Can I Really Catch Up on Retirement If I’m over 50?

For investors behind on retirement and over 50, it may seem as if there is little they can do to catch up.

The good news is that you may be able to get closer to your retirement goals than you think. Below are 9 ways you can catch up on retirement over 50.

#1 Revisit Your Retirement Plan

When was the last time you looked at your retirement plan? Do you even have one in place?

This is where you want to start. Because if you don’t know where you are and where you want to be in retirement, chances are you’ll never get there.

If you want to catch up on retirement over 50, you need a solid plan in place ASAP, and you need to work the plan. And, you’ll need to analyze your progress along the way.

Take time to answer a few questions:

- At what age do you want to retire?

- How much money will you need, not to just scrape by, but have a fulfilling, comfortable retirement?

- How much do you currently have saved for retirement?

Don’t be discouraged if you aren’t where you want to be.

Remember, the key is to figure out where you are and where you want to be. With that information, you can create a plan.

If you get stuck, we recommend seeking professional help as soon as possible.

#2 Delay Retirement a Few Years

After reviewing your retirement plan, you may discover you need to extend your working years and delay retirement.

While you may not like the idea, doing so may make a big difference having money to just get by and having enough during retirement.

Let’s say you are 50, have no savings at all, and want to retire at 65.

If you contribute, starting this year, $500 per month and earn 7% annual rate of return, you’ll have a total of $158,481 saved after 15 years.

If you delay retirement by 5 years, and continue contributing $500 per month earning a 7% return, you’ll have saved a total of $260,463.

#3 Stop Lending Money to Family

If you are behind on retirement over 50 and you continue to lend or give money to family members (or take on student loan debt so your grandkids can go to college), you aren’t going to have enough money in retirement.

Also, if you don’t have enough money in retirement, your kids and grandkids will likely have to help you out financially in your later years.

We don’t know many people who want to be a financial burden to their family, do you?

So when it comes time to paying the maximum each year into your retirement or helping out your grandkids, think first.

#4 Watch Your Spending

If you’re over 50, chances are you’re at a point in your life where you want to splurge a little — after all, you deserve it for all the hard years of work, right?

Of course you deserve it.

But is it wise right now to buy that new car or add that addition onto the house? If you do so, will you be eating into your retirement income in the future?

If you’re behind on retirement savings and over 50, avoid big “reward” purchases and do whatever you can to stay focused and on track with your savings goals.

#5 Open an IRA

In addition to contributing to your 401(k), open and fund an Individual Retirement Account (IRA) to diversify your investment portfolio while reducing your taxable income.

Currently the contribution limits for pretax and Roth IRAs for 2021 is $6,000. The catch-up contribution for people age 50 and over remains the same additional $1,000.

Remember, you have until April 15, 2021, to contribute the maximum for 2020.

#6 Take Advantage of 401(k) and IRA Catch-Up Contribution Limits

The annual 401(k) contribution limit for 2021 is $19,500. This applies to 401(k), 403(b), most 457 plans, and the federal Thrift Savings Plan.

For those age 50 and older, the 401(k) catch-up contribution is $6,500.

If you’re 50 or older and need to catch up on your 401(k) retirement savings, the total amount you’re able to save is $26,000. If you turn 50 anytime during December of 2021, you’re still eligible to contribute the additional $6,500.

For traditional and Roth IRAs, contribution limits are $6,000 in 2020. The catch-up limit is fixed at $1,000 for those over 50 — so if you’re behind on retirement over 50, the total amount you can contribute is $7,000.

How much you can realistically contribute to your 401(k) depends on how much you earn and the amount of debt you carry, among other factors.

Even if it’s a stretch, do what you can to save as close to the 401(k) and/or IRA contribution limits as possible.

Make cuts in monthly spending.

Consider rescheduling that European vacation or other large purchases.

Get a second job and use the money from your side hustle to max out your contribution limits.

Do what you can NOW to meet that limit.

Remember, depending on what your company matches for your 401k) or workplace retirement account, it may double the amount of what you’re already saving.

#7 Downsize Your Home and Invest the Difference

There are many pros to downsizing over 50. Not only can it help reduce expenses and stress, but you can also use it to invest a large chunk of cash in your retirement savings.

#8 Reconsider Target Date Funds

Perhaps when you signed up for your 401(k) plan, you were automatically enrolled into a target date fund (such as a 2030 or 2040 fund).

If so, you may want to reconsider this option.

Target date funds are structured to automatically reallocate as you move through different life stages.

As you age toward your target retirement date, the funds shift toward more conservative investments to protect your money.

If you’re wanting to retire in 2030, you would be told to select a 2030 target date fund.

What this means is investors are grouped solely based on their expected retirement date–location, age, profession, salary, risk tolerance, goals, and objectives are not taken into consideration.

Basically, investing in target date funds and not actively managing your retirement account is equivalent to saying there’s a one-size-fits-all investment strategy that works for everyone.

This doesn’t pass the common sense test, does it?

Another reason we recommend investors avoid target date funds is because they are riskier than many people perceive.

. Citing studies by institutional advisory firm Research Affiliates, Barron’s associate editor Randall W. Forsyth wrote in a February 2019 article, “They [the studies] show that the standard ‘glide path’ of target-date funds, which start heavily weighted in stocks and reallocate to bonds in later years, doesn’t produce the desired results.”¹

According to Rob Arnott, chairman of the board of Research Affiliates:

An article titled Global Financial Crisis and the Performance of Target-Date Funds indicated that on average, target date funds (like 2030 or 2040 funds) invested 75% in stocks, generating average losses of over 30% during the 2008 financial crisis. Investors planning to retire in 2010 suffered significant losses because 2010 target date funds increased their common equity exposure in 2007.³

Morningstar analyst Jeff Holt recently commented, “In the long run, the biggest risk in target-date funds is that they won’t meet investor expectations for avoiding losses.”⁴

By quarterly rebalancing your retirement account, you’ll lower the risk of your account underperforming due to target date funds that may not manage downside risk.

However, if you can, we recommend moving away from this option and better utilize all the options available in your workplace retirement plan.

At the very least, quarterly rebalance your account.

Download our guide 5 Ways Target Date Funds Fail to Live Up to Their Promise.

#9 Seek Professional Managed Help

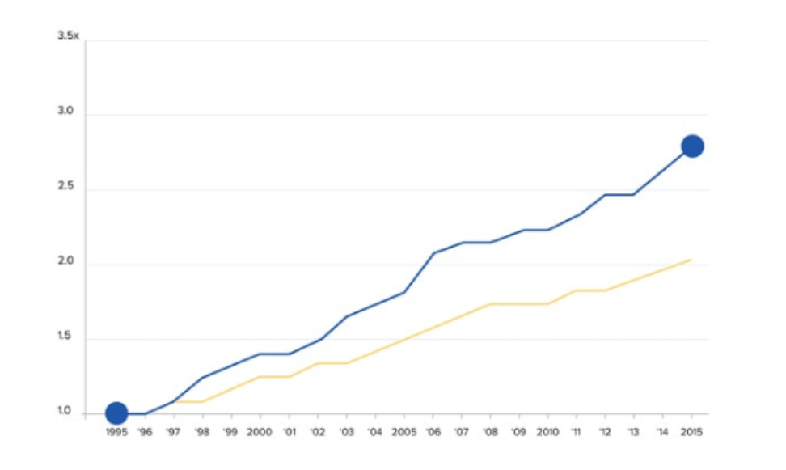

A May 2014 study conducted over a 6-year period compared those who had Help with managing their 401(k)s and those who did not. The study revealed…

“On average, the median annual returns for participants in the study who got Help were more than 3% (332 basis points, net of fees) higher than people who didn’t get Help.”⁵

From the graph above, you can see getting professional help with your 401(k) or other workplace retirement account can be beneficial to life at retirement.

Think of it this way…if you had heart issues, you wouldn’t make major health decisions without the advice of a cardiologist.

So, why turn what could be your largest financial asset over to chance?

If you’d like to take control of your financial future and have more income at retirement, we strongly suggest getting third-party advice.

If you’re hesitant to reach out for advice because you think your account balance isn’t big enough, or you think you’re too close to retirement to get help, don’t let that stop you!

401(k) Maneuver provides professional account management with the goal to help you grow and protect your 401(k).

Our goal is to increase your account performance over time, manage downside risk to minimize losses, and reduce fees that harm your account performance.

There are no time-consuming in-person meetings and nothing new to learn, and you don’t have to move your account.

Simply connect your account to our secure platform, and we regularly review and rebalance your account for you, when necessary. Check out more about how it works.

If you have questions about your 401(k) or if you need help, we’re here for you. Click below to book a complimentary 15-minute 401(k) Strategy Session.

Schedule a 401(k) Strategy Session

Sources:

- MarketWatch, Opinion: Target-date funds are more expensive and less effective than this simple investment plan, February 20, 2019

- MarketWatch, Opinion: Target-date funds are more expensive and less effective than this simple investment plan, February 20, 2019

- The Global Financial Crisis and the Performance of Target-Date Funds in the United States – October 1, 2011

- Special Report: Fidelity puts 6 million savers on risky path to retirement, Reuters.com March 5, 2018

- AON Hewitt “Help in Defined Contribution Plans: 2006 through 2012” Published May 2014