How to Quickly Catch Up on 401(k) Savings

For investors who are behind on retirement savings, it is possible to make up for lost time no matter how much has been saved or how close one is to retirement. Check out our tips on how to quickly catch up on 401(k) savings today.

Get a Plan in Place ASAP

If you’re behind on retirement savings and don’t have a plan or you had one at one point, but are way off track, it’s time to get a game plan together.

If you’re going to catch up on 401(k) savings, you need to get clear on how behind you are and how much you need to get back on track.

From there, you’ll need a plan to get you from where you are to where you need to be to comfortably retire.

If you’re concerned you’re too close to retirement or your balance isn’t big enough to even bother planning, we encourage you to think again.

Every little bit helps. Even a couple extra thousand dollars saved can make the difference between having enough money and struggling to survive.

If you need help figuring out exactly how much you need to retire and creating a successful plan, we suggest speaking to a third-party expert who can help you make the best decisions for how to catch up on 401(k) savings.

Contribute the Maximum to Your 401(k)

The easiest way to catch up on 401(k) savings is to maximize your contribution limit this year and each year until you retire.

In 2020, the annual contribution limit is $19,500 for employees who participate in 401(k), 403(b), most 457 plans, and the federal government’s Thrift Savings Plan.

For those age 50 and older, the 401(k) catch-up contribution limit is $6,500 in 2020.

This means if you’re 50 or older and need to catch up on 401(k) savings, you’ll be able to save $26,000 in your 401(k) this year.

Let’s assume you’re 52 years old, with $100,000 in retirement savings.

Because you’re age 50 and over, you’re legally allowed to save $26,000 per year in a 401(k) retirement fund.

Now, let’s assume a 7% rate of return, and that you’re able to contribute the maximum to your 401(k) until you retire at the age of 71.

By retirement, you’d have roughly $1.3 million saved.

It’s important to note that this number does not take into consideration inflation, how much your company matches, or future increases in yearly 401(k) contribution limits.

If it’s a stretch to contribute the full amount each year, do what you can to get as close to it as possible.

While it might seem like a sacrifice now, your future self will thank you. Promise.

> Discover how to secure a solid financial future and potentially keep more of your hard-earned money. Download our no-cost guide 5 Mistakes You Want to Avoid with Your 401(k) .

Reevaluate Your Spending Habits

Living beyond your means and overspending now can significantly set back your retirement savings plan.

And, if you carry the habit of overspending into retirement, it can seriously hurt your retirement lifestyle.

Cutting back spending is not as easy as it sounds.

In our culture of instant gratification and mass consumerism, it can be hard, especially when you’re cutting back now to save for a future payoff.

But it’s well worth the reward.

If you want to catch up on 401(k) savings, here are a few ways you can easily cut spending and, instead, put that money toward your retirement…

- Tell your kids and grandkids NO. If you’re going to put your financial future first, this means you need to put yourself ahead of your kids’ or grandkids’ college tuition, loans to family and friends, and even expensive gifts to your children. Think of it this way: your kids or grandkids have plenty of time to save for retirement. Let them take out the student loan or find another way to raise the money needed. Also, remember, when you focus on your retirement security first, your children won’t have the burden of taking care of you later on in life.

- Quiz yourself before making a purchase. This is an easy one (much easier than saying NO to the family). The next time you’re out shopping or before you hit the confirm purchase button while shopping online, ask yourself, “Is this a need or a want?” If it’s a want, don’t buy it right now. Instead, make a plan to save for it. Do this for a month, and you’ll be amazed at how much you curb your spending.

- Review your spending and see what you can cut. Take a look at the last 2 months’ worth of bank statements and see what you can trim from your monthly spending. With this information, decide what to cut back and, instead, put that money toward retirement savings.

Curbing spending means forming a new habit of living within your means. Take it one step at a time. Try it for 30 days and see what happens.

If you’re tempted to keep spending, remember this:

[Related Read: Pay Off Debt or Save for Retirement? Which Comes First?]

Get a Side Hustle

If you want to catch up on 401(k) savings, take on a side hustle and use the extra income to save more for retirement.

According to Bankrate’s Side Hustle Survey, “Nearly half of working Americans (45 percent) report having a gig outside of their primary job.”¹

The study also found that Americans who work an average of 12 hours a week on their side hustles earn about $1,222 per month.²

Whether it’s tutoring a few hours a week or delivering food or groceries on the weekend, the extra income of a side hustle may make a big difference in your retirement lifestyle…

And help you quickly catch up on 401(k) savings.

[Related Read: Close the Gap on Financial Goals with a Side Hustle]

Consider Working Longer

Depending on how much money you must save to catch up on 401(k) savings, you may need to work longer so you can contribute more.

Working longer also helps increase the amount of your Social Security check.

Social Security benefits take effect at age 62.

However, delaying retirement each year until 70 can increase your benefits 6% to 8% a year.

There are also downsides to taking Social Security too soon.

If you are 62 and eligible to draw benefits, you will only receive 75% of your benefits because you are under the full retirement age (FRA) of age 66 and 2 months.

Also, if you are still working full-time and make more than $17,640 in income in 2019, Social Security will penalize you for making too much money. One dollar in benefits will be withheld for every $2 in earnings above this limit.

To see what you might receive at different retirement ages, check out this Social Security calculator.

Seek Independent Third-Party Advice

If you want to catch up on 401(k) savings, we recommend seeking third-party advice as soon as possible.

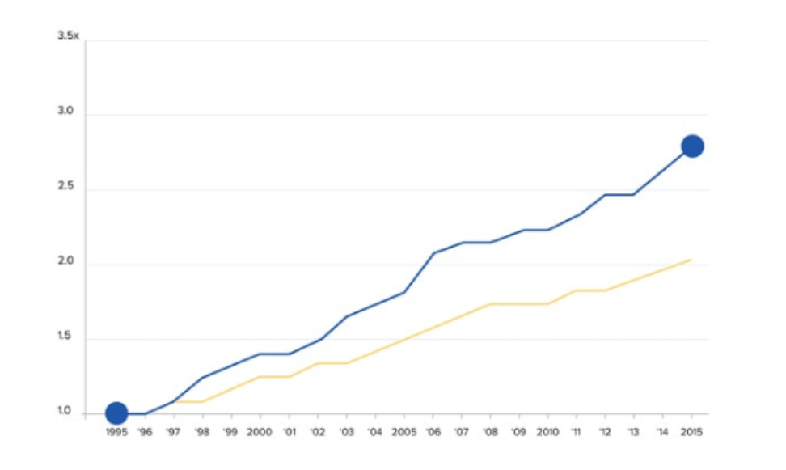

A May 2014 study conducted over a 6-year period compared those who had help with managing their 401(k) and those who did not. The study revealed…

“On average, the median annual returns for participants in the study who got Help were more than 3% (332 basis points, net of fees) higher than people who didn’t get Help.”³

From the graph above, you can see getting expert help with your 401(k) savings can be beneficial to life at retirement.

Click below to book a complimentary 15-minute 401(k) Strategy Session with one of our advisors today.

Book a 401(k) Strategy Session

Sources:

- https://www.bankrate.com/personal-finance/side-hustles-survey-june-2019/

- https://www.bankrate.com/personal-finance/side-hustles-survey-june-2019/

- AON Hewitt “Help in Defined Contribution Plans: 2006 through 2012” Published May 2014