3 Things to Do If You Can’t Max Out Your 401(k) This Year

Maxing out your 401(k) contribution every year helps your balance grow and may increase your chances of retirement with enough money to live comfortably.

However, $19,500 (the 2021 contribution limit) is quite a bit of money to stash away each year. Especially when you have a family to feed, bills to pay, and cash to save for emergencies.

If you can’t max out your 401(k) contribution limits this year, here are 3 actions you can take that may help you save more now for your future.

#1 Get the Company Match

If your employer offers a company match, take advantage of it. According to the Bureau of Labor Statistics, 60% of U.S. workers had access to a 401(k) plan in 2019, yet only 72% of those eligible participated.¹

While the report does not mention the exact number of investors who meet the company match, it does show 28% of eligible employees are missing out on saving pretax for retirement.

If you aren’t currently investing in your 401(k) or you aren’t at least getting the company match, you are missing out on free money.

Here’s the power in the company match:

Let’s say your company matches 100% up to 6% of your pay. With a $55,000 salary, you could put in 6%, or $3,300 for the year, and the company would match this at 100%.

That’s another $3,300 per year of free money that’s yours to keep. And this extra $3,300 does not include compounding your earnings – this is just the additional money you could be saving with your company match.

Don’t forget that employer contributions don’t count against your personal contribution maximum.

#2 Contribute More Than Last Year

Stretch yourself a little and save 1%, 2%, or 5% more than you did last year.

It may not seem like much, but it may make a big impact on your retirement nest egg because of compounding.

Let’s do some quick math to show you how easy it can be to find 1 – 5% extra and apply it toward retirement:

Let’s say you earn $65,000 a year, and you decide to save an additional 2% of your salary in the next 12 months. That’s an additional $1,300 per year, or $108.33 a month, to what you are currently contributing.

- Option A: If you are tight on cash, you could cut a streaming service at $50.99 a month and save the $611.88 annual streaming service cost for retirement. Find another $60 or so to cut from your budget each month for the next 12 months, and you meet your additional $108.33 retirement savings goal each month.

And you’ve done it without having to bring in more money.

- Option B: Find ways to earn more money so you can contribute more to your 401(k). Start a side hustle, ask for a promotion, or look for a new job with a higher salary. Then, adjust your regular contributions accordingly.

Should you get a raise this year, designate the extra income for retirement savings and directly put it into your 401(k). If you do this immediately when the raise takes effect, you won’t miss the extra money because you will never see it reflected in your bank account.

Remember, if you have a traditional 401(k), your contributions are made pretax, which reduces your taxable income – and how much you pay in taxes. This is yet another incentive to contribute more this year than you did last year.

#3 Get Professional Help

Studies continue to show that working with a financial advisor may increase your retirement income and greatly impact the type of retirement lifestyle you can afford.

From 2006 to 2012, Aon Hewitt and Financial Engines conducted a study comparing the returns of investors who sought help in the form of online sources or managed accounts to those who managed their 401(k)s themselves.

The study, which examined the 401(k) investing behavior of 723,000 workers at 14 large U.S. employers, concluded that people who got professional help earned higher median annual returns than those who invested alone.

In fact, “Participants who got Help received, on average, 3.32% (net of fees) more in return annually” than those who managed their own portfolios.²

Morningstar’s David Blanchet, Head of Retirement, CFP, CFA, published a 2014 study titled, The Impact of Expert Guidance on Participant Savings and Investment Behaviors.

The report revealed that participants who received expert guidance had as much as 40% more income during retirement versus those who received no help at all.³

The Vanguard Fund Group, Inc., conducted a 2019 study titled Advisor’s Alpha which found an 3% average increase in the value of portfolios of clients who work with a good financial advisor.⁴ This return, the study states, depends on the client’s situation and will vary from year to year.

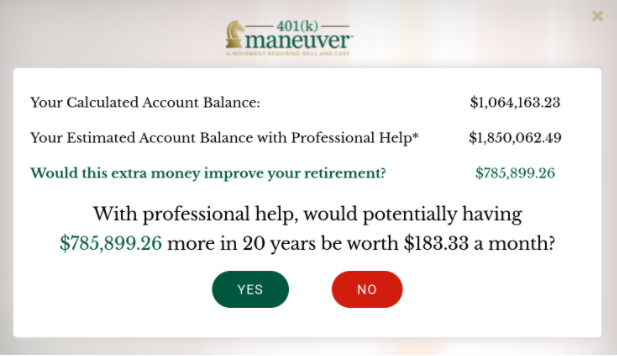

How Much Would 3% Impact Your 401(k) Account Balance?

We created a 401(k) calculator to help you see how professional account management may improve your 401(k) performance.

Let’s say you have an account balance of $275,000, and you expect 7% returns, and you have 20 years until retirement.

Using our 401(k) calculator, you would see that having professional help to properly rebalance your account may improve your retirement by $785,899.26!

The calculations do not include employer contributions or future salary deferrals. With those included, you can see that the difference has the potential to be much larger.

Check out our 401(k) calculator to see how much extra income you could have come retirement.

401(k) Maneuver provides independent, professional account management to help employees, just like you, grow and protect their 401(k) accounts.

Our goal is to…

- Help you have more money for retirement.

- Manage downside risk to minimize losses.

- Reduce fees that are hurting your retirement account performance.

With 401(k) Maneuver, you can go about your life doing what you love with confidence, knowing we are managing your account for you.

Have questions about your 401(k) performance? Book a complimentary 15-minute 401(k) strategy session with one of our advisors.

Book a 401(k) Strategy Session

Sources:

- https://www.cnbc.com/2020/02/24/how-much-money-you-give-up-if-you-dont-grab-employers-401k-match.html

- https://www.edelmanfinancialengines.com/press/2014/financial-engines-aon-hewitt-find-401k-participants-who-use-professional-help-are-better-off

- David Blanchet, Morningstar Analyst 2014, “The Impact of Expert Guidance on Participant Savings and Investment Behaviors”

- https://www.investopedia.com/articles/personal-finance/102616/how-much-can-advisor-help-your-returns-how-about-3-worth.asp