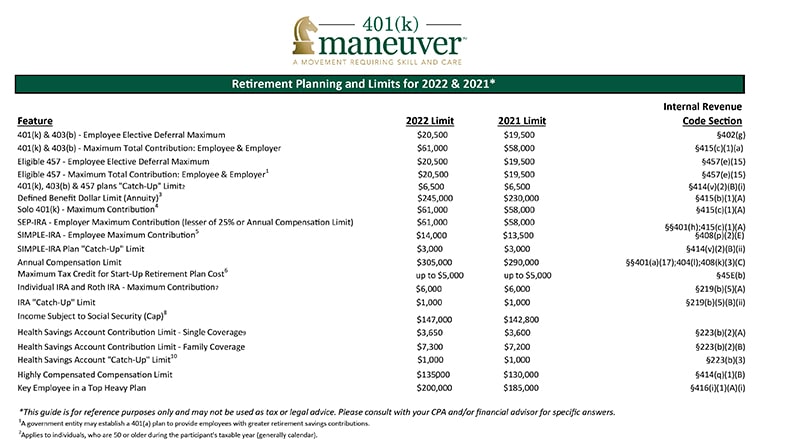

Retirement Plan Contribution Limits for 2022

The IRS has announced contribution limits for qualified retirement plans for 2022.

However, there may be changes coming to the info below.

In the November 3 draft of the Build Back America Act currently sitting in Congress, there are proposed provisions to curb contributions and accelerated distributions for high-balance retirement accounts.

In addition, the bill also has provisions to cut backdoor Roth IRAs and after-tax 401(k) contributions.

We will update you as things unfold.

In the meantime, keep reading below to find out exactly how much you can contribute for 2022, and start making plans now to do what you can to max out your retirement savings next year.

401(k) Retirement Plan Contribution Limits for 2022

401(k)s

Employee contribution limits for 401(k), 403(b), most 457 plans, and the federal Thrift Savings Plan are $20,500 – up from $19,500.

For those age 50 and older, the 401(k) catch-up contribution remains the same at $6,500 for 2022. If you turn 50 anytime during December of 2021, you’re still eligible to contribute the additional $6,500.

After-Tax 401(k) Contributions

If you are self-employed or your employer allows for after-tax contributions, the overall defined contribution plan limit will increase to $61,000 – up from $58,000 in 2021. The $61,000 is a cap of the maximum $20,500 contribution limit deferral, plus employer contributions.

Solo 401(k)s

If you have a Solo 401(k), otherwise known as a Self-Employed 401(k) or Individual 401(k), the contribution limits will increase to $61,000 in 2022, up from $58,000 in 2021. This is how much you can contribute as an employer.

The compensation limit has also risen to $305,000 in 2022, up from $290,000 in 2021.

IRA Retirement Plan Contribution Limits for 2022

IRAs

People with individual retirement accounts will not see an increase and contribution limits stay the same for 2022, with a $6,000 maximum contribution limit. This applies to pre-tax or Roth IRAs.

The catch-up contribution for people age 50 and over remains the same additional $1,000.

While the contributions have stayed flat since 2019, there are changes to the Deductible IRA Phaseouts and to Roth IRA Phaseouts.

Expert Tip: You can contribute the maximum for 2021 until April 15, 2022. If you have an IRA, plan now to maximize the contribution limit for 2021 before April 15 next year.

SEP IRAs

Contribution limits for SEPs, or Simplified Employee Pensions, have increased to $61,000 in 2022, up from $58,000. The compensation limit has also gone up from $290,000 in 2021 to $305,000 in 2022.

SIMPLE IRAs

Contribution limits for SIMPLE retirement plans for 2022 increase to $14,000, up from $13,500 in 2021. The catch-up limit remains the same at $3,000.

Deductible IRA Phaseouts

You can earn a little more in 2022 and get to deduct your contributions to a traditional IRA. For singles and heads of household who are covered by a workplace retirement plan, such as a 401(k), and contribute to a traditional IRA, the phaseout range is between $68,000 and $78,000, up from $66,000 and $76,000 in 2021.

For 2022, the adjusted gross income (AGI) phaseout range for married couples filing jointly who are contributing to a traditional IRA is between $109,000 and $129,000 for 2022, up from $105,000 and $125,000 in 2021.

If you contribute to an IRA but are not covered by a workplace retirement plan, and are married to someone who is, the deduction is phased out if your joint income is between $204,000 and $214,000 in 2022. This is up from $198,000 and $208,000 in 2021.

Expert Tip: You can still contribute to an IRA even if you earn too much–it’s just nondeductible.

Roth IRA Phaseouts

The phaseout range for married couples filing jointly who are covered by a workplace retirement plan and contribute to a Roth IRA in 2022 will increase. For 2022, it will be between $204,000 and $214,000, up from $198,000 and $208,000 in 2021.

For heads of household or those filing as single, the phaseout range is between $129,000 and $144,000 in 2022, up from $125,000 and $140,000 in 2021.

Other Retirement Plan Contribution Limits for 2022

Defined Benefit Plans

The limit on the annual contribution of a defined benefit plan in 2022 will increase to $245,000, up from $230,000 in 2021.

Saver’s Credit

For low and moderate income workers, the new Saver’s Credit (also known as the Retirement Savings Contributions Credit) limit increased to $68,000 for married couples filing jointly – up from $66,000. For heads of the household, the limit has increased from $49,500 to $51,000 in 2022. For singles and married couples filing separately, the limit is $34,000, up $1,000 from 2021.

Have questions or concerns about your 401(k) performance? Click below to book a complimentary 15-minute call with one of our advisors today.

Book a 401(k) Strategy Session