3 Simple Actions That May Maximize Retirement Investments in 2nd Quarter

Contrary to what some investors believe, a 401(k) plan is not a “set it and forget it” program.

It’s just like driving cross-country. If there is a roadblock or other obstacle preventing you from reaching your destination, you need to make the appropriate changes in order to stay on course.So, if you’ve set up a 401(k) or other workplace retirement plan and you aren’t regularly looking at your statements, making changes, or maxing out your contribution limits, chances are you may not reach your retirement goals.

Or worse, you may not even come close.

Let’s pause for a moment and look at some statistics of where America is with retirement savings:

- A study conducted in late 2018 by Fidelity Investments showed that out of 16.2 million 401(k) participants, only 187,000 had over a million dollars in their 401(k).¹

- According to Vanguard, the median 401(k) account balance for an investor age 65 and older was $58,035 in 2018.²

It’s no wonder the Federal Reserve Bank of Saint Louis recently stated: “It could be worrisome that, for many American households, the total balance of their retirement accounts may not be sufficient to ensure a solid life in retirement.”³

What this says is that it’s time for America to take charge of their retirement. It’s time for you to get serious about the income you want at retirement.

Because what you do today may greatly impact your future income at retirement.

So where do you begin?

While there are many tools available to help you fit your investments to your needs, the truth is that by making just a few simple changes this quarter, you may catapult the performance of your 401(k) and move yourself closer to your short- and long-term financial goals.

Read on for the 3 things you can do right now–this quarter–to maximize your retirement investments.

Tip #1 That May Maximize Your Retirement Savings: Company Matching

A common mistake made with 401(k)s or other workplace retirement plans is not to put in–at a minimum–what the company matches.

If you’re not doing it, don’t feel bad. Perhaps you don’t know it is available to you or understand how it could help you maximize your retirement savings.

Whatever the case, I’m here to tell you that it’s really important that you contribute at least the minimum of what your company will match because, if you aren’t doing it, you may be leaving a lot of money on the table.

In some cases, it may double the amount of what you’re already saving.

It may increase your retirement lifestyle.

And it may help you accumulate the amount of money you desire at retirement.

Let me ask you this: In your 401(k) or workplace retirement account, how much is your company putting into your 401(k) each pay, along with what you are putting in?

Are they matching 25%, 50%, or even 100% of what you are putting in up to a certain amount, like 3% 7 or 6% of your pay?

Do you know the answer?

If you don’t know, don’t feel bad. Not a lot of people do know this off the top of their head.

Company matching is one of the secrets to maximizing your 401(k) or workplace retirement account, and it’s often the most overlooked.

But it’s really important because, if your company matches what you put in out of each pay, up to a certain percentage, it’s basically FREE money to you.

Let’s say you work for ABC company, and out of each pay the company will match 25%, up to 3% 7 of your annual pay. If you make $40,000 a year and you put in 3% 7 automatically into your 401(k), that would be $1,200 a year that you’ve contributed. And if your company match is 25%–or 25 cents per dollar–they would put in an additional $300 per year.

That’s $300 of free money you get to keep!

Using the same scenario as above, let’s say your company matched 100% up to 6% of your pay. With same $40,000 salary, you could put in 6% or $2,400 for the year, and the company would match this at 100%. That’s another $2,400 per year of free money that’s yours to keep!

And this doesn’t include compounding interest or your earnings. This is just about the additional money you could be saving with your company match.

So, let me ask you this…

If you could put an additional $300 or $2,400 in your 401(K) each year, per the examples above, why would you NOT at least put in up to your company match?

Could you imagine how your 401(k) or workplace accounts could grow over 10, 20, 30 years while working…if you made sure to at least put into your retirement savings what your company matched?

Folks, this is powerful! And if you aren’t doing it, you’re missing out.

Your Next Steps:

1)Sit down today and look at your statements. Make sure you are at least putting in this year what your company matches.

2)If you aren’t, contact your Human Resources department at your place of employment.

3)If you’re already doing this, great! Now see if you can contribute 5 or 10% more than what you planned. Even better, see what you can do to maximize your 2019 contribution. (Remember, the new contribution limits for employees who participate in 401(k) plans in 2019 is $19,000, up from $18,500 in 2018. And $25,000 for those 50 and older.)

Click here for more expert advice on how to Supercharge Your 401(k) performance.

Tip #2 That May Maximize Your Retirement Savings: Quarterly Rebalancing

When it comes to the market, the only constant is change.

The stock or mutual fund that you chose last year–or even last quarter–may or may not necessarily still be going in the right direction for you.

This is why successful 401(k) investors rebalance their account allocations every quarter, or four times a year.

Successful 401(k) investors know that it’s not only important what they EARN in return, but it’s also important what they KEEP that may have a big impact on their future account value…

And their ability to reach that dream retirement lifestyle they desire.

Sadly, few people rebalance their 401(k) account.

In fact, 80% of 401(k) investors fail to rebalance.⁴

Why is this? Well, in the past, many of us were told that if we’re a traditional investor, we should follow a buy and hold strategy with our 401(k) or other workplace retirement accounts.

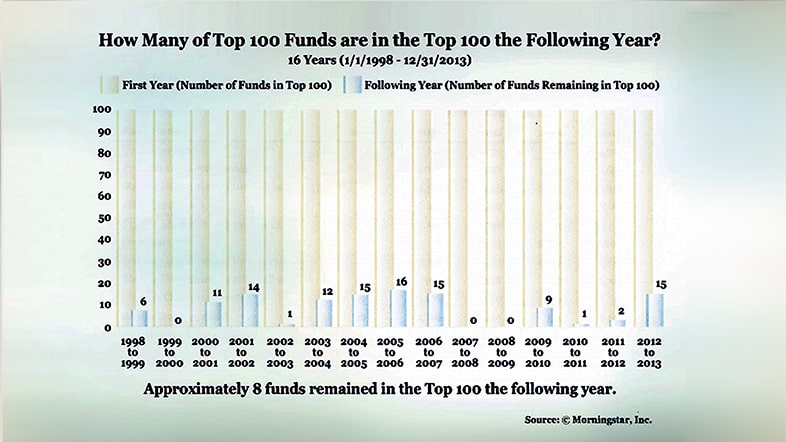

But a recent Morningstar study shows that, as investors, it may not be wise to be a buy and hold type of investor when it comes to your 401(k).⁵

The study monitored the top 100 best-performing mutual funds between January 1, 1998, and December 31, 2013.

And it revealed that, in any given year of top best-performing 100 mutual funds in any of those years, in the next year, about ½ of the time, 8 out of 100 remained in the top 100 the very next year!

If you aren’t rebalancing your account allocations, you may be missing out on earning more and keeping more of your hard-earned retirement savings.

Because unmanaged allocations may experience much larger losses in down markets and may miss the opportunity for growth during good markets.

Your Next Steps:

It’s the start of the quarter, which means it’s a perfect time to rebalance your account allocations!

However, we suggest having an expert take a look at your account on a quarterly basis, and rebalance if necessary to keep you on course, both now and down the road.

We also recommend getting third-party advice because those who do rebalance on their own often fail to manage risk through proper asset allocation. Rebalancing only the percentages of current holdings does not consider current market and economic conditions. This often results in more significant losses during bad markets.

Have questions about your 401(k)? Reach out to us on our Facebook page and we’ll answer you.

Tip #3 That May Maximize Your Retirement Savings: Seek Third-Party Advice

Although you might have basic investment knowledge, utilizing an expert to do the in-depth market research could change the performance of your account from good to great.

In fact, a Morningstar report shows that participants that received expert guidance had as much as 40% more income during retirement versus those who received no help at all.⁶

For this reason, it may be beneficial to turn to an expert for help with investing and allocating your 401(k) or other workplace retirement plan account.

Even though your 401(k) is employer-sponsored, it does not mean they are making changes on your behalf. It’s your account. It’s your money. And it’s your job to look out for your future.

If you’re hesitant to reach out for advice because you think your account balance isn’t big enough, or you think you’re too close to retirement to get help, don’t let that stop you! Let me repeat that: Don’t let your balance or your age stop you from seeking advice.

This is your future. This is your life. And it’s never too late to make changes!

We provide private, third-party advice to guide America’s employees on how they may properly rebalance and reallocate their 401(k) investments each and every quarter.

Download our GUIDE on How To Supercharge Your 401(k) to learn more.

Sources

- https://www.theladders.com/career-advice/the-average-401k-balance-by-age

- https://www.cnbc.com/2019/04/01/theres-a-retirement-crisis-in-america-where-most-will-be-unable-to-afford-a-solid-life.html

- https://www.cnbc.com/2019/04/01/theres-a-retirement-crisis-in-america-where-most-will-be-unable-to-afford-a-solid-life.html

- “Over 90% of Americans make this 401(k) mistake”, Mauri Backman, The Motley Fool

- Morningstar, 2013

- David Blanchet, Morningstar Analyst 2014, “The Impact of Expert Guidance on Participant Savings and Investment Behaviors”

- https://www.aon.mediaroom.com/new-releases?item=136959