What to Do with Your 401(k) Right Now

For an investor, the only thing guaranteed is changing market conditions.

And, we’re seeing a whole lot of it right now.

It’s not only the market that’s volatile – gas prices, utilities, and food costs are putting a serious strain on investors’ pocketbooks. And interest rates are going up.

The current amount of uncertainty naturally creates a high level of anxiety. However, too much focus on the negative can cause irrational decision-making and the potential for regret later on.

That’s why, in this article, we’re sharing 1 thing you can do with your 401(k) right now that may help you better navigate these turbulent times.

The best part – it won’t cost you a cent to do it. Keep reading to find out what to do with your 401(k) right now.

An Antiquated 401(k) Savings Strategy

In the past, investors have been told to follow a “buy and hold” strategy with their 401(k)s: Set up a 401(k), contribute regularly, let it accumulate, and cash it out when you retire.

The problem with this 401(k) savings strategy is that it is potentially costly and may be doing more harm than good.

Here’s why: The investments you initially chose to help you meet your retirement goals – whether that was 25 years ago or 1 year ago – may no longer be the best alternatives for you now.

Especially now with rapidly changing market conditions.

If you’ve followed the “buy and hold” strategy until now, don’t beat yourself up. There is something you can do to possibly ensure you keep more of your hard-earned savings – even in times like we’re experiencing right now.

There are no guarantees. But this one action is critical enough that it has the potential to protect you from more significant losses.

What to Do with Your 401(k) Right Now

It’s as easy as one word: rebalance.

Regularly rebalancing your 401(k) account allocations may be critical to your future retirement income. And it may help you better navigate these volatile times.

Because failing to regularly rebalance your 401(k) portfolio often results in significant losses during bad markets and opens you up to more risk exposure than you initially intended.

Let’s break it down, shall we?

How Rebalancing Works

Rebalancing your account allocations is the process of realigning the weightings of the assets (your investments) in the portfolio.

This can involve periodically buying and/or selling assets in the portfolio in order to maintain the initial desired level of asset allocation.

Let’s say you set up and invested money in your 401(k), and your original asset allocation target was to have 60% in stocks and 40% in bonds.

If you never rebalanced your account and stocks performed far better than the bonds, you’d have much more money invested in stocks. This may increase your asset allocation to 80% of your portfolio in stocks and only 20% in bonds.

While your account may have posted high returns during this period, you are now at a higher risk level than you originally selected.

Continuing with this example and adding in the current market volatility, your retirement savings may potentially suffer major losses, and you might lose some (or a lot) of your hard-earned retirement savings.

In this example, to return to your initial 60/40 target weighting, you would need to sell some of your stocks and purchase more bonds.

However, it’s important to note that rebalancing only the percentages of current holdings does not consider current market and economic conditions.

Be aware that just rebalancing percentages often results in more significant losses during bad markets and missed opportunity for growth during good markets.

Rebalancing Is NOT the Same as Account Allocation

Reallocation is when you change the percentage of invested assets in different asset classes to balance risk versus reward.

Reallocation is about how much risk you want to take.

While they are not the same, the two can be related.

Account allocation is a type of investment strategy that attempts to balance risk versus reward by adjusting the percentage of each asset in a portfolio, based on investment time frame, tolerance to risk, and overall goals and objectives.

In order to help investors grow their accounts, while at the same time keeping risk in check, an asset allocation strategy is often put in place.

Why Rebalancing May Help Protect You from More Loss

If you aren’t rebalancing your account allocations, you may be missing out on earning more and keeping more of your hard-earned retirement savings.

And, as mentioned above, unmanaged allocations may experience much larger losses in down markets and may miss the opportunity for growth during good markets.

This is why a “buy and hold” 401(k) savings strategy may not provide you the retirement results you’re expecting. With this strategy, you aren’t taking into consideration changes in market conditions, tax policy, consumer spending habits, and trade policy.

Things change. So should your investments.

Investments you chose years ago – or even months ago – may no longer be in your best financial interest.

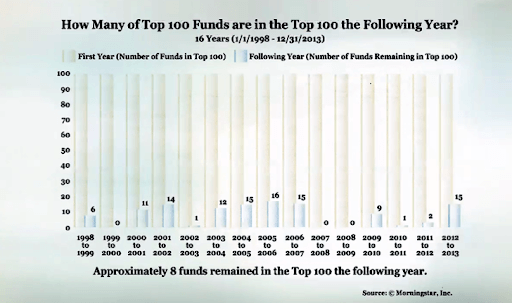

Morningstar conducted a study that monitored the top 100 best-performing mutual funds between January 1, 1998, and December 31, 2013.

This study revealed that, in any given year of top best-performing 100 mutual funds in any of those years, in the next year, about half of the time, 8 out of 100 remained in the top 100 the very next year.¹

Getting Help Rebalancing Your 401(k)

Rebalancing can take time and effort.

This is why, throughout the years, many employer-sponsored retirement plans have touted the benefits of Life Cycle, or target date funds (2020, 2030, 2040 funds).

In fact, many companies resort to these types of funds as the “default” option simply based on a person’s retirement date.

But just because something is easy, it doesn’t mean that it’s the right option for everyone.

In fact, using a “standardized” portfolio allocation can actually be detrimental to investors. Individual investors should ideally have customized solutions that are based on their specific goals and risk tolerance.

Let’s quickly get something out of the way:

How much money you have in your 401(k) should NOT deter you from seeking professional help to rebalance your 401(k).

Nor does it matter how far away from retirement or how close you are.

This is your financial future we’re talking about. If you’re freaking out right now and don’t know what to do or if you don’t have the time or want to learn how to rebalance, get help.

It’s as simple as that.

In fact, studies show that regularly rebalancing your 401(k) with professional advice may significantly improve your 401(k) performance.

In a 2019 study titled Advisor’s Alpha, The Vanguard Fund Group, Inc., reported a 3% average increase in the value of portfolios of clients who work with a good financial advisor.²

Aon Hewitt and Financial Engines conducted a study from 2006 to 2012 comparing the returns of investors who sought help in the form of online sources or managed accounts to those who managed their 401(k)s themselves.

The study examined the 401(k) investing behavior of 723,000 workers at 14 large U.S. employers and showed that people who received professional help earned higher median annual returns than those who invested alone.

“Participants who got Help received, on average, 3.32% (net of fees) more in return annually” than those who managed their own portfolios.³

Check out our 401(k) calculator here to see how you may improve your account performance.

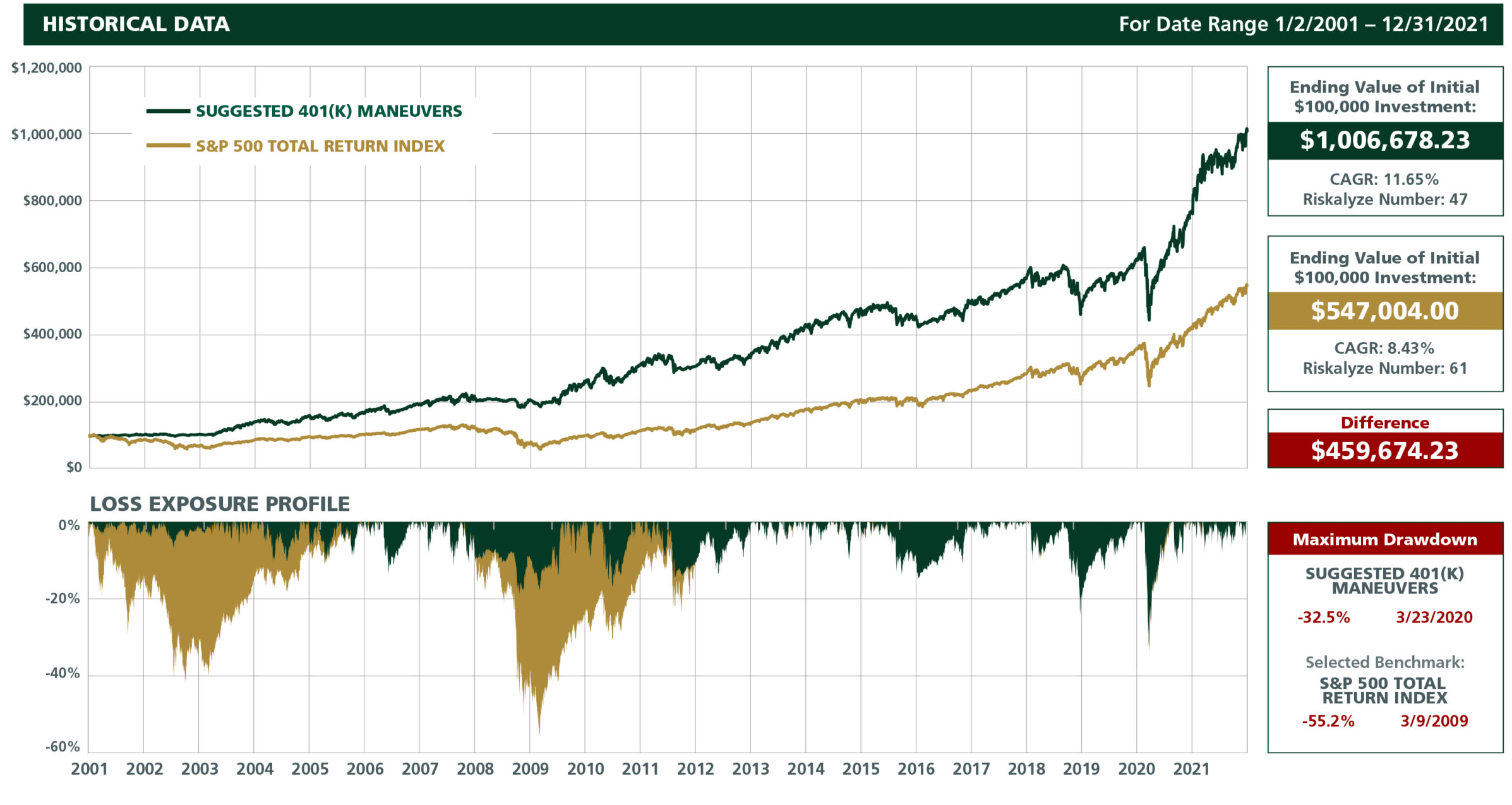

Take a look at the chart below. This 18-year chart illustrates the potential better performance when rebalancing your 401(k) or other workplace retirement accounts with third-party help.

The gold line below represents the hypothetical account allocations using the “buy and hold” philosophy.

The green line represents the potential increase in account performance using third-party help and proper quarterly rebalancing.

To the right of the graph are the ending values of the initial investments of $100,000 shown in the green and gold lines.

The red box to the right shows the potential differences of assets in the account.

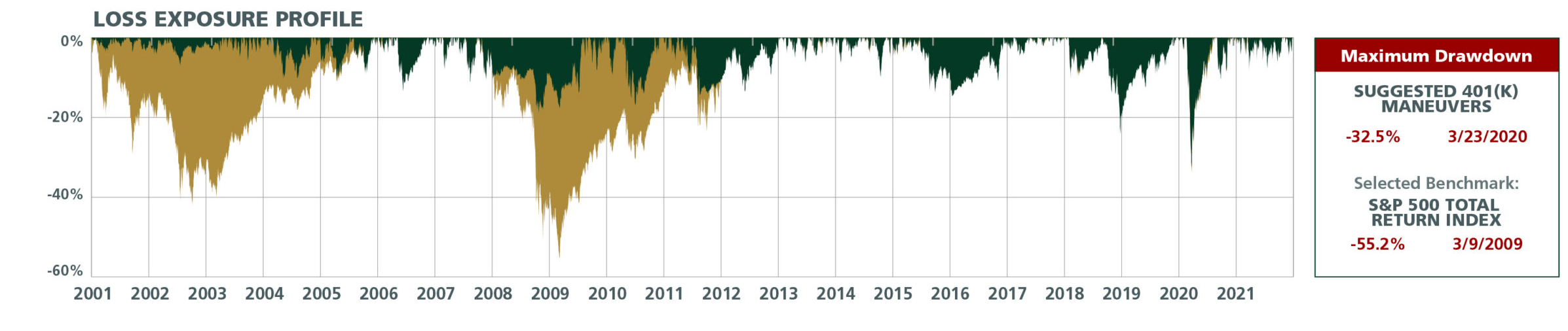

Let’s dive a little deeper, and look at the Loss Exposure Profile. This graph shows how each account would have performed during down markets.

It’s clear that unmanaged allocations experienced much larger losses during these periods.

To the right of the profile is the red box titled Maximum Drawdown. This represents the maximum percentage of loss experienced by each of these accounts – and the day it actually happened.

This shows the difference that third-party help and proper quarterly rebalancing may have.

Remember…

It’s not only important what you earn in return.

It’s also important what you keep that may have a big impact on future account value and your ability to reach your retirement goals.

We’re Here to Help

If you are unsure how to properly rebalance your account or don’t know where to start, we’re here to help.

401(k) Maneuver provides independent, professional account management to help employees, just like you, grow and protect their 401(k) accounts.

Our goal is to increase your account performance over time, manage downside risk to minimize losses, and reduce fees that are hurting your retirement account performance.

We aim to achieve this goal by first looking at how much equity exposure someone has based on current market and economic trends (risk management) and, second, for the equity allocation, our goal is to be in what is working and out of what is not in terms of investment style.

With 401(k) Maneuver, you can go about your life doing what you love with confidence, knowing we are handling the changes for you.

With 401(k) Maneuver, there’s no need for FaceTime meetings. And you don’t even have to move your account – you can keep it right where it is.

Have questions or concerns about your 401(k) performance? Book a complimentary 15-minute 401(k) strategy session with one of our advisors.

Book a 401(k) Strategy Session

Sources:

- The Impact of Expert Guidance on Participant Savings and Investment Behaviors. David Blanchett, Morningstar Investment Management Group, 2014.

- https://www.investopedia.com/articles/personal-finance/102616/how-much-can-advisor-help-your-returns-how-about-3-worth.asp

- https://www.edelmanfinancialengines.com/press/2014/financial-engines-aon-hewitt-find-401k-participants-who-use-professional-help-are-better-off

401(k) Maneuver is another business name for Royal Fund Management, LLC a SEC Registered Investment Adviser.

The Suggested 401(k) Maneuvers data illustrated in the chart on this page is created using back testing. Back testing involves a hypothetical reconstruction, based on past market data, of what the performance of a particular account would have been had the adviser been managing the account using a particular investment strategy. Performance results presented do not represent actual trading using client assets, but were achieved through retroactive application of a strategy that was designed with the benefit of hindsight. Back tested performance results have inherent limitations, particularly the fact that these results do not represent actual trading and may not reflect the impact that material economic and market factors might have placed on the adviser’s decision-making if the adviser were actually managing the client’s money.

These results should not be viewed as indicative of the adviser’s skill and do not reflect the performance results that were achieved by any particular client. During this period, the adviser was not providing advice using this strategy and clients’ results may be materially different. The strategy that gave rise to these back tested performance results is one that the adviser is now using in managing clients’ accounts.

A client’s actual performance could also be materially different as a specific defined contribution plan investment menu may not have the same or similar investment menu options utilized by the adviser during back testing. The limitations of a defined contribution plan’s investment menu could result in materially different performance results.

CAGR is defined as Compound Annual Growth Rate. The Riskalyze Number is a calculation used to define the risk of a portfolio or the risk tolerance of a client compared to market indices. It determines mathematically the potential range of profit or loss with a probability of 95%. There can be no assurance that the portfolio does not lose more than the projected loss of the range of outcomes calculated.

Returns do not reflect the performance of any advisory client and reflects the reinvestment of dividends and capital gains. No current or prospective client should assume that the future performance of any specific investment or strategy will be profitable or equal to past performance levels. All investment strategies have the potential for profit or loss. Changes in investment strategies, contributions or withdrawals, and economic conditions may materially alter the performance of your portfolio. Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment or strategy will be suitable or profitable for a client’s investment portfolio. There are no assurances that a client’s portfolio will match or outperform any particular benchmark. Asset allocation and diversification do not ensure or guarantee better performance and cannot eliminate the risk of investment losses.

Projections are based on assumptions that may not come to pass. There is no guarantee or assurance that the projected or simulated results will be achieved or sustained. Actual results may be better or worse than the simulated scenarios. Trend indicators can shift precipitously in response to global events.

All third-party trademarks, including logos and icons, referenced in this website and our content, are the property of their respective owners. Unless otherwise indicated, the use of third-party trademarks herein does not imply or indicate any relationship, sponsorship, or endorsement between 401(k) Maneuver and the owners of those trademarks. Any reference inside this website or content to third-party trademarks is to identify the corresponding third-party goods and/or services.

Click here for Additional Important Disclosure

https://aon.mediaroom.com/news-releases?item=136959