5 Things That May Boost 401(k) Savings in Your 50s

With volatile markets and soaring inflation, can you still boost 401(k) savings in your 50s?

You bet you can. And you don’t have to invest a ton more to do it.

Obviously, if you really want to boost 401(k) savings in your 50s, the solution is to contribute the maximum this year and every year until retirement.

But this isn’t always possible. And it’s getting harder for many investors to contribute more due to the high inflationary environment we’re currently in.

That’s why we’ve put together a list with 4 out of the 5 tips that don’t require you to invest more money. Keep reading for 5 ways to boost 401(k) savings in your 50s.

#1 Take Advantage of Catch-Up Contribution Limits

Doing what you can now to meet contribution limits will help boost 401(k) savings in your 50s.

Employee contribution limits for 401(k), 403(b), most 457 plans, and the federal Thrift Savings Plan are $20,500.

The 401(k) catch-up contribution for investors 50 years and older is $6,500 for 2022. (If you turn 50 anytime during December of 2021, you’re still eligible to contribute the additional $6,500.)

That means you can save up to $27,000 this year.

How much you can realistically contribute to your 401(k) depends on how much you earn and the amount of debt you carry, among other factors.

Do what you can to save as close to the 401(k) contribution limits as possible: Cut monthly spending, postpone discretionary large purchases, or pick up a side hustle.

[Related Read: Retirement Plan Contribution Limits for 2022]

#2 Avoid Target Date Funds

Perhaps when you signed up for your 401(k) plan, you were automatically enrolled into a target date fund (such as a 2030 or 2040 fund).

If so, you may want to reconsider this option.

Target date funds are structured to automatically reallocate as you move through different life stages.

As you age toward your target retirement date, the funds shift toward more conservative investments to protect your money.

If you’re wanting to retire in 2030, you would be told to select a 2030 target date fund.

What this means is investors are grouped solely based on their expected retirement date–location, age, profession, salary, risk tolerance, goals, and objectives are not taken into consideration.

Because they are based on the date of retirement, target date funds fail to take into consideration that not all investors are created equal.

Basically, investing in target date funds and not actively managing your retirement account is equivalent to saying there’s a one-size-fits-all investment strategy that works for everyone.

This doesn’t pass the common sense test.

Another reason we recommend investors avoid target date funds is because they are riskier than many people perceive.

Citing studies by institutional advisory firm Research Affiliates, Barron’s associate editor Randall W. Forsyth wrote in a February 2019 article, “They [the studies] show that the standard ‘glide path’ of target-date funds, which start heavily weighted in stocks and reallocate to bonds in later years, doesn’t produce the desired results.”¹

According to Rob Arnott, chairman of the board of Research Affiliates:

“You now have a trillion-dollar industry based on ideas that were never tested.”²

An article titled Global Financial Crisis and the Performance of Target-Date Funds indicated that on average, target date funds (like 2030 or 2040 funds) invested 75% in stocks, generating average losses of over 30% during the 2008 financial crisis. Investors planning to retire in 2010 suffered significant losses because 2010 target date funds increased their common equity exposure in 2007.³

Former Morningstar analyst Jeff Holt commented, “In the long run, the biggest risk in target-date funds is that they won’t meet investor expectations for avoiding losses.”⁴

By rebalancing your retirement account, you lower the risk of your account underperforming due to target date funds that may not manage downside risk.

However, if you can, we recommend moving away from this option and better utilizing all the options available in your workplace retirement plan.

Download our guide 5 Ways Target Date Funds Fail to Live Up to Their Promise.

#3 Delay Retirement

While you may not like the idea, delaying retirement a few years may significantly help boost 401(k) savings in your 50s.

Let’s say you are 55, have $300,000 saved, and want to retire at 65.

If you contribute, starting this year, $1,500 per month and earn a 7% annual rate of return, you’ll have a total of $862,526 saved after 10 years.

If you delay retirement by 5 years (to 70), and continue contributing $1,500 per month earning a 7% return, you’ll have saved a total of $1,330,127.

See how delaying retirement just a few years has the potential to significantly boost 401(k) savings?

#4 Regularly Rebalance Your Investments

If you’re a 401(k) investor that follows a set-it-and-forget-it strategy with your 401(k), we encourage you to rethink this advice…especially if you want to boost 401(k) savings in your 50s.

A buy-and-hold strategy often causes investors to potentially miss out on earning more and keeping more of their hard-earned retirement savings.

The investments you initially chose to help you meet your retirement goals – whether that was 2 years ago or 1 month ago – may no longer be the best alternatives for you now.

When you take into consideration changes in economic and market style conditions and investment style performance, trade policy, and consumer sentiment, well…investments that were right for you in the past may not be now.

Morningstar conducted a study that monitored the top 100 best-performing mutual funds between January 1, 1998, and December 31, 2013.

This study revealed that, in any given year of top best-performing 100 mutual funds in any of those years, in the next year, about half of the time, 8 out of 100 remained in the top 100 the very next year.⁵

This is why we recommend you rebalance your 401(k).

Rebalancing is the process of realigning the weightings of the assets (your investments) in the portfolio.

This can involve periodically buying and/or selling assets in the portfolio in order to maintain the initial desired level of asset allocation.

Maintaining an even distribution of assets – such as 50% stocks and 50% bonds–is also a key objective. This is why rebalancing your portfolio may need to take place from time to time throughout each year.

Discover why account balancing and allocation may affect 401(k) performance.

#5 Seek Professionally Managed Help

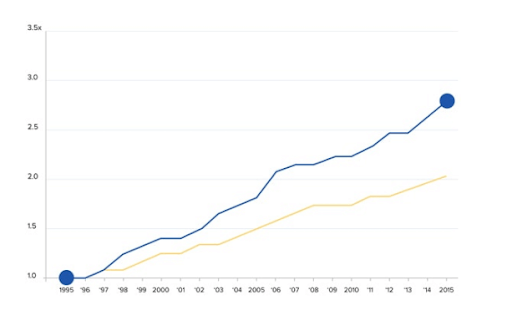

A May 2014 study conducted over a 6-year period compared those who had Help with managing their 401(k)s and those who did not. The study revealed…

“On average, the median annual returns for participants in the study who got Help were more than 3% (332 basis points, net of fees) higher than people who didn’t get Help.”⁶

From the graph above, you can see getting professional help with your 401(k) or other workplace retirement account can be beneficial to life at retirement.

Think of it this way…if you had heart issues, you wouldn’t make major health decisions without the advice of a cardiologist.

So, why turn what could be your largest financial asset over to chance?

If you’d like to take control of your financial future and potentially have more income at retirement, we strongly suggest getting third-party advice.

If you’re hesitant to reach out for advice because you think your account balance isn’t big enough, or you think you’re too close to retirement to get help, don’t let that stop you!

401(k) Maneuver provides professional account management with the goal to help you grow and protect your 401(k).

Our goal is to increase your account performance over time, manage downside risk to minimize losses, and reduce fees that harm your account performance.

There are no time-consuming in-person meetings and nothing new to learn, and you don’t have to move your account.

Simply connect your account to our secure platform, and we regularly review and rebalance your account for you, when necessary. Check here to learn more about how it works.

If you have questions about your 401(k) or if you need help, we’re here for you. Click below to book a complimentary 15-minute 401(k) Strategy Session.

Book a 401(k) Strategy Session

Sources:

- MarketWatch, Opinion: Target-date funds are more expensive and less effective than this simple investment plan, February 20, 2019

- MarketWatch, Opinion: Target-date funds are more expensive and less effective than this simple investment plan, February 20, 2019

- The Global Financial Crisis and the Performance of Target-Date Funds in the United States – October 1, 2011

- Special Report: Fidelity puts 6 million savers on risky path to retirement, Reuters.com March 5, 2018

- The Impact of Expert Guidance on Participant Savings and Investment Behaviors. David Blanchett, Morningstar Investment Management Group, 2014.

- AON Hewitt “Help in Defined Contribution Plans: 2006 through 2012” Published May 2014