Survey Finds Only 27% of Working Adults Are on Track for Retirement

The world has changed over the last year, and, as a result, many of our priorities have shifted – including saving and preparation for retirement.

This past January, Schroders US Retirement Survey 2021 asked 1,000 people about their state of retirement readiness and planning, as well as how their saving and investing priorities have changed since the health crisis started in March of 2020.

Keep reading to find out how you measure up and the steps you can take today to avoid being unprepared for retirement.

Current State of US Retirement Savings

According to the Schroders US Retirement Survey, only 27% of respondents said they feel very good and fully on track about their retirement. That leaves the majority not prepared for the future.¹

Of those near or at retirement (ages 60-70), only 26% said they have enough saved for retirement. 60% said they were not prepared and 7% said they did not know.²

In addition, 62% of working people plan to keep working in retirement.³

57% responded they would keep working because they enjoy it, while 53% said they would keep working in retirement to cover basic living expenses.⁴

Barriers to Retirement

While saving for retirement and the future is one of the top 3 activities people are committed to since the health crisis started (39% of respondents have increased their focus on saving), the survey also found 3 key barriers to retirement:

- 70% said they don’t have enough saved yet to plan for retirement.

- 60% said they have more pressing financial priorities than saving for retirement.

- 50% said the future is too uncertain to plan for retirement at this time.⁵

Steps You Can Take Today to Plan for Retirement

The results of the survey are clear: whether we’re just starting our first job or we’re nearing retirement, a vast majority of us are not prepared for retirement.

When you have debt, kids to feed, healthcare costs, and a house to maintain, how do you focus on saving for your financial future and other financial commitments?

It’s as simple as creating a plan and committing to work the plan.

Step 1: Create a Retirement Savings Plan

Knowing where you are and where you need to be helps you know exactly what you need to do in order to have a comfortable retirement.

Looking at that gap may be uncomfortable, but it’s where you need to start.

The reality is, if you don’t create a plan NOW (no matter your age), chances are, you aren’t going to have enough money to comfortably retire.

With rising healthcare costs, inflation, taxes, down markets, and other unknown future variables, one thing is certain: if you don’t have a plan and take action on that plan now, you’re likely not going to have enough to retire.

Or worse, you’ll end up with so little saved that you might have to struggle to survive.

Let’s say you had close to $250,000 saved for retirement, and you were making $50,000 per year at your job when you retired. How long do you think your money is going to last you in retirement?

Will this give you the retirement you truly desire?

For most, the answer is no. Not even close!

So, do you know how much you will need to retire?

If not, sit down and figure out what you will need to maintain your standard of living when you stop working.

- At what age do you want to retire?

- How much money will you need, not to just scrape by, but have a fulfilling, comfortable retirement?

This is what you need to figure out. Write it down.

If you created a plan years ago, but haven’t followed it, then hit the reset button and create a new plan based on where you are now.

If you don’t know, reach out to an expert who can help you develop out a solid plan.

Step 2: Regularly Fund Your Retirement Plan

You may not have the amount needed right now to fulfill your retirement goals, but every little bit you contribute helps.

When it comes to retirement savings, the name of the game is compounding. So the more you are able to invest now, the more you’ll have come retirement.

The key here is to regularly contribute each month or pay period. Even if it’s 1 or 2% of your salary – something is better than nothing at all.

Contribution Limits

Employee 401(k) contribution limits for 2021 will stay the same as 2020 – at $19,500. This applies to 401(k), 403(b), most 457 plans, and the federal Thrift Savings Plan.

For those age 50 and older, the 401(k) catch-up contribution is $6,500.

The 2021 contribution limit for IRAs is $6,000, and the catch-up contribution for people age 50 and over is $1,000, or $7,000 total. This applies to Roth and traditional IRAs.

[Related Read: Retirement Plan Contribution Limits for 2021]

Company Match

If you have a 401(k) and are tight on cash, see what you can do to at least meet the company match – if available.

If you can’t max out the annual contribution limits for a given year, at least put in enough to get the full company match.

Company matching is one of the secrets to maximizing your 401(k), and it’s often the most overlooked.

When your company matches you, it’s like getting free money. Depending on what your company matches and how much you’ve saved, it may double the amount of what you’re already saving.

Let’s say your company matched 100% up to 6% of your pay. With a $55,000 salary, you could put in 6%, or $3,300 for the year, and the company would match this at 100%.

That’s another $3,300 per year of free money that’s yours to keep! This extra $3,300 doesn’t include compounding your earnings. This is just about the additional money you could be saving with your company match.

Remember, you don’t have to wait for enrollment season to make changes to your 401(k) election. You can make changes anytime during the year.

[Access our guide on how to Supercharge Your 401(k) performance .]

Step 3: Seek Expert Guidance Sooner Rather Than Later

Although you might have basic investment knowledge, utilizing an expert to do the in-depth market research could change the performance of your retirement savings accounts from good to great.

In fact, David Blanchett, Head of Retirement, CFP, CFA of Morningstar reported that participants that received expert guidance had as much as 40% more income during retirement versus those who received no help at all.⁶

If you’re hesitant to reach out for advice because you think your account balance is too small and you need more money saved, don’t let that stop you from getting help.

This is your future we’re talking about.

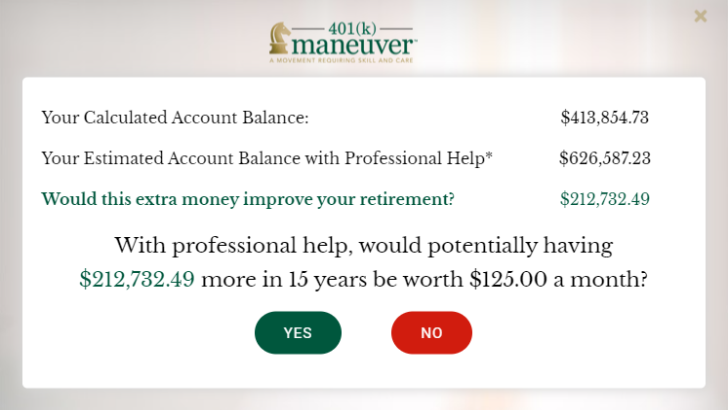

Let’s say you have an account balance of $150,000, and you expect 7% returns, and you have 15 years until retirement.

Using our 401(k) calculator, you would see that having professional help to properly rebalance your account may improve your retirement by $212,732.49.

The calculations below do not include employer contributions or future salary deferrals. With those included, you can see that the difference has the potential to be much larger.

Continuing with the example above, imagine what an additional $212,732.49 at retirement might mean for your future.

Would it mean not having to work full- or part-time longer than you want to?

Could you travel more? Or spend more time crossing items off your bucket list?

Could you have a comfortable retirement and not have to worry about money?

Take a moment to answer these questions.

Now, answer this: Can you afford not to seek professional help to regularly rebalance your 401(k)?

Check out our 401(k) calculator here to see how you may improve your account performance.

Sources:

- https://www.schroders.com/en/us/institutional/dc/retirement-survey-2021/

- https://www.schroders.com/en/sysglobalassets/digital/us/us-dc/schroders-us-retirement-survey_final-2021.pdf

- https://www.schroders.com/en/sysglobalassets/digital/us/us-dc/schroders-us-retirement-survey_final-2021.pdf

- https://www.schroders.com/en/sysglobalassets/digital/us/us-dc/schroders-us-retirement-survey_final-2021.pdf

- https://www.schroders.com/en/sysglobalassets/digital/us/us-dc/schroders-us-retirement-survey_final-2021.pdf

- David Blanchet, Head of Retirement, CFP, CFA, Morningstar 2014, “The Impact of Expert Guidance on Participant Savings and Investment Behaviors”