9 Simple Ways to Catch Up on Retirement Savings

If you’re in your 40s, 50s, or 60s, and you need to quickly catch up on retirement savings, don’t be discouraged. With planning and a focus on saving and investing, it is possible to make up for lost time.

#1 Figure Out How Much You Need

If you’re behind on retirement savings and don’t have a plan or you had one at one point, but are way off track, it’s time to get planning!

Some people avoid making a plan because they think their account balance isn’t big enough. For others, they think they are too close to retirement to plan at this point.

Whatever the case, if you don’t create a plan NOW, chances are, you aren’t going to have enough money to comfortably retire.

Or worse, you’ll end up with so little saved that you might have to struggle to survive.

From knowing how much you will need to retire to maintain your standard of living when you stop working to knowing exactly what you need to save each month, a plan will help you stay focused as you try and catch up on retirement savings.

If you need help, we suggest speaking to a third-party expert who can help you make the best decisions for retirement saving.

#2 Max Your 401(k) Contribution Limits

There is one way that may ensure you catch up on retirement savings and have enough to live on during retirement…make sure you contribute the maximum amount each year.

Even if you are in your 50s or 60s, it’s not too late to do what you can to save the most allowed, as it will greatly impact the amount you have at retirement.

In 2020, the annual contribution limit was raised to $19,500 for 2020 for employees who participate in 401(k), 403(b), most 457 plans, and the federal government’s Thrift Savings Plan..

For those age 50 and older, the 401(k) catch-up contribution limit will also increase $500–from $6,000 in 2019 to $6,500 in 2020.

This means if you’re 50 or older and need to catch up on retirement savings, you’ll be able to save $26,000 in your 401(k) in 2020.

Let’s assume you’re 51 years old, with $100,000 in retirement savings.

Because you’re over 50, you’re legally allowed to save $26,000 per year in a 401(k) retirement fund.

Now, let’s assume a 7% rate of return, and that you’re able to contribute the maximum to your 401(k) until you retire at the age of 70.

By retirement, you’d have roughly $1.3 million saved. However, this number does not take into consideration inflation.

Even if you can’t max out contribution limits, do whatever you can to try and stash as much away in your 401(k) as possible.

#3 Fund an IRA

Once you’ve maxed out your 401(k) or if you don’t have a 401(k), open an Individual Retirement Account (IRA) and maximize your yearly contribution.

For 2020, the contribution limit is $6,000. If you are over 50, the catch-up contribution limit is an additional $1,000, or $7,000 total.

#4 Put Your Future First

Even if you aren’t playing catch-up on retirement savings, it’s important to put your financial future first.

This means you should put your retirement savings ahead of your kids or grandkids college tuition, loans to family and friends, and even expensive gifts to your children.

Your kids or grandkids have plenty of time to save for retirement. Let them take out the student loan or find another way to raise the money needed.

Also, ensuring your financial retirement security means your children won’t have the burden of taking care of you later on in life.

#5 Don’t Be Too Conservative

If you’re in your 50s or 60s and close to retirement, being too conservative with your investments may be a missed opportunity for you to catch up on retirement savings.

Here’s the truth: market volatility can be your friend. And, if managed properly, it can build wealth.

There are two things that build wealth: time and consistency.

With retirement drawing closer and the need to catch up on your savings a top priority, time is not on your side.

However, if you invest consistently each pay period and if you rebalance your 401(k) each quarter, you’re likely to net more money when the market corrects itself instead of losing money.

Here’s why…

A set it and forget it strategy and being too conservative creates underperformance over time. However, if you are rebalancing quarterly, you may be able to manage risk to minimize losses and capitalize on short-term market opportunities.

#6 Plan On Working Longer

Depending on how much money you must save to catch up on retirement savings, you may need to work longer so you can contribute more to your retirement savings.

Working longer also helps increase the amount of your Social Security check.

Social Security benefits take effect at age 62.

However, delaying retirement each year until 70 can increase your benefits 6% to 8% a year.

There are also downsides to taking Social Security too soon.

If you are 62, and eligible to draw benefits, you will only receive 75% of your benefits because you are under the full retirement age (FRA) of age 66.

Also, if you are still working full-time and make more than $17,640 in income in 2019, Social Security will penalize you for making too much money. One dollar in benefits will be withheld for every $2 in earnings above this limit.

To see what you might receive at different retirement ages, check out this Social Security calculator.

#7 Reevaluate Your Spending Habits

A Bankrate survey conducted in February 2019 shows that 40% of respondents aren’t saving for retirement because they have too many other expenses.¹

The same survey reported that 1 in 5 adults cannot cover their current monthly bills.

Living beyond your means and overspending can significantly set back your retirement savings plan.

And, if you carry the habit of overspending into retirement, it can seriously hurt your retirement lifestyle.

It doesn’t matter how much money you make–whether you’re a $40,000 or $150,000 income household.

Overspending and lack of saving for the future plague all income brackets.

Curbing spending isn’t always as easy as it sounds.

We live in a culture of consumerism, and advertisements bombard us daily. It’s hard not to want to have the newest tech gadget or take a luxury trip like your neighbors just did.

If you’re looking to catch up on retirement savings, we recommend taking it one step at a time to begin to form a new habit of living within your means.

The next time you are at the store or about to check out online, ask yourself if this is something you need or you want.

If it’s a want, don’t buy it right now. Instead, make a plan to save for it.

Also, sit down and review your spending and see what you can cut.

There are numerous online tools that track expenses for you. Some banks also offer this feature.

The benefit of these online tools is that you will be able to quickly evaluate where you’re putting your money.

With this information, you can decide what to cut back and, instead, put that money toward retirement savings.

If you sacrifice by choice today, you won’t have to sacrifice out of necessity later!

#8 Take On a Side Hustle

More and more Americans are taking on side hustles and using the extra income to save more for retirement or to pay down debt.

In fact, 76 percent of people over the age of 55 are using their side hustle income to boost their nest egg.²

Whether it’s tutoring a few hours a week or working weekends in retail, the extra income of a side hustle may make a big difference in your retirement lifestyle.

#9 Seek Independent Third-Party Advice ASAP

If you want to catch up on retirement savings, we recommend seeking third-party advice as soon as possible.

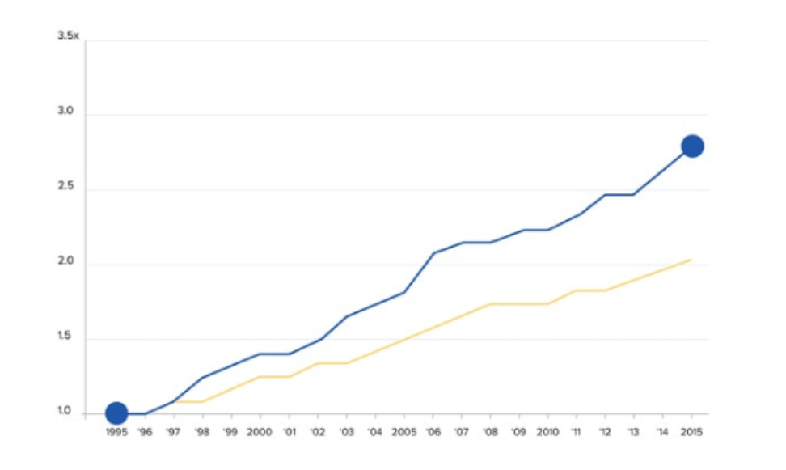

A May 2014 study conducted over a 6-year period compared those who had help with managing their 401(k) and those who did not. The study revealed…

“On average, the median annual returns for participants in the study who got help were more than 3% 4 (332 basis points, net of fees) higher than people who didn’t get help.”³

From the graph above, you can see getting expert help with your 401(k) or retirement savings can be beneficial to life at retirement.

Discover how to secure a solid financial future and potentially keep more of your hard-earned money. Download our no-cost guide 5 Mistakes You Want to Avoid with Your 401(k).

Sources:

- https://www.bankrate.com/banking/savings/financial-security-march-2019/

- https://www.twincities.com/2019/07/27/your-money-how-to-work-gig-work-into-retirement/

- AON Hewitt “Help in Defined Contribution Plans: 2006 through 2012” Published May 2014

- http://www.aon.mediaroom.com/new-releases?item=136959