The #1 Correctable Behavior Studies Repeatedly Show Improves 401(k) Performance by 3%

What’s the one correctable behavior–when done four times a year–that studies show may improve 401(k) performance by 3% 6 ?

It doesn’t require you to contribute more each paycheck…

Nor do you have to inject a large sum of cash into your 401(k)…

It’s as simple as properly rebalancing your 401(k) four times a year.

How Rebalancing Works

Rebalancing is the process of realigning the weightings of the assets (your investments) in the portfolio.

This can involve periodically buying and/or selling assets in the portfolio in order to maintain the initial desired level of asset allocation.

For example, this would need to happen if maintaining a certain percentage amount of stocks and bonds was the desired goal.

If, over time, the stocks outperformed bonds, a person may need to sell off some of the profits created by stocks to buy more bonds, so the portfolio maintains the desired balance.

Therefore, a rebalancing of your portfolio may need to take place from time to time throughout each year.

Rebalancing is not the same thing as asset allocation.

Account allocation is a type of investment strategy that attempts to balance risk versus reward by adjusting the percentage of each asset in a portfolio, based on risk tolerance, investment time frame, and objectives.

In order to help investors grow their accounts, while at the same time keeping risk in check, an asset allocation strategy is often put in place.

Click here to discover the difference between account rebalancing and asset allocation, and how account balancing and allocation may affect your 401(k) performance.

How Rebalancing Helps Improve 401(k) Performance

In the past, traditional investors have been told to follow a “buy and hold” strategy with their 401(k) accounts.

The issue is that a set-it-and-forget-it approach often causes investors to potentially miss out on earning more and keeping more of their hard-earned retirement savings.

Because unmanaged allocations may experience much larger losses in down markets and may miss the opportunity for growth during good markets.

You see, the investments you initially chose to help you meet your retirement goals–whether that was 10 years ago or 10 months ago–may no longer be the best alternatives for you now.

Take into consideration changing market conditions, trade policy, and consumer sentiment–and it doesn’t make sense to always buy and hold.

Yet, despite this, 80% of 401(k) investors fail to rebalance.¹

Just like driving cross-country, if there is a roadblock or other obstacle preventing you from reaching your destination, you need to make the appropriate changes in order to stay on course.

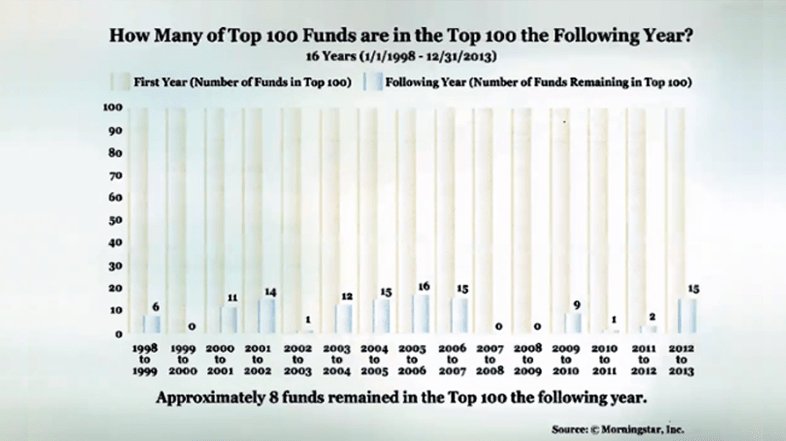

Morningstar conducted a study that monitored the top 100 best-performing mutual funds between January 1, 1998, and December 31, 2013.

This study revealed that, in any given year of top best-performing 100 mutual funds in any of those years, in the next year, about half of the time, only 8 out of 100 remained in the top 100 the very next year.²

This study shows why a set-it-and-forget-it strategy is not always advantageous.

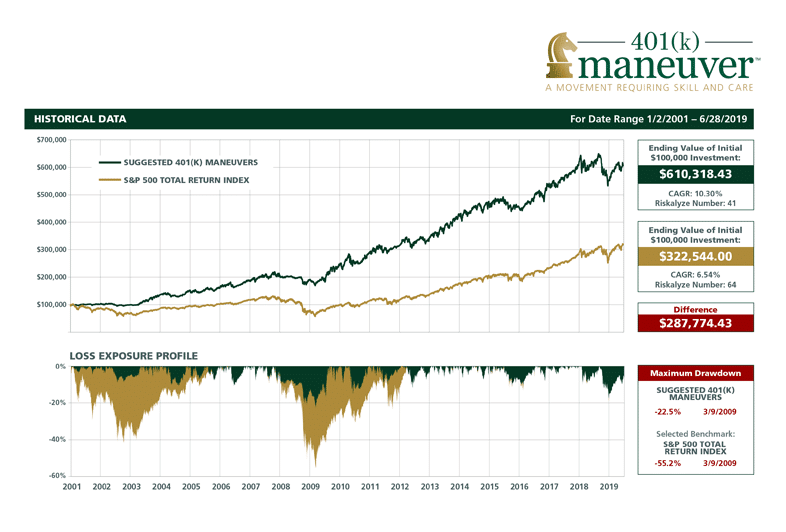

Take a look at the 18-year chart below.

It illustrates the potential better account performance when properly rebalancing your 401(a), 401(k), 403 (b) or TSP account on a quarterly basis with third-party help.*

The gold line represents the hypothetical account allocations using the “buy and hold” philosophy.

The green line represents the potential increase in account performance using third-party advice and proper quarterly rebalancing.

To the right of the graph are the ending values of the initial investments of $100,000 shown in the green and gold lines.

The red box to the right shows the $287,774.43 hypothetical potential difference of assets in the account when you quarterly rebalance with professional help.

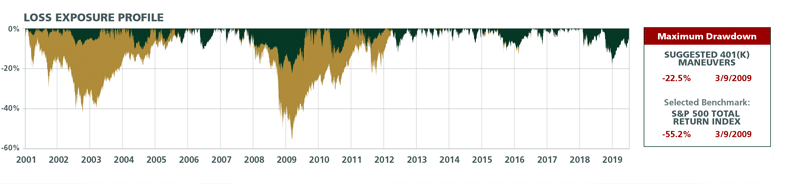

Now, take a look at the Loss Exposure Profile, which shows how each account would have performed during down markets.

The gold represents how unmanaged allocations experienced much larger losses during down markets versus the green, or quarterly rebalancing with third-party help.

The red box titled Maximum Drawdown represents the maximum percentage of loss experienced by each of these accounts–and the day it actually happened.

Again, this further shows the difference proper quarterly rebalancing with third-party help may have on your 401(k) performance and…

Other studies show that properly rebalancing your 401(k) every quarter with professional advice may significantly improve your 401(k) performance.

Aon Hewitt and Financial Engines conducted a study from 2006 to 2012 comparing the returns of investors who sought help in the form of online sources or managed accounts to those who managed their 401(k)s themselves.

The study examined the 401(k) investing behavior of 723,000 workers at 14 large US employers and showed that people who received professional help earned higher median annual returns than those who invested alone.

In fact, “Participants who got Help received, on average, 3.32% (net of fees) more in return annually” than those who managed their own portfolios.³

“If two participants—one using Help and one not using Help—both invest $10,000 at age 45, assuming both participants receive the median returns identified in the report, the Help participant could have 79 percent more wealth at age 65 ($58,700) than the Non-Help participant ($32,800).”⁴

In a 2019 study titled Advisor’s Alpha, The Vanguard Fund Group, Inc. also reported a 3% 6 average increase in the value of portfolios of clients who work with a good financial advisor.⁵

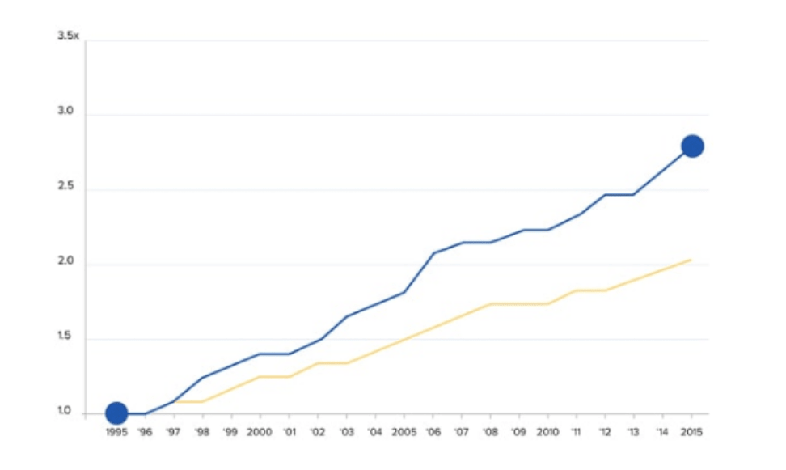

Take a look below to see the potential of adding 3% 6 more to your 401(k) over time.

Check out our retirement calculator to see how much you may have at retirement, and how 3% 6 can improve your 401(k) performance.

If you had severe chest pain, you wouldn’t treat yourself without the help of a doctor, would you?

Or if you broke your leg, you wouldn’t just leave it, hoping it heals on its own.

So, why would you turn what could be your largest financial asset over to chance?

If you’d like to take control of your financial future and potentially have more income at retirement, we strongly suggest working with someone who can help you rebalance your account allocations every quarter, or four times a year.

The type of advice you receive about your finances may be impacted by the type of advisor you resource for advice.

Download our no-cost guide on how to understand The Different Types of Licenses Financial Advisors Have and What They Mean to You .

Sources:

- “Over 90% of Americans make this 401(k) Mistake.” Mauri Backman, The Motley Fool.

- The Impact of Expert Guidance on Participant Savings and Investment Behaviors. David Blanchett, Morningstar Investment Management Group, 2014.

- https://www.edelmanfinancialengines.com/press/2014/financial-engines-aon-hewitt-find-401k-participants-who-use-professional-help-are-better-off

- https://www.edelmanfinancialengines.com/press/2014/financial-engines-aon-hewitt-find-401k-participants-who-use-professional-help-are-better-off

- https://www.investopedia.com/articles/personal-finance/102616/how-much-can-advisor-help-your-returns-how-about-3-worth.asp

- http://www.aon.mediaroom.com/new-releases?item=136959