7 Things That May Maximize 401(k) Performance in 2022

Looking for a way to get ahead on 401(k) retirement savings this year? Check out the list below of 7 things you can do today to help maximize 401(k) performance in 2022.

#1 Don’t Stay with the Default Plan

More and more employers are automatically enrolling employees in their 401(k) plans.

In fact, more and more companies’ 401(k) plans use target date funds (i.e., 2020, 2030, 2040 funds) as their default option, or Qualified Default Investment Alternative (QDIA).

And, yes, this is totally legal.

The Pension Protection Act of 2016 allowed employers to direct plan participants’ assets into a target date fund and not be liable — should the employee not select an investment.

Marketwatch states, “About 70% of U.S. companies automatically enroll employees into 401(k)-type plans, and more than 86% of these firms now direct people’s money by default into ‘target-date funds’ (TDFs).”¹

According to Vanguard’s How America Saves 2021, roughly 4 in 10 single target date investors choose the funds on their own, not through default.²

That means 6 out of 10 do not select an investment and are automatically enrolled in the default plan.

Here’s why this may be an issue if you’re one of those investors: target date funds are based on the date of retirement.

If you’re younger and plan to retire in 2050, you’re told to select a 2050 fund. If you’re wanting to retire in 2030, you’d select a 2030 target date fund.

Target date funds fail to take into consideration your salary, profession, risk tolerance, goals, and objectives.

Again, you are simply put into a fund based on your expected date of retirement.

In addition, target date funds may not appropriately manage downside risk.

They may underperform in good markets and do a poor job of managing downside risk during tough markets.

According to Morningstar analyst Jeffrey Holt in March 2018…

“In the long run, the biggest risk in target-date funds is that they won’t meet investor expectations for avoiding losses.”³

Those looking to maximize 401(k) performance in 2022 should think long and hard about sticking with the default target date fund.

There are other investment options available to you where you can take into account your risk tolerance and your unique goals and objectives.

[Related Read: Are Target Date Funds Good or Bad?]

#2 Regularly Make Changes to Your Investments

Regularly rebalancing your 401(k) is important because the stock or mutual fund you originally selected (or selected a year ago) may not be right for your risk tolerance now.

However, 80% of 401(k) investors fail to rebalance.⁴

Rebalancing your 401(k) is the process of realigning the weightings of the assets, or investments, in your portfolio. This means you periodically buy or sell assets in your portfolio in order to maintain the initial desired level of asset allocation.

Few people rebalance their 401(k) accounts, and even those who do fail to manage risk through proper asset allocation. Rebalancing only the percentages of current holdings does not consider current market and economic conditions.

This may result in more significant losses during down markets and missed opportunity for growth during good markets.

If you aren’t rebalancing your account allocations, you may be missing out on earning more and keeping more of your hard-earned retirement savings.

Check out the video below to learn more about how rebalancing may help you safeguard your retirement savings.

#3 Reassess Your Risk Tolerance

There’s a common belief of investing that says, if you want safety and security, you have to sacrifice good returns.

This belief can be very costly – especially if you’re close to retirement.

If you want your portfolio to grow, you want to hold both stocks and bonds.

Morningstar reported that, “Since World War II the S&P 500 stock index has returned 11.1 percent, which is 7 percentage points more than the CPI. Even if future returns don’t match those gains, equities are still likely to outperform other assets over the long term.”⁵

According to Morningstar’s Head of Retirement Research, David Blanchett, “A 50-50 stock and bond mix, which gives you growth and income, is a good starting point for retirees.”⁶

Other advice, especially given to older investors, is to build up cash savings so, if the market takes a dip, you have cash on hand and can avoid tapping into your depleted investment portfolio.

The downside to cash is that most money market accounts pay little to no interest.

So, if you’re cash rich, you risk losing value due to inflation.

While it’s important to reallocate your investments per your tolerance to risk, if you are too cautious, you risk coming up short when you retire because you aren’t able to maximize growth.

#4 Try to Max Out the 401(k) Contribution Limit

Employee 401(k) contribution limits for 2022 are $20,500. This applies to 401(k), 403(b), most 457 plans, and the federal Thrift Savings Plan.

For those age 50 and older, the 401(k) catch-up contribution is $6,500.

Not everyone can max out their 401(k) contribution limit each year.

Between cost of living, family obligations, debt, and rising healthcare costs, we get it can be a big stretch.

However, just saving a little bit more than you did last year can help you maximize your 401(k) performance.

See if you can save 2% more than you did last year. If you can swing 5% more, do it.

Let’s say you earn $65,000 a year.

- If you saved 1% more of your salary, you’d save an additional $650 a year, or $54.16 per month.

- If you saved 2% more of your salary, you’d save an additional $1,300 per year, or $108.33 each month.

- If you saved 5% of your salary, you’d save $3,250 more each year, or $270.83 each month.

Imagine what an additional $3,250 each year will bring in returns 10, 20, or 30 years down the road.

Take out a calculator and see what saving an additional 1, 2, or 5% adds up to. Then figure out how to contribute more in 2022.

#5 Contribute at Least the Company Match

An easy way to maximize your 401(k) performance in 2022 is to contribute what your company will match.

If you aren’t currently contributing what your company matches, you’re basically turning away free money.

In some cases, the company match may double the amount of what you’re already saving and may increase your retirement lifestyle.

Let’s say your company matched 100% up to 6% of your pay.

With a $40,000 salary, you could put in 6% or $2,400 for the year, and the company would match this at 100%.

That’s $2,400 per year of free money that will help you grow your retirement savings and help you maximize your 401(k) performance over time.

#6 Get Engaged with Your Investments

Too many people don’t understand what they are invested in. They simply set up a 401(k), fund it, and don’t think much more about it.

If you want to potentially maximize your 401(k) performance, one of the best things you can do is become financially literate.

Get engaged with your investments. After all, it’s your money and your retirement future we’re talking about.

How you do this starts with a decision to take control of your financial future.

Here are a few ways you can enhance your 401(k) savings knowledge:

- Continue reading blogs like this.

- Open your 401(k) statements when they arrive.

- Ask your plan provider questions if you are unclear about your 401(k) investments. Check out this article: 5 Questions to Ask a 401(k) Plan Provider Sooner Rather Than Later.

- Consult a professional.

Learn how to read and understand a 401(k) statement. Watch the video below.

Do whatever you can to gain the knowledge you need to make the best decisions regarding your money.

Once you start to educate yourself, it won’t be difficult for you to understand.

#7 Seek Professional Help

401(k) Maneuver exists to help employees grow and protect their 401(k) accounts. We provide independent, personalized professional account management to help employees, just like you, grow and protect their 401(k) accounts.

And we do this without in-person meetings so you don’t have to drive to an appointment or spend hours preparing for the meeting.

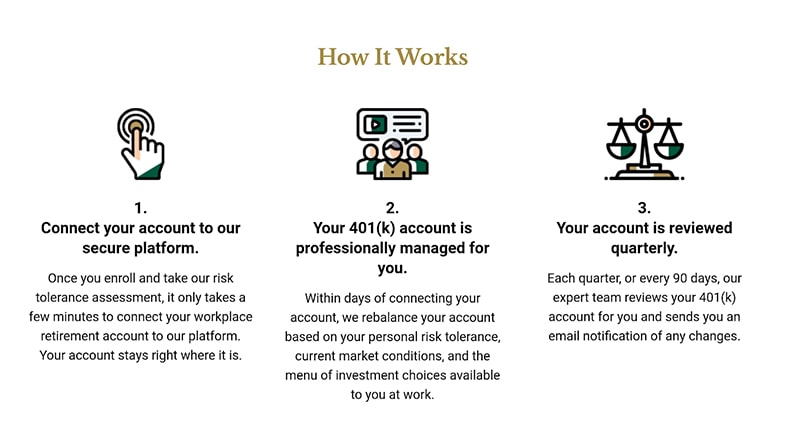

Our done-for-you, virtual service allows you to keep your 401(k) right where it is while we review and rebalance your account based on your risk tolerance and current market conditions.

All you need to do is to connect your account to our secure platform, and we manage your account for you. There’s no need to move your account – you can keep it right where it is.

As a fiduciary, we are bound by law to put your interests first, and we do not receive commissions on the trade.

Watch this short video on how it works and how 401(k) Maneuver may help you increase your account performance.

Have questions about your 401(k) performance? Book a complimentary 15-minute 401(k) Strategy Session with one of our advisors.

Book a 401(k) Strategy Session

- MarketWatch, Opinion: Target-date funds are more expensive and less effective than this simple investment plan, February 20, 2019

- https://institutional.vanguard.com/content/dam/inst/vanguard-has/insights-pdfs/21_CIR_HAS21_HAS_FSreport.pdf

- Special Report: Fidelity puts 6 million savers on risky path to retirement, Reuters.com March 5, 2018

- “Over 90% of Americans make this 401(k) mistake”, Mauri Backman, The Motley Fool

- David Blanchet, Morningstar Analyst 2014, “The Impact of Expert Guidance on Participant Savings and Investment Behaviors”

- David Blanchet, Morningstar Analyst 2014, “The Impact of Expert Guidance on Participant Savings and Investment Behaviors”