What Every Investor Needs to Know about Rebalancing a 401(k)

If you are like many working Americans with a 401(k), rebalancing your 401(k) is probably not one of your top priorities. You have better things to think about. We get it.

But, what if we told you that by failing to rebalance, you are essentially turning your investments (and your future retirement income) over to chance.

Failing to regularly rebalance your 401(k) portfolio often results in significant losses during bad markets and opens you up to more risk exposure than you initially intended.

And, you may be missing out on earning more and keeping more of your retirement savings–which means you may need a part time job to make ends meet during retirement.

The cold hard truth is this: Financial ignorance can be very costly.

And with 401(k)s being the biggest asset many people have, it’s worth your while to become an informed investor.

If you aren’t, who else will be? It’s up to you to make sure you have enough money for retirement.

It’s not your employer’s job either. It’s your money. Your 401(k) plan. Your financial future.

Keep reading to discover what rebalancing your 401(k) looks like, why rebalancing may boost your account performance, and steps you can take today to maximize your retirement savings.

What Does It Mean to Rebalance Your 401(k)?

Rebalancing your 401(k) is the process of realigning the weightings of the assets, or investments, in your portfolio.

This means you periodically buy or sell assets in your portfolio in order to maintain the initial desired level of asset allocation.

Let’s say you set up and invested money in your 401(k) in 2012, and your original asset allocation target was to have 60% to stocks and 40% invested in bonds. And let’s say the stocks performed well over this period of time. If you never rebalanced your account and stocks performed far better than the bonds, you’d have much more money invested in stocks. This may increase your asset allocation to 80% of your portfolio in stocks and only 20% in bonds.

While your account may have posted high returns during this period, you are now at a higher risk level than you originally selected.

And, should the market drop and stocks take a dive, your retirement savings could potentially suffer major losses and you might lose some (or a lot) of your hard-earned retirement savings.

In this example, to return to your initial 60/40 target weighting, you would need to sell some of your stocks and purchase more bonds.

It’s important to note that rebalancing is not the same thing as reallocation.

Reallocation is when you change the percentage of invested assets in different asset classes to balance risk versus reward. Or, in other words, reallocation is about how much risk you want to take. In order to help investors grow their account, while at the same time keeping risk in check, an asset allocation strategy is often put in place.

We recommend rebalancing your 401(k) account quarterly, or four times a year. Doing so helps you stay within your risk level and protect against potential losses.

We also recommend reviewing your 401(k) statement when it arrives.

Watch the video below to see how to read a 401(k) statement.

How Rebalancing Your 401(k) May Increase Retirement Savings

Few people rebalance their 401(k) account, and even those who do fail to manage risk through proper asset allocation. Rebalancing only the percentages of current holdings does not consider current market and economic conditions.

This may result in more significant losses during down markets and missed opportunity for growth during good markets.

If you aren’t rebalancing your account allocations, you may be missing out on earning more and keeping more of your hard-earned retirement savings.

Yet, 80% of 401(k) investors fail to rebalance.¹

Many investors are unaware they can go into their account and rebalance to keep their portfolio on track for retirement.

This might stem from the belief that retirement is a long game, and, if you have a 401(k), you’re a long-term investor. Therefore the reasoning goes, a “buy and hold” strategy is best.

This may be why so many investors make their initial allocation selection when they set up their 401(k), and then largely ignore their account–except for occasionally checking the balance.

Sadly, this strategy given in the past doesn’t always benefit the average 401(k) investor and protect them from potential losses.

Rebalancing Your 401(k) Is Critical to Your Retirement Future

Morningstar conducted a study of the top 100 best performing mutual funds between January 1, 1998, and December 31, 2013.

The study revealed that, in any given year of the top 100 best performing mutual funds in any of those years, in the very next year about half of the time, 8 of the top 100 remained in the top 100 the very next year.²

That study tells us as investors that it’s not very wise to continue using an antiquated “buy and hold” strategy.

A “buy and hold” strategy doesn’t take into consideration changing market conditions, tax policy, consumer spending habits, and trade policy. Investments you chose months ago may no longer be in your best financial interest.

In fact, failing to rebalance may leave you exposed to risk.

“The buy and hold strategy was great decades ago when the stock market and investments were less impacted by news cycles, and they were really more impacted by market fundamentals and consumer buying habits,” says Matthew Jackson, a partner at 401(k) Maneuver. “But in today’s 24-hour news cycle, the buy and hold strategy just isn’t as effective today as it was decades ago.”³

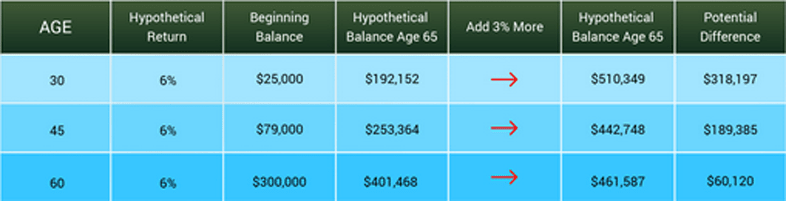

Recent studies show that investors who get professional help rebalancing their account may receive more than 3% in additional annual return over time.

The Vanguard Fund Group published a 2019 study titled Advisor’s Alpha, which reported a 3% average increase in the value of portfolios of clients who work with a good financial advisor and have their accounts regularly rebalanced.⁴

Aon Hewitt and Financial Engines conducted a study from 2006 to 2012 comparing the returns of investors who sought help in the form of online sources or managed accounts to those who managed their 401(k)s themselves.

The study examined the 401(k) investing behavior of 723,000 workers at 14 large US employers and showed that people who received professional help earned higher median annual returns than those who invested alone.

In fact, “Participants who got Help received, on average, 3.32% (net of fees) more in return annually” than those who managed their own portfolios.⁵

3% more can add up to a ton of extra money. Potentially hundreds of thousands of dollars over time.

The chart below shows you what ignoring your 401(k) account–and failing to rebalance–could potentially mean in actual dollars to your future.

What would an extra couple hundred thousand dollars mean to your lifestyle during retirement?

Really think about that for a moment.

- Would you be able to sleep better at night knowing you won’t have to scrape by?

- Would you be able to take luxury vacations instead of staycations?

- Would you be able to spend more time doing what you love rather than working a part-time job to make ends meet?

Check out our retirement calculator to see how much you may have at retirement, and how 3% may improve your 401(k) performance.

Getting Help Rebalancing Your 401(k)

Not regularly rebalancing your 401(k) has the potential to do real harm over time to your retirement nest egg.

The investment choice you made 3 months ago may not be the best today if there is a change in economy, trade/tax policy, or consumer sentiment.

If you aren’t rebalancing your 401(k) at least four times a year, you may be cheating yourself out of better returns.

Sadly, many investors don’t know they can get independent help to rebalance their portfolio.

Others fail to reach out for professional help because they think they don’t have a large enough account balance or they are too close or too far away from retirement.

It doesn’t matter how old you are, how close to retirement you are, or how much money you have saved…

With 401(k) Maneuver, optimizing your 401(k) each quarter has never been easier. We are shifting the “buy and hold” paradigm that may be preventing investors like you from maximizing your 401(k) retirement savings.

401k Maneuver is a secure online tool that provides 401(k) investors independent and professional investment help.

We are real people who make changes to your 401(k) account on a quarterly basis with the goals in mind of…

- Increasing account performance over time.

- Managing downside risk to minimize losses.

- Reducing fees that harm account performance, so you may keep more of your hard earned money.

When you join the Maneuver Nation, you will receive professional quarterly 401(k) account reviews every 90 days and rebalancing that is personalized to your tolerance to risk based on current economic and market conditions.

You don’t have to do a thing because we handle everything for you!

And the best part? You never have to spend your valuable time meeting with a financial representative.

See how 401(k) Maneuver may potentially improve your account performance.

Not ready to commit? No worries. Check out or no-cost guide 5 Mistakes You Want to Avoid with Your 401(k) and discover how you can keep more of your hard-earned money.

Sources:

- “Over 90% of Americans make this 401(k) Mistake.” Mauri Backman, The Motley Fool.

- The Impact of Expert Guidance on Participant Savings and Investment Behaviors. David Blanchett, Morningstar Investment Management Group, 2014.

- https://issuu.com/advisorsmagazine/docs/issue_94/18

- https://www.vanguard.com/pdf/ISGQVAA.pdf

- https://www.edelmanfinancialengines.com/press/2014/financial-engines-aon-hewitt-find-401k-participants-who-use-professional-help-are-better-off