Family Financial Planning: Why Awkward Money Talks Are Necessary

What parent conversation is more uncomfortable than the birds and bees? Talking to your adult children about family financial planning.

According to a study by Home Instead Senior Care, approximately 80 million Americans neglect to have important end-of-life discussions regarding family financial planning.¹

The study also reports, “Unfortunately, research indicates that 70 percent of conversations happen too late, being initiated by an event such as a health crisis or other emergency, which may increase the likelihood of family disputes. According to surveyed attorneys, two-thirds of these disputes that end up in court could have been avoided if end-of-life wishes were communicated and documented in advance.”²

As much as we’d like to control our destiny, we never know when our time will come.

But there is something we can control – our finances.

However, even if you are meticulous with your money, you may still leave your kids in a difficult position if you haven’t practiced family financial planning.

Family Financial Planning Defined

This is an all-encompassing term for planning your financial future and including your family, such as keeping your adult kids in the loop.

These conversations include talking to your adult kids about how much money you have, what your financial outlook is for the rest of your life, and what is to be expected upon your death.

And, if you are like most American parents, that makes you squirm.

It’s hard to talk about your finances with your kids, even after they become adults.

There are many reasons.

First, we’ve been conditioned to think it is inappropriate.

Second, we don’t want to burden our children.

Third, we don’t like to consider a future where our kids exist, and we don’t.

But your adult children need to know where things stand with you financially so that they can better prepare.

Consider the following statistics from a Fidelity Investments study.³

- 92% of parents expect their children will assume the role of executor; however, 27% of children identified as executor didn’t know this was expected of them.

- 69% of parents expect one of their children will help manage their investments in retirement; however, 36% of kids identified in this role didn’t know this was expected.

- 72% of parents expect one of their children will assume long-term caregiver responsibilities in retirement if needed; however, 40% of children identified as the caregiver didn’t know it was them.

In general, family financial planning requires you to talk to your kids about these things to avoid any surprises in the future.

As awkward as the whole family financial planning talk may be, it is one of the most important conversations you may ever have.

Why Family Financial Planning Is So Important

Most of us know someone who has been shocked to learn about their parent’s finances upon a severe illness or death.

We also have all heard stories about families broken apart after the reading of the will.

The reason these scenarios are familiar is because they happen often – and they shouldn’t.

By including your adult children in financial conversations today, you may help prevent shock and hurt later.

Even if you make financial decisions your children don’t agree with, it is still better for them to know ahead of time.

Given that family financial conversations are uncomfortable, we’ve compiled a list of topics that should be covered and tips for handling the talk with grace.

#1 Follow the 40/70 Rule

According to the study by Home Instead Senior Care, “Given the severe consequences of waiting too long to have this critical conversation, if your parents are approaching 70 and you are approaching 40, you should have ‘the talk’ about critical aging issues.”⁴

Finances and living preferences are two of the important critical aging issues that parents and adult children need to discuss.

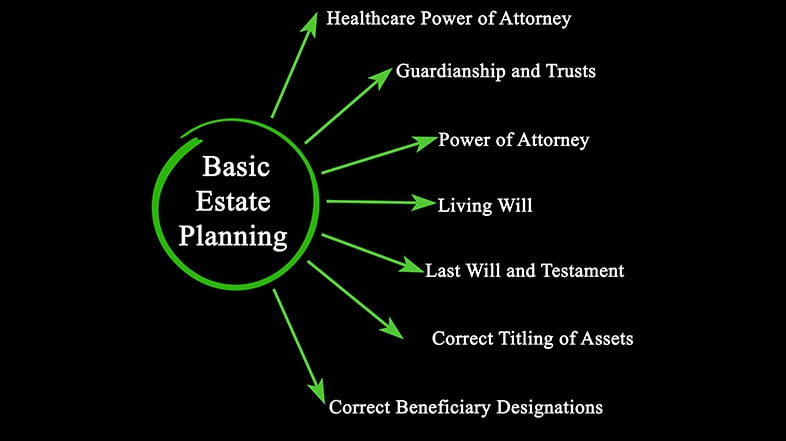

#2 Use Estate Planning Tools

Estate planning details where your assets go after you die. The process protects family members from headaches, heartbreaks, and confusion.

Estate planning includes wills, trusts, powers of attorney, and life insurance.

You need a will. Even if you think you don’t have “enough” to have a will, you need a will.

If you don’t have a will, the courts decide what happens to your assets. And chances are they won’t go where you want them to.

Ideally, you should work with an attorney to do this type of family financial planning.

#3 Tell Your Adult Children Where to Find Everything

Get your documents in order.

Whether you put together a notebook with all your financial information or create a computer document, you should have everything together in one place.

And you need to tell your kids where to find it.

Those handling your estate need the following information (and know where you’ve stashed the info):

- Bank and investment accounts

- A list of assets

- Debts

- Insurance information

- Your pension or other income

- Recurring expenses

- Names and contact information for the following: accountant, financial planner, lawyer

- Powers of attorney

- Your estate’s executor

- Any healthcare proxies

- Living wills

- Wills

#4 Share What You May or May Not Need

One of the more awkward parts of family financial planning is discussing what you may or may not need from your children.

For example, if you are financially prepared to take care of yourself or have long-term care insurance, let your children know.

Likewise, if you believe you may need financial assistance from your children, prepare them for the possibility.

Have honest conversations about extended care and where you want to live out your days.

Along these same lines, this is also the time when you discuss funeral expenses.

For instance, do you plan for your children to use your life insurance policy for the funeral? Let them know now.

#5 Discuss Their Potential Inheritance

Here’s a startling statistic: 68% of young people expect an inheritance, yet only 40% of their parents will leave one.⁵

If your children have the wrong notion about an inheritance, you need to set the record straight.

If you plan to give your children an inheritance, discuss it without being so specific that they become dependent on money they haven’t yet received.

#6 Be Honest about Debts

The good news is your kids should not be held accountable for your debts after you pass away.

However, your estate will have to pay off any debts.

This means whatever money the executor of your estate (possibly one of your children) makes from selling your home, cars, or other possessions goes toward paying off the debt.

Rather than having your children surprised that they have to sell the family home, discuss the reality of your debt situation with them ahead of time.

Take family financial planning a step further and start working toward getting out of debt altogether.

#7 Identify Family Roles

Whether you receive a serious diagnosis or pass away, your children may likely be tasked with handling your finances at some point.

Therefore, it is critical to identify which roles your children may play.

You need to designate one of your adult children as the one handling finances (aka the executor of your estate).

Additionally, identify the one who takes on the role of caregiver and who holds power of attorney.

If you don’t feel your children are up to these types of tasks, designate a third party.

While uncomfortable, this type of family financial planning should alleviate stress in the long run.

#8 Talk about Your Wishes

Along with important discussions regarding end-of-life care, such as living wills and power of attorney, you need to talk about financial considerations.

Talk to your family about your funeral requests and if there is money set aside to cover the costs.

Tell your children how you plan to divide your assets – especially if they are not divided equally.

As sad as this conversation is, it helps prevent family discord.

While you’re alive, you have time to explain your financial decisions and mend hurt feelings rather than having your children turn into enemies after a lawyer reads a will.

General How-Tos for Having the Family Financial Planning Talk

In addition to the above topics to cover, here are some tips to make the talk go smoothly.

- The Sooner, The Better: Have the conversation earlier rather than later. This gives your family time to accept your plans.

- Set a Time and Place: Don’t surprise them with a death folder at Thanksgiving dinner. Prepare them ahead of time for the conversation.

- Make It an Ongoing Conversation: After the initial conversation, continue talking about your financial situation.

- Avoid Specific Numbers: Stick to general numbers instead of telling your exact amounts since account balances ebb and flow.

We regularly post videos with financial information and updates. Check us out on YouTube.

Sources:

- https://www.prnewswire.com/news-releases/study-finds-most-families-wait-too-long-to-begin-aging-conversations-270894401.html

- https://www.prnewswire.com/news-releases/study-finds-most-families-wait-too-long-to-begin-aging-conversations-270894401.html

- https://www.fidelity.com/bin-public/060_www_fidelity_com/documents/fidelity/Family-Finance-Infographic.pdf

- https://www.prnewswire.com/news-releases/study-finds-most-families-wait-too-long-to-begin-aging-conversations-270894401.html

- https://www.cnbc.com/2017/06/06/68-percent-of-millennials-expect-an-inheritance-only-40-percent-of-them-will-get.html