6 Questions Every 401(k) Investor Needs to Ask ASAP

If you’ve taken a new job, chances are you were automatically enrolled into a new 401(k), handed a welcome packet, and then left wondering what to do.

The problem is that 63% of Americans don’t understand how a 401(k) plan works.¹

Here’s the deal: If you’re already contributing money from each paycheck to a new 401(k), you need to know how the plan works.

It’s YOUR money – not your employer’s – and it’s also YOUR retirement – not your employer’s.

It is up to you to understand how your new 401(k) works so you can get the most out of it.

In this article, we’re discussing the 6 critical questions you need to ask about your new 401(k) as soon as possible. Knowing these answers could lead to either saving and earning more than you thought you could or missing opportunities to make better returns in the long run.

#1 How Is My Money Invested?

It’s common for employers to auto-enroll new employees in the employer-sponsored 401(k) plan.

While this means more people have 401(k)s, it also means most people are auto-enrolled using the default investment option.

This new way of enrolling plan participants could cost you in the long run because you may be tossed into a target date fund (TDF) that may not align with your goals or risk tolerance.

In addition, TDFs often underperform in good markets and do a poor job of managing downside risk during tough markets.

If you want to maximize your retirement savings, your money should work for you. And should be invested based on your goals, your risk tolerance, and when you will need access to your funds.

Be sure to ask how your money is invested.

#2 When Can I Change My Investment Options?

If you discover that you are auto-enrolled in a target date fund or a fund that doesn’t fit your needs and goals, you need to know the rules of your 401(k) plan to determine what you can do.

That requires you to contact HR or your plan administrator to find out how to change your investment options.

Don’t wait to find out the answer. You want to be able to make the necessary changes as soon as possible.

Here’s why: If you’re a conservative investor and you’ve been put in a pretty aggressive fund and the market moves against you, you may lose money rather quickly.

If you’re an aggressive investor and you’ve been put mainly in bonds, and then stocks take off, you may miss out on opportunity costs.

#3 What Fees Are Associated with the Default Investment Option?

The U.S. Government Accountability Office found that even though 401(k) retirement plans are required to disclose plan and investment fees, “40% of participants don’t fully understand fee information and 41% don’t know they pay fees.”²

If you aren’t careful, high fees can eat away at your retirement savings.

The first thing you need to know is that 401(k) fees fall into 3 basic categories: Investment fees, plan administration fees, and individual service fees.

- Investment Fees make up the largest portion of 401(k) fees and include the cost of investment management and other investment-related services. They are generally charged as a percentage of assets.

- Plan administration fees cover general management, such as record-keeping, accounting, legal, and trustee services.

- Service fees are like additional administrative fees. They cover features that you opt into, like taking out a 401(k) loan, rolling 401(k) investments over to an IRA, or seeking financial advisory services.

As you can see, fees can add up fast.

Unfortunately, you can’t just make these fees disappear, but you do have some options.

You won’t get rid of administrative fees. If they are in your plan, they are there, and there’s nothing you can do about them.

But each of the investment options inside your plan have different fees, and you can switch investment options as the plan allows.

For example, an S&P 500 index fund may have a fee around .02% compared to a target date fund at .7%, which is a significant difference.

Fees are laid out in your statements. This is why you must get your statements, read them, and know this information.

[Related: How to Read a 401(k) Statement and Understand It]

#4 Is There a Roth 401(k) Option?

The Roth allows for tax-free withdrawals in retirement since your contributions are made with after-tax dollars today.

Thanks to the Secure Act 2.0, there are more benefits to the Roth provision.

Starting in 2024, employee plan sponsors can create emergency savings accounts for participants to contribute to a separate emergency savings account that’s part of the 401(k) plan.

Contributions are after-tax only, which means they must be put in a Roth 401(k).

The caveat is that the savings account balance cannot exceed $2,500, and you can take up to one withdrawal per month.

Also, the first 4 withdrawals in a year must be penalty-free.

Your employer can impose fees after that, but you’ll still have access to your money.

Contributions to this new emergency savings account qualify for matching contributions to your 401(k).

Also, if you leave the company, the funds can be converted into a Roth investment account or withdrawn because your contributions are always yours to keep.

[Related Read: Should I Consider the Roth 401(k)?]

#5 Does My Employer Provide Matching Contributions?

The 401(k) company match is basically free money for your future, which is why you want to know ASAP if your employer matches contributions and what the rules are.

For example, a company may match 100% up to 6% of your pay.

If you make $40,000 a year, you could put in $2,400 (or 6%) for the year, and your company would match this 100%.

This means you would get $2,400 of free money toward your retirement.

However, how much you receive depends on the terms of your 401(k) plan.

Many employers match a percentage of employee contributions up to a certain portion of the total salary.

Some match employee contributions up to a certain dollar amount.

Some plans make you wait (because of the high turnover ratio). For example, you may have to wait 3 months to a year to qualify.

At the same time, there are plenty that allow you to participate with your first paycheck.

It’s up to you to find out your plan rules regarding the employer match.

If you don’t know, call HR or your plan representative.

Then, do what you can to contribute at least enough to your new 401(k) to reach the match amount.

#6 What Is the Vesting Schedule?

It is critical for 401(k) investors to know their vesting schedule.

Essentially, vesting schedules prevent 401(k) investors who don’t stay long at a company from taking their employer-matching retirement contributions with them when they change jobs.

The free money you received through your company match may not be yours to keep and can be taken back if you leave before you’re fully vested.

For example, if you were to change jobs after 2 years and your company required you to work for 3 years to vest the entire company match, you would have to forfeit the money your company contributed.

[Related Read: Don’t Lose Your Match: The Danger of Ignoring Your 401(k) Vesting Schedule]

401(k) vesting rules vary from employer to employer.

There are three types of vesting schedules: immediate, graded, and cliff.

- An immediate vesting schedule means you own your employer’s matching contribution as soon as you receive it in your 401(k) account.

- A graded vesting schedule means you vest a certain percentage of your employer’s matching dollars in a set period of time until you are 100% vested. For example, 20% might be vested after your first year working, 40% vested the second year, etc.

By law, employers must vest employees at least 20% at the end of 2 years, and another 20% annually each year thereafter. This means by the end of year 6 of working for your company you will be 100% vested for the company match.

Cliff vesting occurs when a company requires employees to stay employed for a specific amount of time before the money their employer contributed becomes theirs. Employers have up to 3 years to vest employees in this type of vesting schedule.

Want to Maximize Your 401(k)? Here’s How.

401(k) Maneuver exists to help employees grow and protect their 401(k) accounts. We provide independent, personalized professional account management to help employees, just like you, grow and protect their 401(k) accounts.

And we do this without in-person meetings so you don’t have to drive to an appointment or spend hours preparing for the meeting.

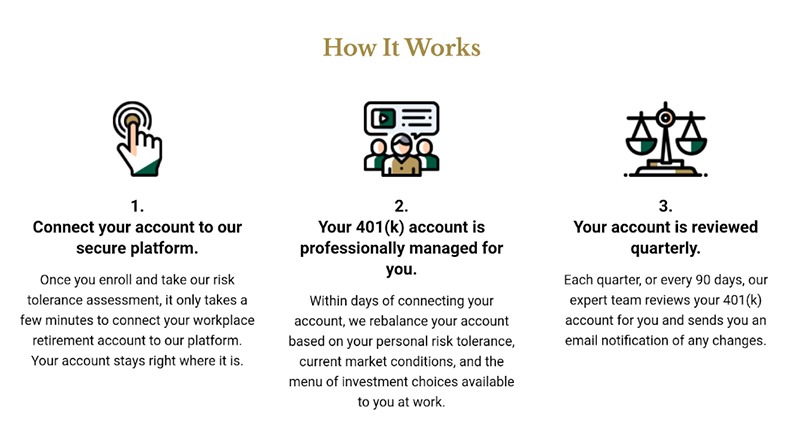

Our done-for-you, virtual service allows you to keep your 401(k) right where it is while we review and rebalance your account based on your risk tolerance and current market conditions.

All you need to do is to connect your account to our secure platform, and we manage your account for you. There’s no need to move your account – you can keep it right where it is.

As a fiduciary, we are bound by law to put your interests first, and we do not receive commissions on the trade.

Watch this short video on how it works and how 401(k) Maneuver may help you increase your account performance.

Have questions about your 401(k) performance? Book a complimentary 15-minute 401(k) Strategy Session with one of our advisors.

Sources

- https://www.cnbc.com/2019/03/07/63-percent-of-americans-are-confused-about-401k-retirement-plans.html

- https://www.gao.gov/products/gao-21-357