How to Read a 401(k) Statement and Understand It

Too many investors don’t know how to read a 401(k) statement, much less understand it.

It’s understandable. There’s a lot in a statement. Knowing how to read and understand the information presented in a 401(k) statement may be vital to your retirement future.

Why Investors Need to Open and Read Their 401(k) Statements

Many investors approach their 401(k)s with a set-it-and-forget-it strategy. This is not advisable as 401(k)s are often people’s largest asset come retirement.

If you don’t pay attention to how your 401(k) is performing, understand what you’re paying in fees, or rebalance at least quarterly, you are not in control of your financial future.

Here’s a breakdown of the 3 reasons you want to make it a point to open and read your 401(k) statements:

- See how your 401(k) is performing.

- Understand what you are paying in fees.

- This is the part of your retirement that you control.

This last reason is critical because the three-legged stool of retirement is all but gone.

The stool once consisted of Pensions, Social Security, and Personal Savings.

Pensions, for the most part, are no longer a part of many workplaces. If you still have one, you are one of the lucky few.

The future of Social Security is uncertain. We hear daily the problems with Social Security running out of money or delaying the dates you may receive your income.

That leaves us with Personal Savings, which includes 401(k)s. Personal Savings is the only leg remaining that people can count on to support them in retirement.

Watch the video below to see how to read a 401(k) statement.

How to Read a 401(k) Statement Front Page Overview

Not all 401(k) statements are the same. In fact, there are hundreds of different types of 401(k) statements based on the company you work for and the plan you are in.

While they might look different, most statement front pages contain the following summary information of your account:

- Basic information

- Account summary

- Investment allocation summary

- Risk analysis/retirement goals progress

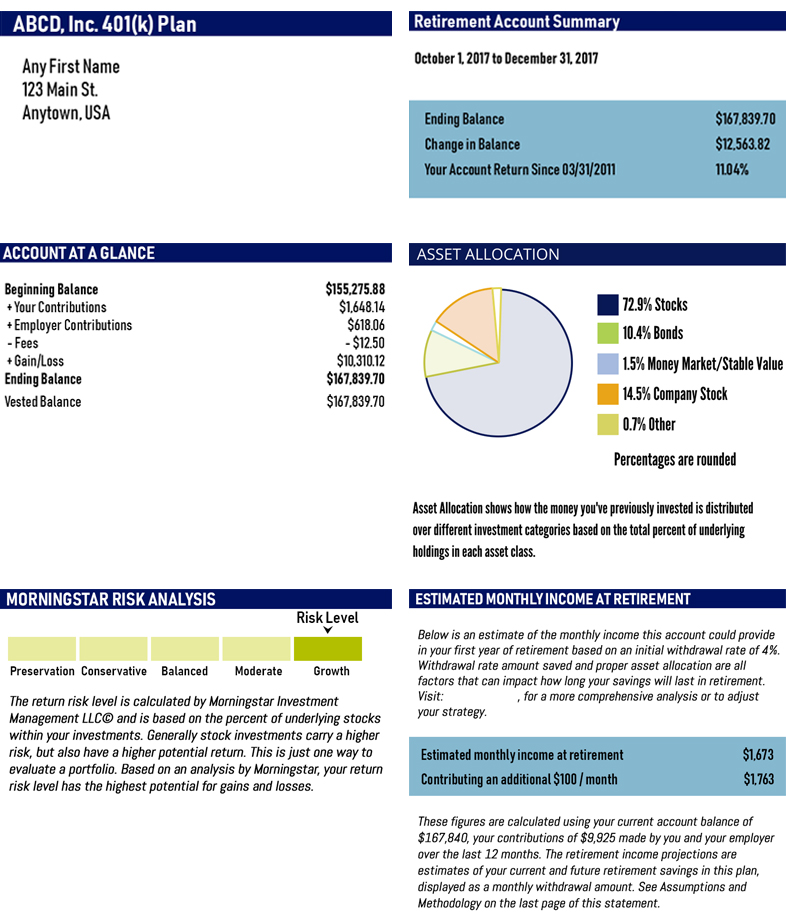

The following is an example of what is on the front page of most statements.

Let’s break down each section in detail.

Basic Information Section

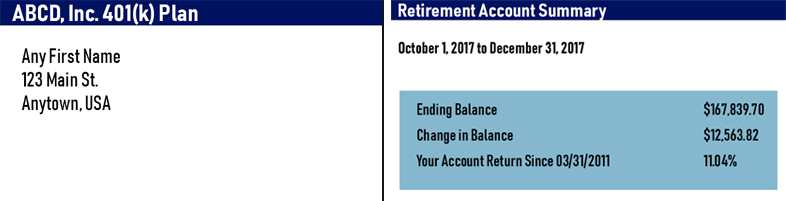

- 401(k) Plan Name and Investment Plan Sponsor Contact Information

Here you will see the name of your 401(k) plan and broker information, and may see the sponsoring firm’s name and contact information. - Your Contact Information

This is your basic information, such as name, address, and phone number. Always make sure to verify that this info is correct. - Statement Period

Your 401(k) statement period usually comes quarterly, and it will detail everything that happened during this time frame. - Your Beneficiary(ies)

This section lists your beneficiary or beneficiaries. Make sure to check who you have listed. If this is not printed on your statement, contact your HR department to find this information. - Your Personal Rate of Return

This is what you have earned in your 401(k) account per the period stated (which could be that period, year to date, or since inception).

Account Summary Section

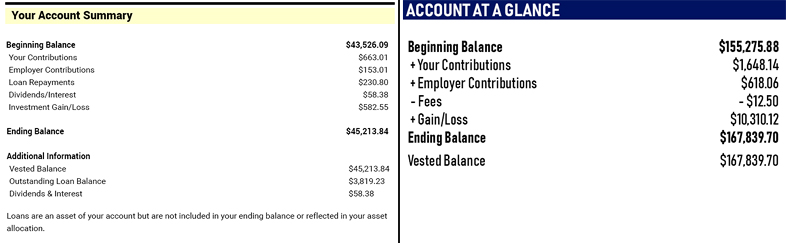

The account summary section often differs greatly from company to company. Here are two examples of what an account summary might look like.

Below is the information you may find in this section:

- Beginning Balance – Balance as of date.

- Your Contributions – Lists the amount you put into your 401(k), either pre-tax or post-tax.

- Employer Contributions – This is the amount your employer put in for you (the company match).

- Fees – These are deducted from your balance. These may be administrative fees, brokerage fees, or transaction costs. You want to check your plan website for more information.

- Your Distributions – If you’ve taken any distributions during this period, it will show any withdrawals from your account.

- Investment Gain/Loss – This is a breakdown of investment gains or losses during this period.

- Loan Repayments – If you have a loan, this will show any repayments you made this period.

- Dividends/Interest – Dividends are when a company distributes a portion of their earnings to you. Interest is the money earned for holding an investment like money market or bonds. This section lists the dividends and interest during a specific time frame.

- Ending Balance – This is your balance to date.

- Vested Balance – This is how much of your account is yours, if you leave your job. This is usually scaled over a 3-or-5 year period, depending on your company. After the declared period, 100% of the vested amount is yours. If your statement doesn’t show this, make sure to ask your HR department.

- Outstanding Loan Balance – If you have a loan against your account, it will show the loan amount and any payments made toward it.

Investment Allocation Summary Section

Asset allocation is defined as dividing an investment portfolio among different asset categories.

How you choose your investments is usually determined by your risk tolerance and time until you reach retirement.

Many people think that their company takes care of this for them. However, this is not the case. Your company cannot and will not. It’s your account, not theirs.

Again, another reason to open and read your 401(k) statements and take control of your financial future.

Other terms that you may see on your statement for this section are Balance by Asset Class, Current Investment Mix, Asset Allocation Summary, or simply, Your Positions or Holdings.

On your 401(k) statement, you will usually see a pie chart summary (like in the image above) of where and how your money is allocated between different asset classes such as:

- Stocks (Large Cap/Mid Cap/International)

- Bonds

- Money Market/Stable Value/Cash

- Company Stock

- Other Investments

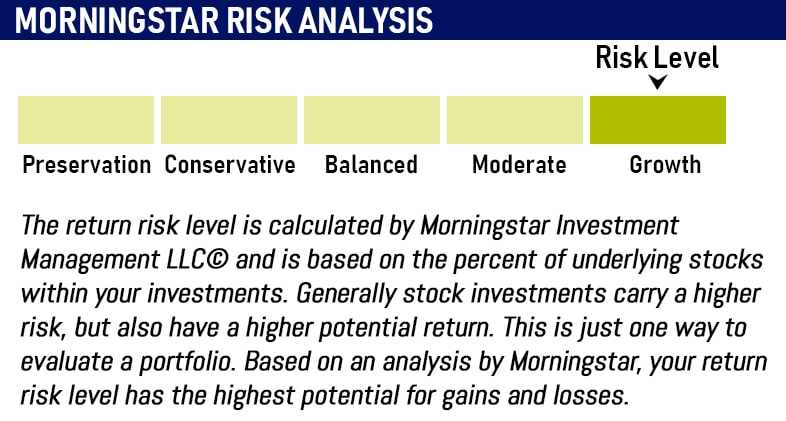

Risk Analysis/Retirement Goals Progress Section

The last section on most front pages will usually show either your risk profile or retirement goals progress.

Some of the larger 401(k) plans will have a section on the front page that tells you what your risk tolerance is based on your current holdings, as well as if you are on track to retire comfortably.

This may tell you if your 401(k) balance is in line with others of your age.

In this section, you may also find details to determine if you will have enough money at retirement, and how close you are to reaching these goals.

Some statements may also show what your balance may be worth as a monthly stream of income in retirement.

How to Understand the Details on a 401(k) Statement

Now that you know how to read and understand the account summary, or cover page, of your 401(k) statement, it’s time to dive into the details.

Specifically, the activity, transactions, fees, and investment options inside your 401(k) statement. This information is usually found on all the additional pages of your statement.

The details inside your 401(k) statement can be broken down into 6 sections:

- 401(k) Account Activity

- 401(k) Investment Activity

- 401(k) Transaction Details

- 401(k) Investment Fees

- 401(k) Investment Performance

- 401(k) Investment Options

The final pages of your statement are typically the customary 401(k) Statement Disclosures, which may be several pages in length.

Watch the video below

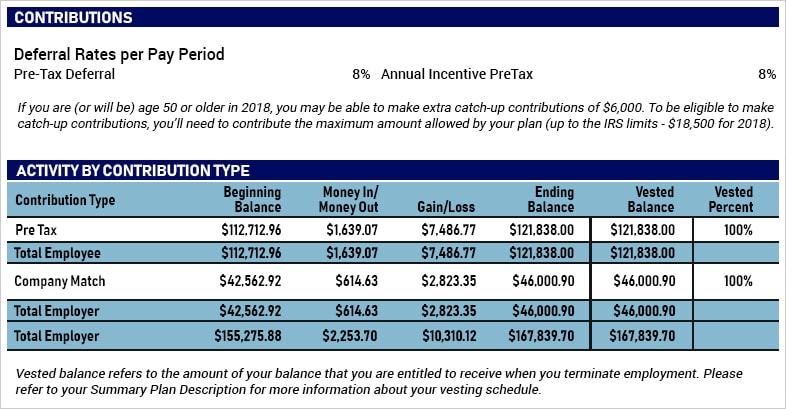

401(k) Account Activity

You may see on your statement, similar to the image below, a section that covers the activity of the current period.

This section includes:

- Your Activity By Contribution Type – This section may detail how much of your pay is going into your 401(k) and the maximum contribution you are allowed to put in for the year. In this example above, the employee is putting in 8% of each paycheck into the 401(k) plan. And, on a pre-tax basis. This means that contributions go into the account prior to any tax withholdings.

- Company Match – This is the amount of money your employer will put into your 401(k) for you each year. This is usually a percentage, up to a maximum amount, defined by the 401(k) plan. For example, if you put 3% of your pay into your 401(k), your employer may match 25%, 50% or 100% of this up to the same 3%. If you don’t know how much your company match is, ask HR for a copy of the 401(k) plan summary.

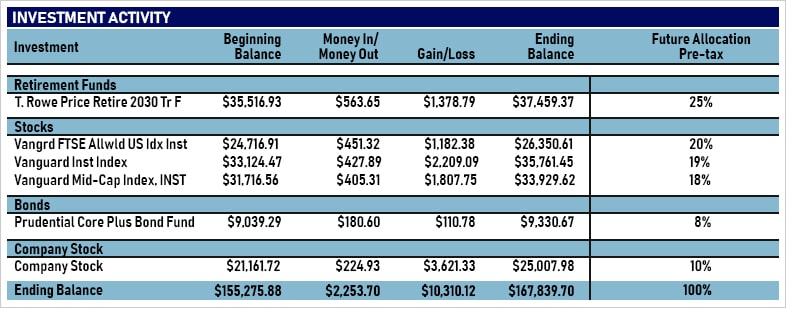

401(k) Investment Activity

This section breaks down any activity of your current holdings for this period.

Here you can see what you are invested in, what the balances are of each holding, and what percentage of your future allocations will be added to these holdings.

Let’s use the image above as an example.

- Column 1 (to the left) shows that this 401(k) is currently holding a 2030 target date fund, 3 Vanguard stock funds, 1 bond fund, and some company stock.

- Column 2 shows the beginning balance of each holding for this period.

- Column 3 shows how much money was put into each investment this period.

- Column 4 shows the gain or loss of each holding for this period.

- Column 5 shows the ending balance per holding for this period.

- The last column shows the percentage of future pre-tax contributions that will be added to the current holdings.

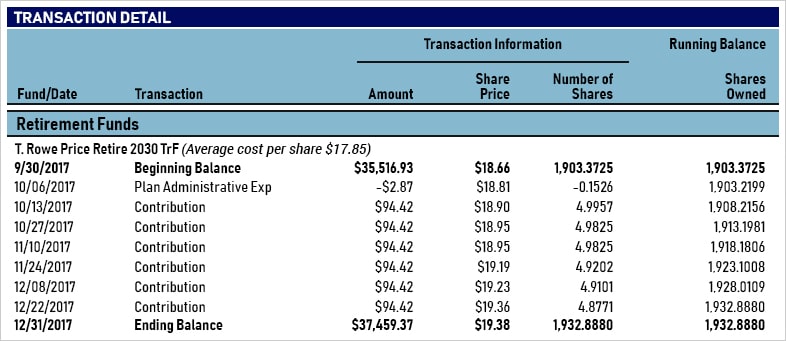

401(k) Transaction Details

On your statement, you will have transaction details for every holding in your account in this section.

Keeping with our statement example, we see the 2030 target date fund again.

- The column on the left shows the date of every transaction that occurred this period.

- Column 2 shows what transaction occurred.

- Column 3 starts with the beginning balance, shows every contribution, every expense, and ends with ending balance for the period.

- Column 4 shows the share price on the date of each contribution.

- Column 5 shows the number of shares that were purchased on this date, with the amount contributed.

- The final column to the right shows the running balance of shares owned, from the start of this period to the end.

This is a great example of dollar cost averaging. As you can see, since inception, the average cost per share of this fund is $17.85.

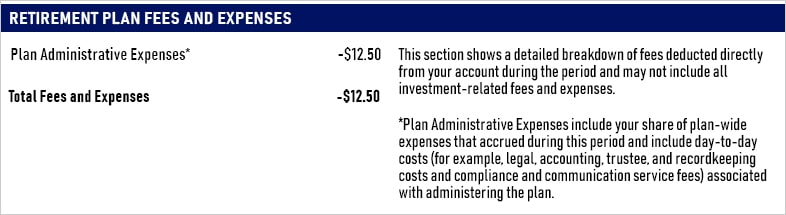

401(k) Retirement Plan Fees and Expenses

This section shows a detailed breakdown of fees that were directly debited from your account during the period.

These were listed in the above example chart as Plan Administrative Expenses. This is your share of expenses that everyone in your plan pays.

These normally include day-to-day costs to run the plan, such as legal, accounting, and trustee and recordkeeping costs.

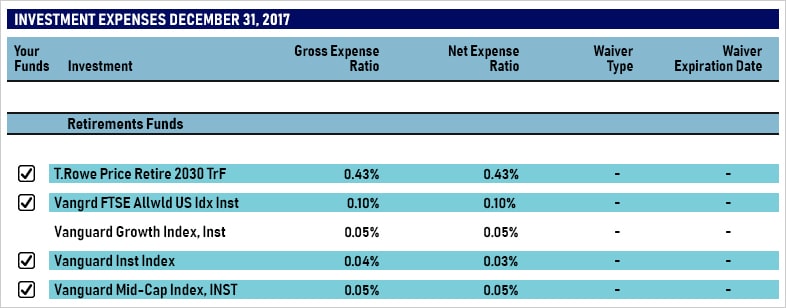

Not all of the 401(k) fees you are paying are easy to find.

Sometimes, it takes a little more research to understand your true costs in your 401(k) plan.

As you can see in the disclosure in the fine print below, there may be other expenses paid directly from the investment options you have to choose from, such as revenue sharing agreements, 12b-1 fees, and sub-transfer agent fees.

There are some additional fees that come from the funds themselves.

These fees are called expense ratios.

A quick definition: expense ratios are the total percentage of fund assets used for administrative, management, advertising (12b-1), and all other expenses.

For example, the 2030 target date fund expense ratio is 0.43% basis points, versus Vanguard’s Institutional Index expense ratio of 0.04% basis points. The expense ratio of the 2030 target date fund here is 10 times that of the Vanguard Fund.

How does the difference relate to you in terms of actual dollars?

Let’s say you had $100,000 invested in both the 2030 target date fund example with an expense ratio of 0.43% and the Vanguard Fund with an expense ratio of 0.04%.

This means you will pay $430 per year in fees for the 2030 target date fund versus $40 per year for the Vanguard Fund.

Your fees are more than 10 times with the 2030 target date fund.

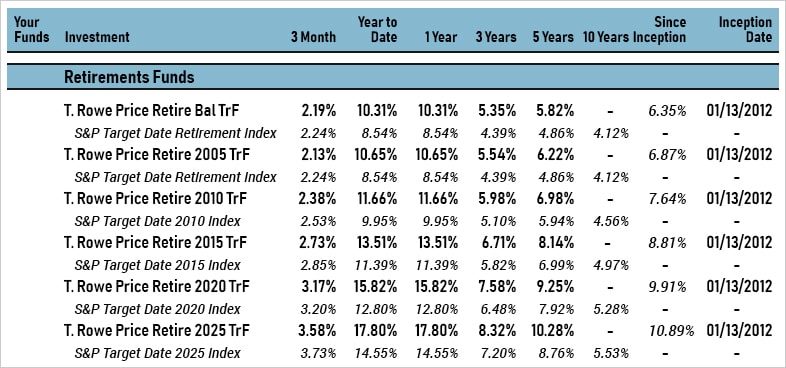

401(k) Investment Performance

On this chart, you will see your overall performance since the inception date of 11.04%. This is your account return or performance since you started it.

This account in our example has been active for more than 5 years, but less than 10. This is why the 10-year performance column is empty. The same goes for the 2030 target date fund.

You can see the difference in performance in these funds listed here.

Your statement will not look like others, as this depends on which fund you chose for your account, and what your risk tolerance was.

Understanding how this section works is very important for the long-term growth of your 401(k).

401(k) Investment Options

This part is where many investors get stuck.

Many 401(k) statements will have a list of all the available investment options for you to choose from.

Some plans start with as few as 10 investment choices, while others could have dozens of choices.

One of the biggest questions I have been asked over the years is, “How do I choose my 401(k) investments?”

This is where professional help comes in, and one of the reasons why 401(k) Maneuver was created.

Your adviser should be able to help you determine your tolerance to risk, how long it is until you retire, and any other information needed to choose the correct funds.

Not everyone is the same, nor should he/she be.

The chart starts with your available target date funds. As you can see, there are many different years.

Some plans today auto enroll you into the one closest to your retirement age, which may or may not be in your best interest. And for many good reasons. Like the difference in fees we discussed earlier, and the difference in performance over time.

You may also have similar charts that show Stock Funds, Bond Funds, and Money Market or Stable Value Funds. When you see all these, you may want to seek professional help.

401(k) Statement Disclosures

The last section on your statement will most likely be the fine print or disclosures of your 401(k) plan.

This could be several pages in length, and a good rule of thumb is, the longer your statement is, the more detailed the disclosures will be.

Your Next Steps

The above is a lot of information and why 401(k) investors need professional account management.

401(k) Maneuver provides independent, professional account management to help employees, just like you, grow and protect their 401(k) accounts.

Our goal is to increase your account performance over time, manage downside risk to minimize losses, and reduce fees that are hurting your retirement account performance.

With 401(k) Maneuver, you can go about your life doing what you love with confidence, knowing we are handling the changes for you.

If you’d like to see how professional account management may improve your 401(k) account performance, check out our calculator.

Have questions or concerns about your 401(k) performance? Click below to book a complimentary 15-minute 401(k) Strategy Session with one of our advisors today.

Book a 401(k) Strategy Session