7 Retirement Investment Mistakes to Avoid and What to Do Instead

#1 Not Having a Plan for Retirement

If you don’t have a clear path to where you want to be in retirement, you’re probably not going to end up there.

This may sound obvious, but many people fail to set a plan for retirement.

For some, it may be because they think their account balance isn’t big enough, so why bother. For others, they think they are too close to retirement to plan at this point. And then there are those who think they don’t have to think about it right now because they just entered the workforce.

Whatever the case, if you don’t create a plan NOW (no matter your age), chances are, you aren’t going to have enough money to comfortably retire.

With rising healthcare costs, inflation, taxes, down markets, and other unknown future variables, one thing is certain: if you don’t have a plan and take action on that plan now, you’re likely not going to have enough to retire.

Or worse, you’ll end up with so little saved that you might have to struggle to survive.

So, do you know how much you will need to retire?

If not, sit down and figure out what you will need to maintain your standard of living when you stop working.

If you don’t know, reach out to an expert who can help you figure out a solid plan.

#2 Not Regularly Looking at Your Statements

Many employees are apathetic about their retirement savings and don’t even open their 401(k) or other workplace retirement plan statements. When statements come in the mail each month, they toss them in the trash.

Rather than managing their 401(k), too many people hope they’ll have enough saved for retirement.

Although reviewing the statement for your 401(k) plan might not be the most exciting read, it is important that you have a good understanding of the information that is provided to you.

Opening and reviewing your statements also helps you determine whether or not you’re on track to meet your financial goals.

Do you open your statement every month? And, do you understand why you get what you get?

If the answer is no to both questions, we recommend you become engaged with your retirement savings. Open your statements.

Watch the video below to see how to read a 401(k) statement.

#3 Not Saving the Maximum Contribution Limit

A question we at 401(k) Maneuver™ get asked a lot is, “Am I on track for retirement based on what I have saved so far for my age?”

It’s an excellent question. And one you should ask yourself as well.

If you aren’t thinking about your retirement income now and the lifestyle you want when you retire, and have a plan on how to meet your goals, chances are you’ll be like too many Americans and NOT be on track for a comfortable retirement.

According to a Fidelity Investments study in 2018, out of 16.2 million 401(k) participants, only 187,000 had over a million dollars in their 401(k).¹

With healthcare costs rising and tax rules being unknown in 5, 10, 20 years, it’s crucial to have enough money saved to comfortably retire.

Let’s say you had almost $200,000 average balance at retirement age, and you were making $50,000 per year at your job when you retired. How long do you think these funds are going to last you in retirement?

Will this give you the retirement you truly desire?

For most, the answer is no. Not even close!

There is one way that may ensure you have enough to live on during retirement… contribute the maximum amount in any given year.

Even if you are 50, it’s not too late to do what you can to save the most allowed, as it will greatly impact the amount you have at retirement.

In 2019, the annual contribution limit has been raised to $19,000 for 2019 for employees who participate in 401(k), 403(b), most 457 plans, and the federal government’s Thrift Savings Plan. This is $500 over 2018.

For employees age 50 or older in the plans listed above, the additional contribution limit will stay the same for 2019 at $6,000. This means the annual contribution limit is $25,000 for those 50 or older.

Remember, if you don’t invest in your future, no one else will do it for you. So sit down, review your statements, and see if you can contribute more than you are now.

Your future self will thank you for it!

#4 Not Putting In Enough to Get the Full Company Match

If you can’t max out the annual contribution limits for a given year, at least put in enough to get the full company match.

Company matching is one of the secrets to maximizing your 401(k) or workplace retirement account, and it’s often the most overlooked.

According to Vanguard’s How America Saves,² only 13% of employees with retirement plans at work saved the then-maximum 401(k) contribution limit of $18,000 in 2017.

And only 14% of those 50 or older took advantage of plans offering catch-up contributions.

At 401(k) Maneuver™, we cannot stress enough how important it is that you contribute at least the minimum of what your company will match.

Because when your company matches you, it’s like getting free money, folks!

If you aren’t doing it already, you may be leaving a lot of money on the table.

Just sit back and imagine what your retirement could look like with all this extra free money added to it…

Putting in the company match may increase your retirement lifestyle. And it may help you accumulate the amount of money you desire at retirement.

So why not do it?

Remember, you don’t have to wait for enrollment season to make changes to your 401(k) election. You can make changes anytime during the year!

#5 Relying Only on Target Date Funds

While target date funds have become extremely popular with 401(k) participants in the past few years, it is essential that you diversify your account, and not rely solely on these financial vehicles.

Why?

Because target date funds are based on the date of retirement, they fail to take into consideration that not all investors are created equal.

If you’re younger and plan to retire in 2060, you’re told to select a 2060 fund. If you’re wanting to retire in 2030, you’d select a 2030 target date fund.

What this means is that investors are grouped solely based on their expected retirement date–location, age, profession, salary, risk tolerance, goals, and objectives are NOT taken into consideration.

Because everyone has different goals and objectives for the future, there is no one-size-fits-all way to invest in a 401(k) plan.

In addition, target date funds do not appropriately manage downside risk.

They may often underperform in good markets and do a poor job of managing downside risk during tough markets.

If you are currently in a target date fund, we suggest moving away from this option and better utilizing all the options available in your workplace retirement plan.

Click here to download our guide 5 Ways Target Date Funds Fail to Live Up to Their Promise

#6 Not Rebalancing Your Account Allocations Quarterly

Contrary to what some investors believe, a 401(k) plan or other workplace retirement plan is not a “set it and forget it” program.

And, just like driving cross-country, if there is a roadblock or other obstacle preventing you from reaching your destination, you need to make the appropriate changes in order to stay on course.

A lot of people we speak with think their employer is taking care of their 401(k) for them.

But it’s not true.

It’s your money. It’s your account. It’s up to you to make changes.

Because of this belief few people rebalance their 401(k) account, and even those who do fail to manage risk through proper asset allocation.

In fact, 80% of 401(k) investors fail to rebalance.³

Rebalancing only the percentages of current holdings does not consider current market and economic conditions. The stock or mutual fund that you chose last year–or even last quarter–may or may not necessarily still be going in the right direction for you.

Not rebalancing also often results in more significant losses during bad markets.

With that in mind, properly allocating and rebalancing your retirement account–based on your specific objectives–can be extremely advantageous.

Successful 401(k) investors rebalance their account allocations every quarter, or four times a year…and we recommend you do the same.

Click here to download our guide on how to Supercharge Your 401(k) performance.

#7 Not Seeking Expert Guidance

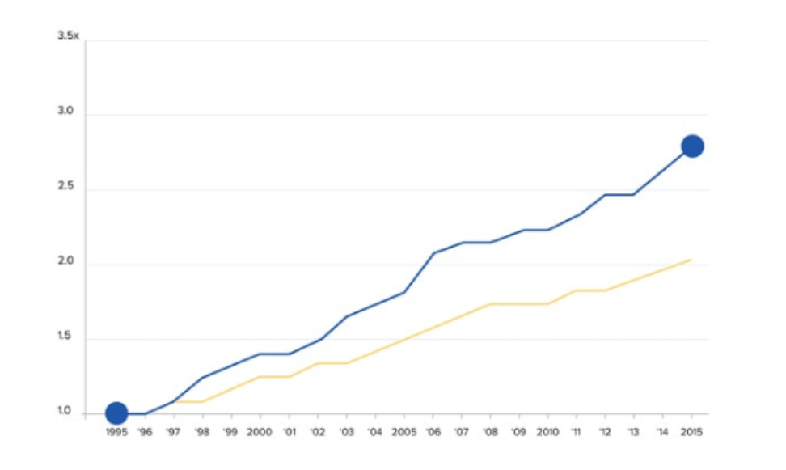

A May 2014 study conducted over a 6-year period compared those who had help with managing their 401(k) and those who did not. The study revealed…

“On average, the median annual returns for participants in the study who got help were more than 3% 5 (332 basis points, net of fees) higher than people who didn’t get help.”⁴

From the graph above, you can see getting expert help with your 401(k) or other workplace retirement account can be beneficial to life at retirement.

Think of it this way…You wouldn’t make major health decisions without the advice of a doctor.

So, why turn what could be your largest financial asset over to chance?

If you’d like to take control of your financial future and have more income at retirement, we strongly suggest getting third-party advice sooner rather than later.

Want to further optimize your workplace retirement account? Download our GUIDE How to Supercharge Your 401(k) Performance Today.

Sources

- https://www.theladders.com/career-advice/the-average-401k-balance-by-age

- How America Saves 2018: Telling the retirement story with data

- “Over 90% of Americans make this 401(k) mistake”, Mauri Backman, The Motley Fool

- AON Hewitt “Help in Defined Contribution Plans: 2006 through 2012” Published May 2014

- http://www.aon.mediaroom.com/new-releases?item=136959