5 Must-Know Details about Your 401(k) Plan

If you’re confused by your 401(k) plan, you aren’t alone.

According to a J.P. Morgan 2021 Defined Contribution Plan Participant Survey, 401(k) investors are “overwhelmed and unsure about the various aspects of retirement planning.”¹

In fact, 52% feel they are presented with more plan information than they can absorb.²

Perhaps this is why 51% of 401(k) participants do not take time to read all the investment information provided by the plan.³

401(k) plans may be confusing, especially when you’re presented with a packet written in industry jargon and told to hurry up and make a decision about your financial future.

Understanding exactly what you’re enrolled in and why can be as easy as asking these 5 questions of your HR department or plan provider.

#1 What Is Your 401(k) Plan Vesting Schedule?

Vesting is nothing more than a fancy way of saying ownership.

The money you contribute to your 401(k) each pay period is 100% vested and yours to keep. What your company matches is a different story.

Vesting is your legal right to keep what your employer contributes as a company match.

Depending on your 401(k) plan’s vesting schedule, you may not own the money your employer contributed until you are fully vested.

There are 3 types of vesting schedules.

#1 Immediate – This means you own your employer contribution as soon as you receive it in your 401(k) account.

#2 Graded – This means you vest a certain percentage of your employer matching dollars in a set period of time, until you are 100% vested. By law, employers must vest employees at least 20% at the end of 2 years, and another 20% annually each year thereafter.

#3 Cliff – Some companies require you to stay employed for a specific amount of time before the money your employer contributed is yours. This is known as cliff vesting. Employers have up to 3 years to vest employees with a cliff vesting schedule.

If you don’t know your 401(k) plan’s vesting schedule, call HR or your plan provider and find out.

Because, if you decide to leave the company after 2 years and have a 401(k) plan that has a cliff vesting schedule that requires you to work 3 full years before you are 100% vested, you will lose the money your company contributed.

[Related Read: What Every Investor Needs to Know about 401(k) Vesting]

#2 What Is Your Company Match?

A 401(k) company match is money your employer contributes to your account based on your contribution amount and is usually capped at a certain percentage of your income.

There are different matching structures, and it’s important to know what yours is so you can maximize the amount of free money your company matches.

Some companies offer dollar-for-dollar matches. This means the employer matches $1 for every $1 you contribute, up to a certain amount.

The more common type is the partial matching of percentages. This means the company matches a percentage, or portion of what you contribute, up to a certain amount.

If you aren’t taking advantage of company matching, you might as well be throwing away free money. Contact HR or your plan provider to find out the type and amount of your company’s match.

#3 What Are Your Investment Options?

Many companies’ 401(k) plans use target date funds (i.e., 2030, 2040, or 2050 funds) as their default option, automatically enrolling employees in them.

They can do this thanks to the Pension Protection Act of 2016, which allows employers to direct plan participants’ assets into a target date fund and not be liable should the employee not select an investment.

According to Marketwatch, “About 70% of U.S. companies automatically enroll employees into 401(k)-type plans, and more than 86% of these firms now direct people’s money by default into ‘target-date funds’ (TDFs).”⁴

Target date, or lifestyle, funds are supposed to automatically adjust account allocations throughout life.

Investors are grouped solely based on their expected retirement date. This means target date funds do not take into consideration an investor’s…

- Location

- Profession

- Salary

- Risk tolerance

- Retirement goals and objectives

The reality is that target date funds will often underperform in good markets and do a poor job of managing downside risk during tough markets.

According to Morningstar analyst Jeffrey Holt in March 2018, “In the long run, the biggest risk in target-date funds is that they won’t meet investor expectations for avoiding losses.”⁵

A recent article indicated that, on average, target date funds invested 75% in common equity, generating average losses of over 30% during the 2008 financial crisis.

Investors planning to retire in 2010 suffered significant losses because 2010 target date funds increased their common equity exposure in 2007.⁶

The good news is, you don’t have to stay with the default option.

Now that you know why you might want to avoid target date funds, the first step is to find out if you were automatically enrolled in a target date fund or not.

If you are, then, your second step is to find out what other 401(k) investment options are available to you.

Check out this video to learn more on how to choose investments for your 401(k).

#4 What Is the Cost of Your 401(k) Investment Options?

Your 401(k) comes with various fees that, when added up, may get pricey and have an impact on your 401(k) return over time.

The good news is the U.S Department of Labor requires 401(k) providers to disclose all fees in the prospectus you’re given when you enroll in a 401(k). They also require the information be updated and shared every year to reflect fee changes.

When it comes to investment option fees, some funds have lower expense ratios than others.

We recommend asking your plan provider for the disclosure that shows how much of your return is deducted for the investment’s annual cost. Contact your plan provider or HR and specifically request the 401(k) fee disclosure 408(b)(2) section.

#5 How Do I Change My 401(k) Investments?

Understanding how to change your 401(k) investments is important if you want to maximize your returns.

Adjusting your account allocations (or rebalancing) is the process of realigning the weightings of the assets (your investments) in the portfolio.

This can involve periodically buying and/or selling assets in the portfolio in order to maintain the initial desired level of asset allocation.

Understanding how to rebalance is critical because things change and you want your account to reflect these changes.

For example, your risk tolerance may change. Market conditions change, as do tax regulations.

If you aren’t rebalancing, you may run the risk of unmanaged allocations experiencing much larger losses in down markets and miss the opportunity for growth during good markets.

Make sure to ask the following questions of your 401(k) plan provider:

- Can I make changes to my investments online?

- Do I have to go through the plan provider or fill out a form?

- How often am I able to make changes?

[Related Read: What Every Investor Needs to Know about Rebalancing a 401(k)]

It’s not only important to know how to make changes to your investment menu, but you also need to know how to review and verify these changes to ensure they’re accurate.

If you are able to verify online, make sure you have access to this information and understand what it is that you’re looking at.

Where to Get Professional 401(k) Account Management

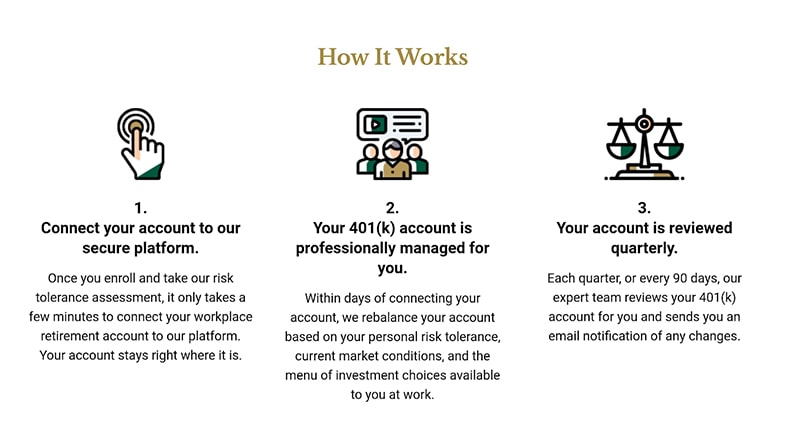

401(k) Maneuver exists to help employees grow and protect their 401(k) accounts. We provide independent, personalized professional account management to help employees, just like you, grow and protect their 401(k) accounts.

And we do this without in-person meetings so you don’t have to drive to an appointment or spend hours preparing for the meeting.

Our done-for-you, virtual service allows you to keep your 401(k) right where it is while we review and rebalance your account based on your risk tolerance and current market conditions.

All you need to do is to connect your account to our secure platform, and we manage your account for you. There’s no need to move your account – you can keep it right where it is.

As a fiduciary, we are bound by law to put your interests first, and we do not receive commissions on the trade.

Watch this short video on how it works and how 401(k) Maneuver may help you increase your account performance.

Have questions about your 401(k) performance? Book a complimentary 15-minute 401(k) Strategy Session with one of our advisors.

Book a 401(k) Strategy Session

Sources

- https://am.jpmorgan.com/us/en/asset-management/adv/insights/retirement-insights/defined-contribution/plan-participant-survey/

- https://am.jpmorgan.com/us/en/asset-management/adv/insights/retirement-insights/defined-contribution/plan-participant-survey/

- https://am.jpmorgan.com/us/en/asset-management/adv/insights/retirement-insights/defined-contribution/plan-participant-survey/

- MarketWatch, Opinion: Target-date funds are more expensive and less effective than this simple investment plan, February 20, 2019

- Special Report: Fidelity puts 6 million savers on risky path to retirement, Reuters.com March 5, 2018

- The Global Financial Crisis and the Performance of Target-Date Funds in the United States – October 1, 2011