds.

In this case, in order to return to your initial target 50/50 weighting, you would need to sell off some of the stocks and purchase more bonds. In other words, you would need to rebalance your portfolio.

Why Rebalance Your 401(k)

When it comes to saving, it’s not only important what you earn in return.

It’s also important what you keep that may have a big impact on future account value and your ability to reach your retirement goals.

This is why rebalancing is so important and may help boost 401(k) returns in 2020.

In fact, not regularly rebalancing has the potential to do real harm over time to your retirement account performance.

On the flip side, rebalancing may help you take advantage of opportunities for growth during good markets.

If rebalancing is so important, why do 80% of investors sign up for a 401(k) and never touch it again?¹

Some don’t know rebalancing is an option or understand how it may boost 401(k) returns.

Others have been told to follow a “buy and hold” strategy with their 401(k) accounts.

Whatever the case, setting up your 401(k), contributing to it each pay period, and letting it do its thing may cause you to potentially miss out on earning more and keeping more of your hard-earned retirement savings.

Potentially Boost 401(k) Returns by 3%

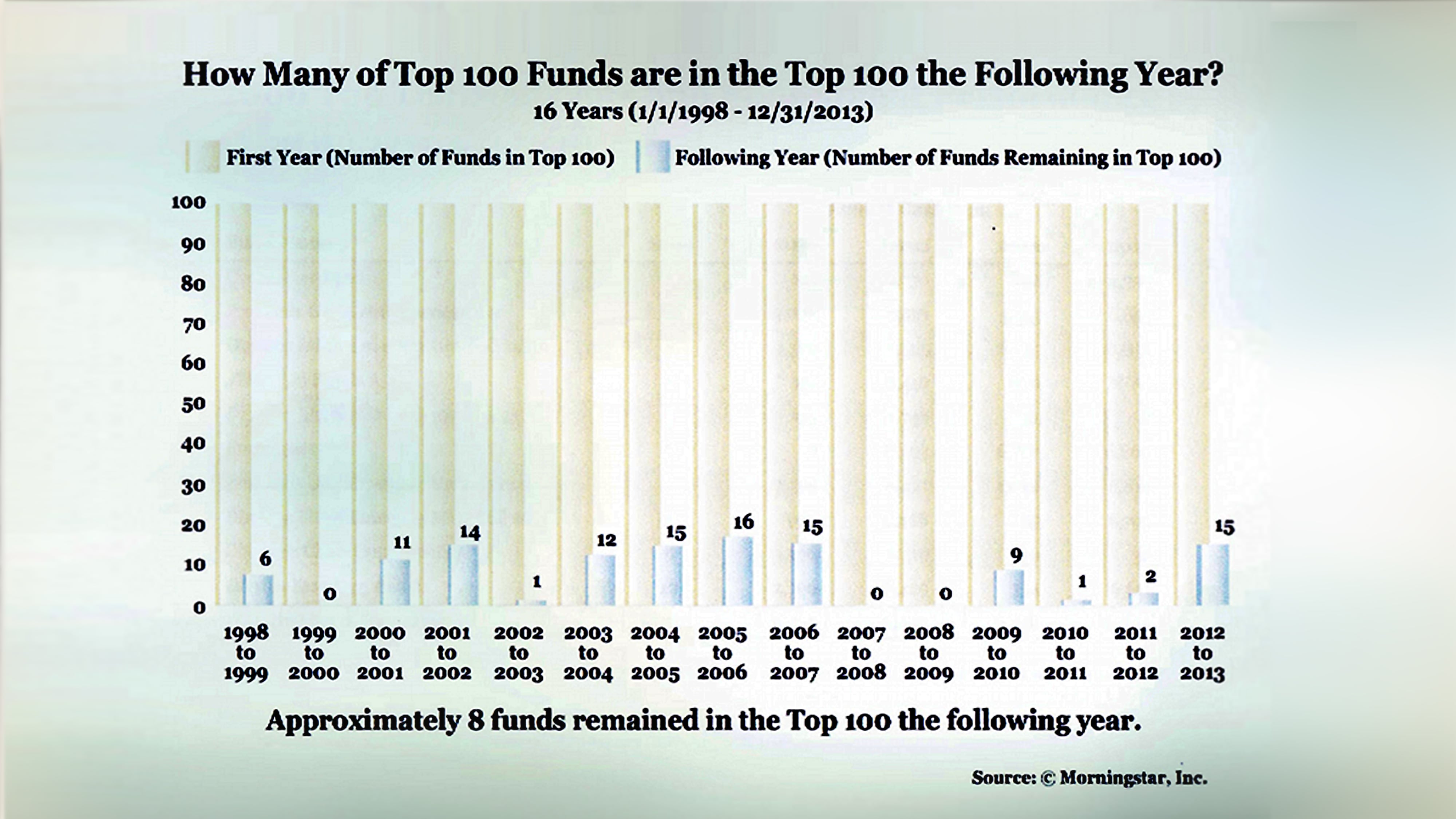

Morningstar conducted a study that monitored the top 100 best-performing mutual funds between January 1, 1998, and December 31, 2013.

This study revealed that, in any given year of top best-performing 100 mutual funds in any of those years, in the next year, about half of the time, only 8 out of 100 remained in the top 100 the very next year.²

This study shows why a set-it-and-forget-it strategy is not always in your best interest because the investments you initially chose to help you meet your retirement goals may no longer be the best alternatives for you now.

In our 24/7 news-cycle world, tax policy, the economy, and consumer sentiment can change on a dime.

This is why we recommend rebalancing your 401(k) quarterly, or four times a year.

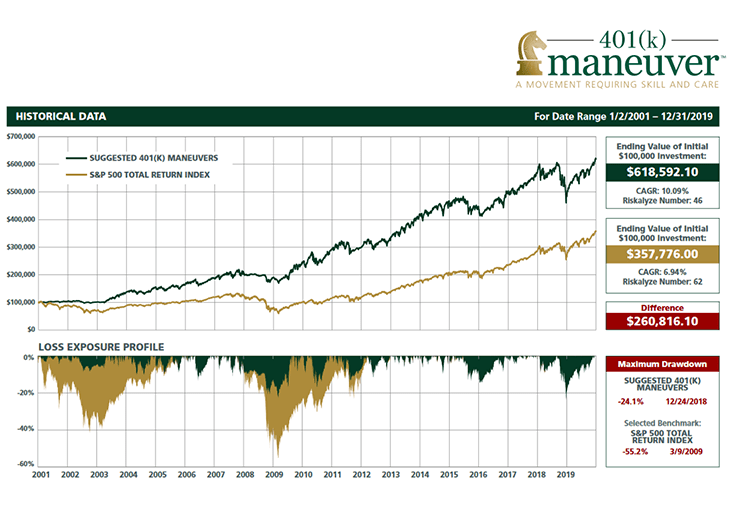

The 18-year chart below illustrates the potential better account performance when properly rebalancing your 401(k), 401(a), 403(b) or TSP account on a quarterly basis with third-party help.*

The gold line represents the hypothetical account allocations using the “buy and hold” philosophy.

The green line represents the potential increase in account performance using third-party advice and proper quarterly rebalancing.

To the right of the graph are the ending values of the initial investments of $100,000 shown in the green and gold lines.

The red box to the right shows the $260,816.10 hypothetical potential difference of assets in the account when you quarterly rebalance with professional help.

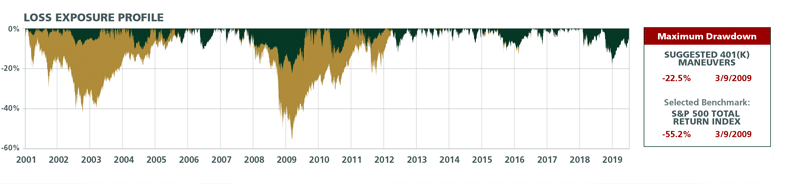

Now, take a look at the Loss Exposure Profile, which shows how each account would have performed during down markets.

The gold represents how unmanaged allocations experienced much larger losses during down markets versus the green, or quarterly rebalancing with third-party help.

The red box titled Maximum Drawdown represents the maximum percentage of loss experienced by each of these accounts–and the day it actually happened.

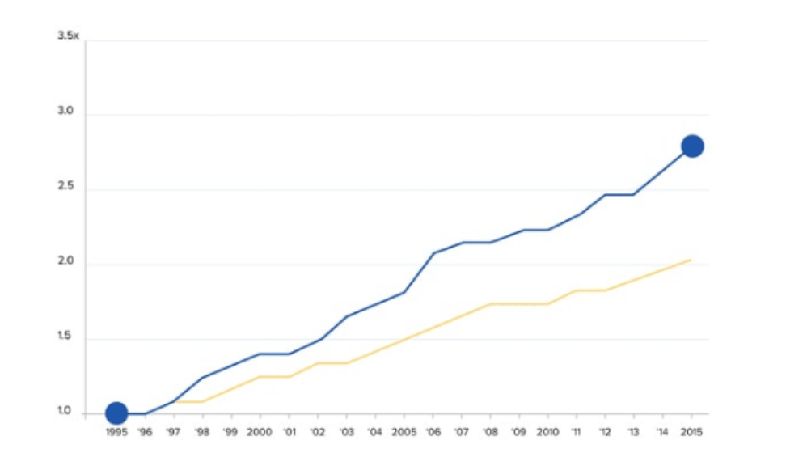

Other studies show that properly rebalancing your 401(k) every quarter with professional advice may significantly improve your 401(k) performance.

Aon Hewitt and Financial Engines conducted a study from 2006 to 2012 comparing the returns of investors who sought help in the form of online sources or managed accounts to those who managed their 401(k)s themselves.

The study examined the 401(k) investing behavior of 723,000 workers at 14 large U.S. employers and showed that people who received professional help earned higher median annual returns than those who invested alone.

In fact, “Participants who got Help received, on average, 3.32% (net of fees) more in return annually” than those who managed their own portfolios.³

“If two participants—one using Help and one not using Help—both invest $10,000 at age 45, assuming both participants receive the median returns identified in the report, the Help participant could have 79 percent more wealth at age 65 ($58,700) than the Non-Help participant ($32,800).”⁴

In a 2019 study titled Advisor’s Alpha, The Vanguard Fund Group, Inc., also reported a 3% average increase in the value of portfolios of clients who work with a good financial advisor.⁵

Stop and think for a moment about what impact 3% would have to your retirement income.

Would it make the difference between having just enough to get by or being able to enjoy your retirement?

Check out our retirement calculator to see how much you may have at retirement, and how 3% may improve your 401(k) performance.

Save More for Retirement

If you are unsure how to properly rebalance your account or don’t know where to start, we’re here to help.

401(k) Maneuver exists to help employees grow and protect their 401(k) accounts.

Our done-for-you, virtual service allows you to keep your 401(k) right where it is while we review and rebalance your account based on your risk tolerance and current market conditions.

There are no face-to-face meetings needed.

And we are not a robo advisor. We are real people who put your interests first.

Click here to see how we manage your 401(k) for you.

We regularly post videos with financial information and updates. Check us out on YouTube.

Sources:

- “Over 90% of Americans make this 401(k) Mistake.” Mauri Backman, The Motley Fool.

- The Impact of Expert Guidance on Participant Savings and Investment Behaviors. David Blanchett, Morningstar Investment Management Group, 2014.

- https://www.edelmanfinancialengines.com/press/2014/financial-engines-aon-hewitt-find-401k-participants-who-use-professional-help-are-better-off

- https://www.edelmanfinancialengines.com/press/2014/financial-engines-aon-hewitt-find-401k-participants-who-use-professional-help-are-better-off

- https://www.investopedia.com/articles/personal-finance/102616/how-much-can-advisor-help-your-returns-how-about-3-worth.asp