6 Possible Ways to Maximize 401(k) Performance in 2020

With the New Year comes the desire to do more, be better, live healthier, and, yes, even contribute more to retirement savings. If you’re wanting to see your savings grow, keep reading for 6 possible ways to maximize your 401(k) performance in 2020.

#1 Become an Engaged Investor

Too many people don’t understand what they are investing in.

Others don’t know how to read their 401(k) statement when it comes in the mail.

There are even some who think their employer takes care of their 401(k) for them.

The ugly truth is this: financial ignorance is costly.

If you aren’t engaged with your investments, no one else will be. It’s your money. Your accounts. Your financial future.

And it’s up to you to make sure you have enough money for retirement.

How you do this starts with a decision to take control of your financial future.

From there, do what you can to educate yourself…

- Continue reading blogs like this.

- Attend seminars and online trainings.

- Read books on the subject.

- Consult a third-party expert.

Do whatever you can to gain the knowledge you need to make the best decisions regarding your money. Once you start to educate yourself, it won’t be difficult for you to understand.

Your future self will thank you for it!

#2 Try to Maximize Your 401(k) Contribution Limit

Employee 401(k) contribution limits have gone up for 2020 to $19,500.

This applies to 401(k), 403(b), most 457 plans, and the federal Thrift Savings Plan.

For those age 50 and older, the 401(k) catch-up contribution limit will also increase $500–from $6,000 in 2019 to $6,500 in 2020.

This means if you’re 50 or older and need to catch up on retirement savings, you’ll be able to save $26,000 in your 401(k) in 2020. If you turn 50 anytime during December of 2020, you’re still eligible to contribute the additional $6,500.

If maximizing your 401(k) contribution limit is too much of a stretch for you, do what you can to get close to it.

Even saving an additional $50 or $100 each pay period may make a big difference in retirement because that money will grow over time.

If you were planning on setting aside 6% of your $70,000 salary, or $350 each month–and did it consistently throughout the year–you’d end 2020 contributing $4,200 to your 401(k).

Now, if you stretched yourself a bit and saved an additional $100 each pay period during 2020–and you get paid twice a month–you’d have an additional $2,400 contributed.

Just by saving an additional $100 each pay period, you’d end the year saving a total of $6,600.

If you’re 49 years old and younger, that’s about a third of the $19,500 maximum contribution limit!

What can you do to save 1%, 3%, or more each pay period?

We recommend reviewing your budget to see what expenses you can cut, and then take the money saved and put it in your 401(k).

Here’s the thing: you don’t have to suffer or “get by” to stretch yourself to save a bit more.

Take a look at these two examples:

- Dining out during the workweek: Let’s say you spend on average $10 on lunches three times a week. If you packed your lunch instead of going out, that’s $120 a month/$1,440 a year you could easily save just by changing your behavior.

- Cutting back on subscription services: Let’s say you have a TV streaming subscription for $44.95/month. If you cut that back to the basic plan at roughly $12/month, you could save $395 a year.

You can save even more if you cancel subscriptions, start mowing your own lawn, or limit the amount you spend on clothing.

Saving for retirement is a long game.

The actions you take today, this month, this year may greatly impact your life in retirement and maximize your 401(k) performance in 2020.

#3 Contribute at Least the Company Match

An easy way to maximize your 401(k) performance in 2020 is to contribute–at a minimum–what your company will match.

If you aren’t currently contributing what your company matches, you may be leaving a lot of money on the table…

Because company matching is like getting free money.

In some cases, it may double the amount of what you’re already saving and may increase your retirement lifestyle.

Let’s say your company matched 100% up to 6% of your pay.

With a $40,000 salary, you could put in 6% or $2,400 for the year, and the company would match this at 100%.

That’s $2,400 per year of free money that will help you grow your retirement savings and help you maximize your 401(k) performance over time.

#4 Roll Over Old 401(k) Plans

If you’ve recently changed employers and had a 401(k) plan with them or if you changed jobs years ago and have a 401(k) with an old employer, we recommend you roll it over.

It’s your money, and it’s yours to manage.

Whether you have one 401(k) account you left with a past employer, or have two or three of them, leaving them behind may result in overlapping funds that may not suit your tolerance for risk.

Also, rolling over an old 401(k) into one account may help you better track your investment growth and may potentially reduce the overall fees you pay.

While you may be able to leave your 401(k) account with your previous employer, there are some disadvantages to doing so:

- Your account will remain subject to plan rules.

- You may continue to have limited investment options.

- You will have another account to keep up with.

A better option would be to roll your old 401(k) into your new employer’s 401(k) plan, providing it’s allowed, or roll it into an IRA.

Just make sure to choose a plan with the lowest, most manageable fees. Or seek third-party advice to help you make the best rollover decision possible.

Avoid these 5 irreversible and costly 401(k) rollover mistakes. Click here to download your free guide .

#5 Rebalance Your 401(k) Four Times a Year

If you’ve been told a set-it-and-forget-it strategy is best when it comes to your 401(k), you may want to rethink this advice.

Saving for retirement is a long-term game.

However, this buy and hold strategy often causes investors to potentially miss out on earning more and keeping more of their hard-earned retirement savings.

The investments you initially chose to help you meet your retirement goals–whether that was 5 years ago or 5 months ago–may no longer be the best alternatives for you now.

Changing market conditions, trade policy, and consumer sentiment may affect your investments–and what was right for you in the past may not be now.

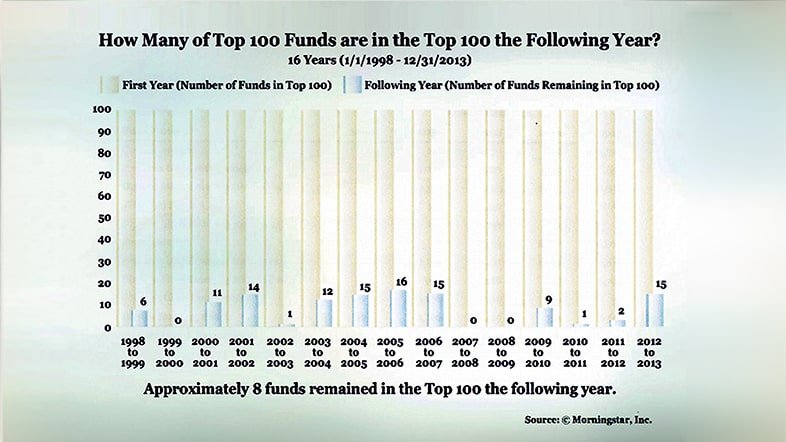

Morningstar conducted a study that monitored the top 100 best-performing mutual funds between January 1, 1998, and December 31, 2013.

This study revealed that, in any given year of top best-performing 100 mutual funds in any of those years, in the next year, about half of the time, 8 out of 100 remained in the top 100 the very next year!¹

This is why we recommend you rebalance your 401(k) quarterly, or four times a year.

Rebalancing is the process of realigning the weightings of the assets (your investments) in the portfolio.

This can involve periodically buying and/or selling assets in the portfolio in order to maintain the initial desired level of asset allocation.

Maintaining an even distribution of assets–such as 50% stocks and 50% bonds–is also a key objective.

Therefore, a rebalancing of the portfolio may need to take place from time to time throughout each year.

Discover why account balancing and allocation may affect 401(k) performance. Download your no-cost guide today.

#6 Choose the Right Investments for Your 401(k)

Rebalancing, while important to your 401(k) performance, can take time and effort.

This is why, throughout the years, many employer-sponsored retirement plans have touted the benefits of target date funds, also referred to as lifestyle funds and retirement date funds (you may know them as 2030, 2040, and 2050 funds).

In fact, many companies resort to these types of funds as the “default” option simply based on a person’s retirement date.

Just because something is easy, it doesn’t mean that it’s the right option for everyone.

In fact, using a “standardized” portfolio allocation may potentially be detrimental to investors.

Individual investors should ideally have customized solutions that are based on their specific goals and risk tolerance.

This doesn’t mean target date funds aren’t more beneficial for some investors than others.

But for a majority of investors, there can be a downside .

Studies show that target date funds will often underperform in good markets and often do not do a good job of managing downside risk during tough markets.

A recent article indicated that, on average, target date funds invested 75% of asset allocation in common equity, generating average losses of over 30% during the 2008 financial crisis.

Investors planning to retire in 2010 suffered significant losses because 2010 target date funds increased their common equity exposure in 2007.²

According to Morningstar analyst Jeffrey Holt in March 2018, “In the long run, the biggest risk in target-date funds is that they won’t meet investor expectations for avoiding losses.”³

If you are currently in a target date fund, we recommend you rethink this strategy.

Or, at least look inside your fund’s portfolio and make sure the portion of stocks to bonds is at a level you’re comfortable with, and you’re comfortable with the level of risk you’re taking.

Although you might have basic investment knowledge or are invested in a target date fund, we recommend reaching out for third-party advice .

Utilizing an expert for help with investing and allocating your 401(k) may change the performance of your account from good to great.

In fact, a recent Morningstar report shows that participants who received expert guidance had as much as 40% more income during retirement versus those who received no help at all.⁴

It’s never too late to take control of your financial future! If you’d like more tips on How to Supercharge Your 401(k) Performance Today , check out our no-cost guide.

Sources:

- Morningstar, 2013

- The Global Financial Crisis and the Performance of Target-Date Funds in the United States – October 1, 2011

- David Blanchet, Morningstar Analyst 2014, “The Impact of Expert Guidance on Participant Savings and Investment Behaviors”

- David Blanchet, Morningstar Analyst 2014, “The Impact of Expert Guidance on Participant Savings and Investment Behaviors”