Behind on Retirement Savings after 60: Avoid these 8 Mistakes

In your 60s, retirement is drawing closer or is months away. If you’re behind on retirement savings after 60, check out our 8 mistakes to avoid and tips on what to do instead.

#1 Thinking Nothing You Do Now Will Make a Difference

If you’re in your 60s and are behind on retirement, you might think nothing you do at this point will help.

Nothing could be further from the truth.

While you might not be able to catch up to your retirement goals, you might be able to get closer than you think.

Anything you can do now to save, eliminate debt, and plan for retirement will help.

If you’ve become apathetic about retirement, we encourage you to shift your mindset and learn as much as you can about how to have the most comfortable retirement possible.

As you’ll see in the tips below, with a few changes in spending and saving, and a clear focus on where you need to be and by when, you can make a difference in your retirement.

#2 Not Taking Advantage of 401(k) and IRA Catch-Up Contribution Limits

The annual contribution limit has been raised to $19,000 for 2019 for employees under 50 who participate in 401(k), 403(b), most 457 plans, and the federal government’s Thrift Savings Plan. This is $500 over 2018.

For employees age 50 or older in the plans listed above, the additional contribution limit will stay the same for 2019 at $6,000.

This means the annual contribution limit is $25,000 for those 50 or older.

For traditional and Roth IRAs, contribution limits are $6,000 in 2019, $500 over 2018.

The catch-up limit is fixed at $1,000 for those over 50–so if you’re in your 60s, the annual contribution limit is $7,000.

How much you can realistically contribute to your 401(k) depends on how much you earn and the amount of debt you carry, among other factors.

Even if it’s a stretch, do what you can to save as close to the 401(k) and/or IRA contribution limits as possible.

Make cuts in monthly spending.

Consider rescheduling that European vacation or other large purchases.

Get a second job and use the money from your side hustle to max out your contribution limits.

Do what you can NOW to meet that limit.

Remember, depending on what your company matches for your 401k) or workplace retirement account, it may double the amount of what you’re already saving.

#3 Being Too Cautious as an Investor

There’s a common belief of investing that says that if you want safety and security, you have to sacrifice good returns.

This belief can be very costly–especially if you’re close to retirement.

If you want your portfolio to grow, you want to hold both stocks and bonds.

Morningstar reported that, “Since World War II the S&P 500 stock index has returned 11.1 percent, which is 7 percentage points more than the CPI. Even if future returns don’t match those gains, equities are still likely to outperform other assets over the long term.”¹

According to Morningstar’s Head of Retirement Research, David Blanchett, “A 50-50 stock and bond mix, which gives you growth and income, is a good starting point for retirees.”²

Other advice often given to older investors is to build up cash savings so if the market takes a dip, they have cash on hand and can avoid tapping into their depleted investment portfolio.

The downside to cash is that most money market accounts pay little to no interest.

So, if you’re cash rich, you risk losing value due to inflation.

While it’s important to reallocate your investments per your tolerance to risk in your 60s, if you’re too cautious, you risk coming up short when you retire because you aren’t able to maximize growth.

#4 Overspending

As you near retirement, it might be tempting to splurge a little. If you’ve been saving for a while, it’s easy to want to take off the brakes and reward yourself.

Luxury trips. New boat or car. Finally adding a sunroom onto the house.

These rewards can quickly derail you from your retirement dreams and goals.

If you’re behind on retirement savings, avoid big “reward” purchases and do whatever you can to stay focused and on track.

#5 Paying Off Debt Not a Priority

If you’re behind on retirement savings after 60 and you still have outstanding debt, you need to take action now to get debt paid off before you retire.

Credit card, student loan, and even house debt can drain your retirement savings fast.

We recommend you review your budget and see what expenses you can cut.

Depending on how much debt you have, you might need to take a second job or sell things to pay it off.

Also, do whatever it takes to not incur any new debt between now and retirement.

If you’re really behind on saving for retirement and in a ton of debt, consider selling your home and downsizing.

Use the profit to pay off debt and fund your retirement savings.

#6 Taking Social Security Too Soon

While Social Security benefits kick in at 62, it’s advisable not to do so as it can be a costly mistake.

Let’s say you are 62, and are now eligible to draw your benefits.

Think about this before you take that first check:

- Since you are under FRA (full retirement age), you will only receive 75% of your benefits at this age.

- If you are still working full-time and make more than $17,640 in income in 2019, Social Security will penalize you for making too much money. One dollar in benefits will be withheld for every $2 in earnings above this limit.

- If you quit working, you are not eligible for Medicare until age 65. Unless you are on your spouse’s healthcare plan, your cost of healthcare may take the majority of your Social Security benefits. Check pricing on www.healthcare.gov.

According to 401(k) Manuever’s™ Brian Neff,

#7 Not Saving Enough for Healthcare

Healthcare is expected to be one of the largest retirement expenses–with an estimated $285,000 (after tax) in medical expenses needed in retirement for the average couple over 65 in 2019, according to Fidelity Retiree Health Care Cost Estimate.⁴

Factors contributing to soaring costs include…

- People are living longer.

- Healthcare inflation.

- Average retirement is 62, while Medicare eligibility is 65.

With the day of union- and company-sponsored health benefits to retirees gone, the burden now falls on you to plan and save.

The exact amount you’ll need depends on…

- How healthy you are.

- When and where you retire.

- How long you live.

- Your tax rates in retirement.

- How you pay for medical expenses.

If you’re still working and your employer offers an HSA-eligible plan, we recommend enrolling and contributing to an HSA, which will help you save for healthcare costs during retirement.

#8 Not Getting Expert Advice

If you’re behind on retirement savings after 60, it’s critical you get expert advice on how to protect and grow what you have this close to retirement.

Especially if you’re in your 60s, you need to speak with an expert who can help you reallocate your investments per your tolerance to risk and time to retirement…

And advise on Social Security and healthcare savings.

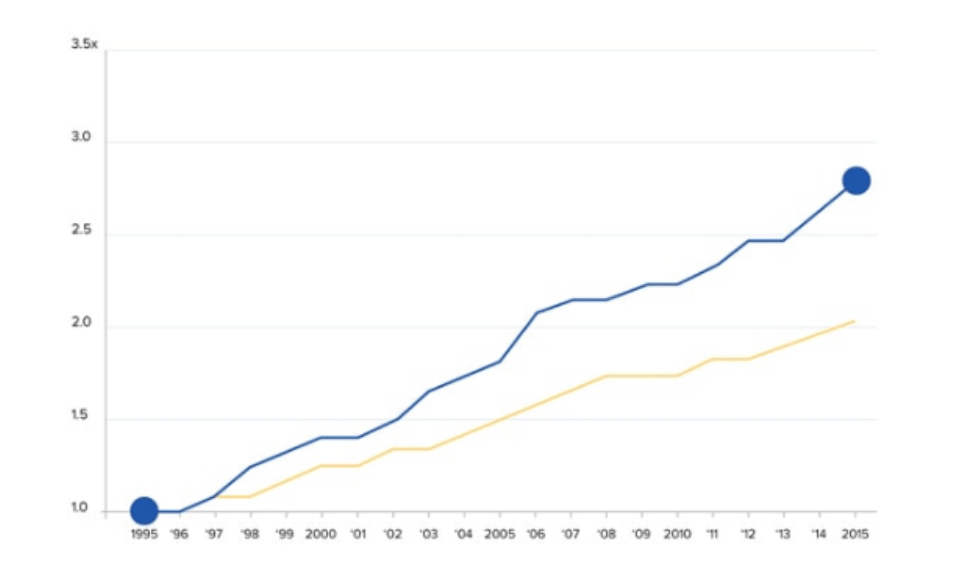

A 2014 study conducted over a 6-year period compared those who had help with managing their 401(k)s and those who did not.

The report showed that “on average, the median annual returns for participants in the study who got help were more than 3% 7 (332 basis points, net of fees) higher than people who didn’t get help.”⁵

Add that up over the years, and 3% 7 higher annual returns just by getting expert help can add up to tens of thousands of dollars you could potentially save.

Wouldn’t you say that’s worth reaching out for help?

In another 2014 Morningstar report, David Blanchett, CFA, CFP, and Head of Retirement Research, stated that participants who received expert guidance had as much as 40% more income during retirement versus those who received no help at all.⁶

We encourage you to sit down and write out the impact an extra $20,000, $50,000, or $100,000 of retirement income would have on your life.

If you’d like more retirement savings tips, download our no-cost guide How to Supercharge Your 401(k) Performance Today.

Sources:

- https://www.consumerreports.org/retirement-planning/how-to-protect-your-retirement-savings-from-inflation/

- https://www.consumerreports.org/retirement-planning/how-to-protect-your-retirement-savings-from-inflation/

- Brian Neff, 401(k) Maneuver™

- https://www.fidelity.com/viewpoints/personal-finance/plan-for-rising-health-care-costs

- David Blanchet, Morningstar Analyst 2014, “The Impact of Expert Guidance on Participant Savings and Investment Behaviors”

- David Blanchet, Morningstar Analyst 2014, “The Impact of Expert Guidance on Participant Savings and Investment Behaviors”

- http://www.aon.mediaroom.com/new-releases?item=136959