How to Maximize 401(k) Retirement Savings at Any Age

The question of how to maximize 401(k) retirement savings is one we get asked frequently.

Whether you’re in your late 20s or early 60s, it’s an important question to ask because if you aren’t thinking about your financial future, no one else will.

According to the Wall Street Journal, more Americans are reaching retirement age in worse financial shape than the prior generation, for the first time since Harry Truman was president.¹

With more and more baby boomers entering retirement age, study after study shows a majority have not saved enough.

Rising healthcare costs, people living longer than expected, and undisciplined spending mean many are on a path to run out of money.

The Insured Retirement Institute April 2019 report states that 45% of baby boomers have nothing at all saved for retirement.²

While savings aren’t the only source of income in retirement–there’s social security, pension payments, and income from part-time work–they still are an important component to retiring comfortably and making sure enough money is saved.

The statistics for younger generations isn’t that promising either.

With households carrying too much debt and the rising cost of living and healthcare, not enough people are saving for retirement.

We don’t share this information to depress you.

Rather, to help encourage you to get back on track toward saving for a retirement lifestyle you desire .

No matter where you are toward your retirement goals, there’s no time like the present to take action.

Keep reading for tips on how to maximize 401(k) retirement savings at any age.

Become an Engaged 401(k) Investor

Sadly, popular advice is systematically disconnecting people from their 401(k)s or other workplace retirement accounts.

Our industry tells people that it’s hard to be a successful investor.

As a result, there is little education and training that goes into investing for retirement.

It’s no wonder many people are apathetic about their retirement and savings.

No wonder many people fail to regularly open statements, ask questions about their workplace retirement account, or seek third-party help.

The result is that, rather than managing their 401(k), too many investors are simply hoping they’ll have enough for retirement.

They feel hopeless because they believe they have little control over their 401(k) account’s performance.

We at 401(k) Maneuver believe it isn’t difficult to be a savvy investor, and we’re committed to providing you the info you need to help you manage your 401(k) better.

When you invest in yourself and your knowledge, no one can take it away from you.

With a little time and effort, you can grow your investing skills and have more control over your financial future.

And, when this happens, you’ll be empowered to make the changes needed that may maximize your 401(k) retirement savings at any age. [link to pop up opt in for supercharge guide]

So, how do you go from a passive investor hoping for enough to one who is engaged and proactive?

The first step is to review your 401(k) statement every time you receive it.

Reviewing your statement will help you have a better understanding of the information that is provided to you.

It also helps you determine whether or not you’re on track to meet your financial goals.

If you don’t understand what you’re receiving, reach out to an expert for help.

Doing so may have a big impact on your overall returns and confidence about achieving your goals for retirement.

The second step is to educate yourself.

Read our blog articles for retirement tips and savings strategies, and search online for related articles. Go to local seminars or attend webinars on the topic.

Remember, if you don’t invest in yourself, no one else will.

And if you aren’t doing anything, it’s unlikely you’ll reach your retirement goals. So take action today to learn as much as you can.

How to Maximize 401(k) Retirement Savings in Your 20s

If you’re in your 20s, you have the opportunity to build wealth for retirement because you have time on your side.

If you don’t have a family to feed yet or a mortgage to pay, it’s easier to save.

Here are a few ways you can jumpstart your 401(k) retirement savings…

- If you haven’t signed up for your employer’s 401(k) plan, do so ASAP.

- Contribute as much as you can to your 401(k).

- Whatever you do, at least put in the company match because it’s like getting free money!

- Build an emergency fund so you won’t have to pull back on your 401(k) contributions or go into debt if an emergency arises.

- Avoid target date funds.

- Rebalance your 401(k) account quarterly.

- Get expert advice.

How to Maximize 401(k) Retirement Savings in Your 30s

The 30s bring about major life events such as marriage, kids, a new house, and often a higher-paying salary.

It’s easy to get caught up in the excitement of our daily lives and ignore retirement planning.

In order to avoid stress and worry that come in the 40s and 50s from lack of planning (and working your plan), here are a few ways you can jumpstart your retirement savings after 30…

- Create a solid plan for retirement.

- Try to maximize annual 401(k) contribution limits.

- If you can’t maximize your 401(k) contributions, at least put in the company match.

- Build an emergency fund so if something comes up like your car breaks down, you won’t have to pull back on your 401(k) contributions or go into debt.

- Avoid target date funds.

- Rebalance your 401(k) account quarterly.

- Get expert advice sooner rather than later.

Click here for 5 ways to jumpstart retirement savings after 30.

How to Maximize 401(k) Retirement Savings in Your 40s

Saving for retirement if you’re over 40 brings up a key concern: Will I have enough money to retire based on what I’ve saved thus far?

Most people in their 40s are at their peak earning potential.

Yet, statistics show more and more aren’t able to save the maximum due to other priorities.

A recent survey by T. Rowe Price showed that 69% of parents want to put money toward college first, and more than three quarters say they are willing to delay retirement to pay for kids’ schooling.³

Add to that the $4 trillion in consumer debt Americans now owe ($1 trillion of which is revolving debt such as credit card debt), the rising cost of healthcare, and taking care of aging parents.

It’s no wonder so many 40-somethings lack confidence in their retirement preparedness and are often at a loss about where to start to get back on track.

Here are 5 things you can do right now to take control of your financial future and maximize your 401(k) retirement savings after 40…

- Create a solid plan for retirement.

- Try to maximize annual 401(k) contribution limits.

- If you can’t maximize your 401(k) contributions, at least put in the company match.

- Continue to build your emergency savings–should an emergency arise, you won’t have to cut back on your 401(k) contributions.

- Roll over older workplace retirement accounts.

- Avoid target date funds.

- Quarterly rebalance your 401(k) account.

- Seek third-party expert advice as soon as possible.

Check out more retirement savings tips if you’re in your 40s.

How to Maximize 401(k) Retirement Savings in Your 50s

With retirement getting closer, now is the time to plan on maximizing your 401(k).

However, if you’re behind on your retirement savings and are unsure how to make a difference at this point in your life, it’s easy to want to give up.

The truth is, with planning and determination, it is possible to enjoy a comfortable retirement.

Below are a few things you can do right now to maximize your 401(k) retirement savings after 50…

- Do whatever you can to maximize annual 401(k) contribution limits.

- Consider delaying retirement for a few years so you can save more.

- Roll over older workplace retirement accounts.

- Avoid target date funds.

- Quarterly rebalance your 401(k) account.

- Seek third-party advice sooner rather than later.

Read more on how to catch up on 401(k) retirement savings after 50.

How to Maximize 401(k) Retirement Savings in Your 60s

In your 60s, retirement is a few years or even months away.

As you near retirement, it’s crucial you do what you can to maximize your 401(k) retirement savings.

No matter how much you have saved or whether you plan on retiring at 62, 65, or later, now is the time to either catch up on or further increase your 401(k) retirement savings.

What you do in the next few years with your 401(k) may mean the difference between having enough to get by or having the retirement lifestyle you desire.

Here are a few ways to maximize your 401(k) performance after 60…

- Don’t be too cautious as an investor–being too conservative may create underperformance over time.

- Do whatever you can to maximize annual 401(k) contribution limits.

- Take advantage of the 401(k) catch-up contribution–doing so means you can save an additional $6,000.

- Consider delaying retirement for a few years so you can save more.

- Rebalance your 401(k) account quarterly.

- Avoid target date funds.

- Get third-party advice ASAP.

If you’re behind on retirement savings after 60, check out our 8 mistakes to avoid and tips on what to do instead.

How Third-Party Advice May Help Maximize 401(k) Retirement Savings

You wouldn’t make major health decisions without the advice of a doctor, would you?

So, why would you turn what could be your largest financial asset over to chance?

As 401(k) Maneuver founder Mark Sorensen says, “It doesn’t pass the common sense test, does it?”

However, this is exactly what many Americans are doing.

Many people we speak with think their employers are making changes to their 401(k) for them, which is not the case.

Others have been advised to invest in target date funds (also called lifestyle funds and retirement date funds, or 2020, 2040, 2050 funds) and that a buy-and-hold strategy is best.

There are also people who believe their account balance isn’t big enough or they are too close to retirement to consult an expert–that it’s just not worth the time or effort.

Whatever the reason, they aren’t seeking third-party advice to help them plan and stay on track for retirement . [link to pop up opt in for the financial advisor license download.]

And this inaction may be hindering account balances.

In the age of low-cost robo advisors and financial DIY tools you can access on your smartphone, many people overlook the importance and value of third-party expert advice.

Although you might have basic investment knowledge, utilizing an expert to make the moves that require skill and care may change the performance of your account from good to great.

And potentially boost retirement savings.

In fact, studies continue to show that working with a financial advisor may increase your retirement income and greatly impact the type of retirement lifestyle you can afford.

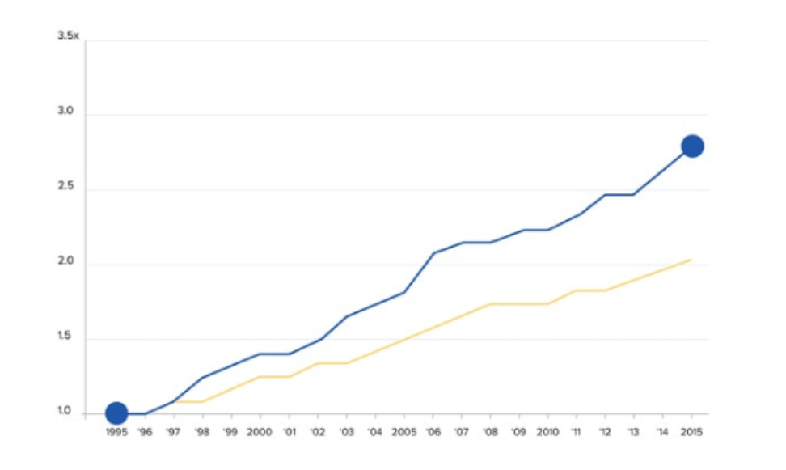

From 2006 to 2012, Aon Hewitt and Financial Engines conducted a study where they compared the returns of investors who sought help in the form of online sources or managed accounts to those who managed their 401(k)s themselves.

The study, which examined the 401(k) investing behavior of 723,000 workers at 14 large U.S. employers, concluded that people who got professional help earned higher median annual returns than those who invested alone.

In fact, “Participants who got Help received, on average, 3.32% (net of fees) more in return annually” than those who managed their own portfolios.⁴

“If two participants—one using Help and one not using Help—both invest $10,000 at age 45, assuming both participants receive the median returns identified in the report, the Help participant could have 79 percent more wealth at age 65 ($58,700) than the Non-Help participant ($32,800).”⁵

Add that up over the years, and 3% higher annual returns just by getting expert help can add up to tens of thousands of dollars you could potentially save.

Wouldn’t you say that’s worth reaching out for help?

In another 2014 report, Morningstar’s Head of Retirement Research, David Blanchett, CFA, CFP, stated that participants who received expert guidance had as much as 40% more income during retirement versus those who received no help at all.⁶

How much would 40% more income impact your retirement lifestyle?

Would it make the difference between taking luxury vacations vs. weekend road trips a few hours away?

Would it allow you to be able to spend more time with the grandkids and friends instead of having to take a part-time job to make ends meet?

We encourage you to sit down and write out the impact an extra $20,000, $50,000, or $100,000 of retirement income would have on your life.

Writing it out is a powerful exercise that can take you from being an apathetic, passive investor to one who is engaged and excited about maximizing your 401(k) retirement savings…no matter your age.

No matter your age or how much you have saved to date, it’s never too late to take control of your financial future!

If you’d like to know How To Supercharge Your 401(k) Performance Today, download our no-cost guide.

Sources:

- https://www.wsj.com/articles/a-generation-of-americans-is-entering-old-age-the-least-prepared-in-decades-1529676033

- https://www.myirionline.org/docs/default-source/default-document-library/iri_babyboomers_whitepaper_2019_final.pdf?sfvrsn=0

- https://www.troweprice.com/corporate/en/press/t–rowe-price–many-parents-short-changing-their-retirement-to-c.html

- https://www.edelmanfinancialengines.com/press/2014/financial-engines-aon-hewitt-find-401k-participants-who-use-professional-help-are-better-off

- https://www.edelmanfinancialengines.com/press/2014/financial-engines-aon-hewitt-find-401k-participants-who-use-professional-help-are-better-off

- David Blanchet, Morningstar Analyst 2014, “The Impact of Expert Guidance on Participant Savings and Investment Behaviors”