Are These 401(k) Myths Costing You Money?

401(k) plans are a valuable tax-advantaged retirement savings tool for many Americans.

With it often being the largest retirement asset investors own, it’s critical investors understand how to maximize savings so they earn and keep more to enjoy during retirement.

The problem is many 401(k) myths keep investors from doing just that.

They think they know something to be true, when in fact, it’s not.

Mark Twain famously said…

“It ain’t what you don’t know that gets you into trouble. It’s what you know for sure that just ain’t so.”

Don’t assume what you believe about your 401(k) is accurate. Instead, check out these top 5 401(k) myths below.

#1 Your Employer Pays for All the Costs

Even though your 401(k) is employer-sponsored, it does not mean your employer is managing your 401(k), making changes on your behalf, or assuming all the costs involved.

Your 401(k) comes with various fees that, when added up, may get pricey and have an impact on your 401(k) return over time.

Fees include day-to-day costs to run the plan, such as legal, accounting, and trustee and recordkeeping costs. Some employers will cover the administrative fees for employees and some do not.

There are additional fees that come from the funds themselves, which are also referred to as expense ratios.

The good news is the U.S. Department of Labor requires 401(k) providers to disclose all fees in the prospectus you’re given when you enroll in a 401(k). They also require the information be updated and shared every year to reflect fee changes.

When it comes to investment option fees, some funds have lower expense ratios than others.

We recommend asking your plan provider for the disclosure that shows how much of your return is deducted for the investment’s annual cost. Contact your plan provider or Human Resources and specifically request the 401(k) fee disclosure 408(b)(2) section.

Or, pull out that last 401(k) statement for a breakdown of fees.

Watch the video below to see how to read a 401(k) statement.

#2 You Are Automatically Enrolled in Your Employer’s 401(k) Plan

In 2020, about 62% of businesses automatically enrolled workers into a 401(k) plan, according to the Plan Sponsor Council of America.¹

While many employers automatically enroll their employees, don’t assume your employer does this.

Don’t wait for someone from Human Resources to come to you about it. Take the initiative and contact HR to verify you’re enrolled.

Even if you are automatically enrolled, contributions may not be anywhere near the level you want to invest each pay period.

It’s up to you to elect your own contribution based on your retirement goals and what you can afford to save.

[Related Read: 5 Questions to Ask a 401(k) Plan Provider Sooner Rather Than Later]

#3 Target Date Funds Are the Best Way to Invest

Buying into this 401(k) myth may be the difference between a comfortable retirement and one where you struggle to make ends meet.

Target date funds (such as 2030, 2040, or 2050 funds) are popular because you select a fund based on the date of retirement, and then let it do its thing.

As you age toward your target retirement date, the funds shift toward more conservative investments to reduce risk. Basically, target date funds help make 401(k) investing hands-off.

Another reason target date funds are on the rise is because many plans have target date funds as the default savings option.

When you first contribute to your 401(k), your money often goes into this type of plan ‒ unless you change it, you’ll continue investing in funds that may or may not be right for you.

While target date funds may be popular, this doesn’t mean they are a right fit for every investor.

You may be better off selecting your own investments based on your retirement goals and your risk tolerance, and then rebalancing as needed.

Watch the video below to see how target date funds may hurt your 401(k) account performance.

#4 401(k) Loans Are an Easy, Inexpensive Way to Cover Emergency Needs

What may sound like a good idea at first – being your own bank and borrowing from your 401(k) to cover emergencies or large purchases such as a down payment on a house – may cost you in retirement.

Because every dollar you put out now means you’re losing out on the growth of that money over time.

To show you how powerful compounded growth is to your future, let’s say you are 53, and you plan on retiring at 68 – or in 15 years.

You have $75,000 in your 401(k), and you don’t tap into your account.

Even if you stopped contributing any more money to your 401(k) for the next 15 years, and you got a 6% return on your money, that money could grow to $179,741.

In this hypothetical situation, that’s almost $100,000 growth to your account balance without you ever contributing another cent.

Another reason it’s not advisable to borrow against your 401(k) is because, if you leave your job or are terminated, you have to pay back the loan faster than you’d planned – or face taxes and penalties.

Under the Tax Cuts and Jobs Act (TCJA) passed in 2017, 401(k) loan borrowers have until the due date of your tax return to pay it back.

This means that, if you lost your job and the distribution of the unpaid loan happened in March of 2021, you’ll have until the next tax return deadline to fully pay back the loan.

If you don’t pay the full unpaid balance by this date, the loan will be treated as an early withdrawal, and the unpaid loan balance will be considered a taxable distribution.

And, if you are under age 59½, you will also have to pay a 10% federal tax penalty on the unpaid balance along with income taxes on the balance of the loan.

So you can see where a “good idea” can turn into a nightmare – costing you more than you’d expected in the short term – and later in retirement.

Wondering if you should borrow from your 401(k) to purchase a house or to help with the down payment? Check out the video below.

#5 A Set-It-and-Forget-It Approach Works Best

This 401(k) myth is one that may be doing more harm than good to your account balance.

Despite what some investors believe, a 401(k) plan is not a set-it-and-forget-it program.

In fact, it’s the opposite.

Saving for retirement is a long game, and it’s important to make adjustments as you go through different phases of your life.

Risk tolerance and goals change as we age. So does tax policy, trade regulations, markets, and the investments you originally selected.

So, why set up a 401(k) plan and leave it alone for decades?

It makes no sense, does it?

If you want to maximize your 401(k), you need to course correct. And that means regularly rebalancing your account.

In down or volatile markets, rebalancing your 401(k) may help you stay within your risk level and protect against potential losses.

And, in good markets, rebalancing may help you take advantage of opportunities for growth.

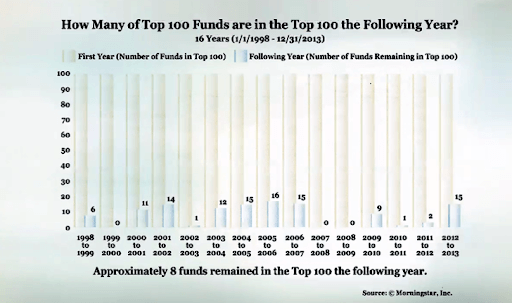

A Morningstar study monitored the top 100 best-performing mutual funds between January 1, 1998, and December 31, 2013.

This study revealed that, in any given year of top best-performing 100 mutual funds in any of those years, in the next year, about half of the time, only 8 out of 100 remained in the top 100 the very next year.²

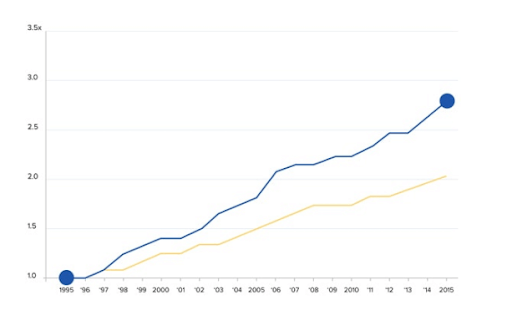

“Participants who got Help received, on average, 3.32% (net of fees) more in return annually” than those who managed their own portfolios.

Check out our 401(k) calculator here to see how you may improve your account performance.

If you are unsure how to properly rebalance your account or don’t know where to start, we’re here to help.

401(k) Maneuver provides independent, professional account management to help employees, just like you, grow and protect their 401(k) accounts.

Our goal is to increase your account performance over time, manage downside risk to minimize losses, and reduce fees that are hurting your retirement account performance.

With 401(k) Maneuver, you can go about your life doing what you love with confidence, knowing we are handling the changes for you.

Have questions or concerns about your 401(k) performance? Book a complimentary 15-minute 401(k) strategy session with one of our advisors.

Book a 401(k) Strategy Session

Sources:

- https://www.cnbc.com/2021/12/28/more-employers-use-401k-automatic-enrollment.html

- The Impact of Expert Guidance on Participant Savings and Investment Behaviors. David Blanchett, Morningstar Investment Management Group, 2014.

- https://www.investopedia.com/articles/personal-finance/102616/how-much-can-advisor-help-your-returns-how-about-3-worth.asp

- https://www.edelmanfinancialengines.com/press/2014/financial-engines-aon-hewitt-find-401k-participants-who-use-professional-help-are-better-off