What Are My Rights as a 401(k) Investor?

It’s important you know your rights as a 401(k) investor.

A 401(k) is one of the largest assets people have, so why leave it to chance?

The sad truth is that too many Americans don’t understand how their 401(k) plan works or why they selected the investment accounts they did.

This is possibly due to the fact that when you sign up for a 401(k) plan, you’re simply given a packet of information filled with industry jargon. Or very little is explained by your plan representative or HR department.

It’s up to you to figure it out.

Couple that with a lack of education, such as defining key terms or showing people how to read their statements and an often unhelpful HR contact, and it’s no wonder people don’t grasp what they are invested in.

If you’re confused about your 401(k), not to worry. Keep reading to understand your rights as a 401(k) investor.

The more you know, the better choices you’ll be able to make for your future and building wealth for retirement.

Your Company Does Not Take Care of Your 401(k) for You

A lot of people we speak with think their employer is taking care of their 401(k) for them.

This is not true. They cannot and will not make changes for you.

It’s your money. It’s your account. It’s up to you to make changes.

Sadly, this belief is disconnecting average investors from their money, and potentially keeping them from maximizing their retirement savings.

You Don’t Always Own Employer Matching Dollars Right Away

Any money you contribute to your 401(k) is always 100% vested, and it’s yours to keep.

Vesting is your legal right to keep what your employer contributes as a company match.

Each employer has its own requirements for vesting.

No matter what, once you become fully vested, the money is yours to keep.

So, should you change jobs after you are fully vested, you don’t have to return part or all of the money your company matched.

Your vesting schedule should be clearly spelled out in the information packet provided when you signed up. If you don’t see it, make sure to ask your plan representative or HR department.

There are three types of vesting schedules:

- Immediate: This means you own your employer contribution as soon as you receive it in your 401(k) account.

- Graded: This means you vest a certain percentage of your employer matching dollars in a set period of time, until you are 100% vested. For example, 20% might be vested after your first year working, 40% vested the second year, etc. By law, employers must vest employees at least 20% at the end of 2 years, and another 20% annually each year thereafter.

This means by the end of year 6 working for your company, you will be 100% vested for the company match.

However, if you leave the company after 4 years and your company has a 6-year vesting schedule, you will own 60% of the amount your employer has contributed if they vested 20% at the end of year 2, 20% year 3, and 20% year 4. - Cliff: Some companies require you to stay employed for a specific amount of time before the money your employer contributed is yours. This is known as cliff vesting. Employers have up to 3 years to vest employees in this type of vesting schedule.

If you were to change jobs after 2 years and your company required you to work for 3 years to vest the entire company match, you would lose that money your company contributed.

Should you decide to leave your job early, depending on the vesting schedule, you might walk away forfeiting your employer matching dollars.

Now you know why it’s vital you understand which type of vesting schedule your company offers.

Knowing this information will help you make smart decisions when it comes to your 401(k).

You Can Contribute up to $19,500 In 2020

There is one way that may ensure you have enough to live on during retirement… contribute the maximum amount in any given year.

The annual contribution limit has been raised to $19,500 for 2020 for employees who participate in 401(k), 403(b), most 457 plans, and the federal government’s Thrift Savings Plan.

For those age 50 and older, the 401(k) catch-up contribution limit will also increase $500–from $6,000 in 2019 to $6,500 in 2020.

This means if you’re 50 or older and need to catch up on retirement savings, you’ll be able to save $26,000 in your 401(k) in 2020.

You Can Roll Over Old 401(k)s

If you have an old 401(k) from a previous employer, or more than one, you can roll them over into your current 401(k) or into an individual retirement account (IRA).

Before you do anything, it’s important to know the irreversible and costly 401(k) rollover mistakes so you avoid unnecessary penalties and taxes.

There are two types of rollovers: direct and indirect.

Direct Rollover: When you transfer your money from one retirement account directly into another. With a direct rollover into your new employer’s 401(k) plan or into your IRA, you never touch the money and no money is withheld for taxes.

Indirect Rollover: When your 401(k) account funds are given to you via check for deposit into a personal account, with the intention of reinvesting those funds into a new retirement account within 60 days or less.

Indirect rollovers come with stipulations and penalties:

- Your company will automatically withhold 20% for income taxes for indirect rollovers, and then send you the remaining funds via check. You must deposit those funds into a new IRA within 60 days; otherwise, you’ll have to pay penalties.

- If you deposit the money into a new IRA within the 60-day grace period, you still have to come up with the 20% that was withheld for taxes.

- In most cases, if you are 59½ and you do an indirect rollover, you will also have to pay a 10% early withdrawal penalty if you go longer than the 60-day period.

- The IRS only allows one indirect rollover in a 12-month period.

- You cannot split the transfer among multiple accounts. The transfer must come from one account and go to another account.

Most financial and tax advisors recommend investors opt for the direct rollover option to avoid withholding taxes and potential penalties.

Rolling over your 401(k) account into an IRA too soon may also be a costly mistake.

If you plan to retire before age 59½, taking money out of an IRA will result in regular income tax on your withdrawals and an additional 10% IRS early withdrawal penalty.

However, if you leave your money inside your 401(k) plan, you may be able to take advantage of the “over 55 rule.”

This rule states that if you are 55 or over in the calendar year you leave your job, you can take penalty-free withdrawals from that employer’s 401(k) plan.

You will still have to pay taxes on the withdrawals, but you’ll avoid paying early withdrawal penalties.

Avoid these 5 irreversible and costly 401(k) rollover mistakes. Download our free guide today.

You Can and Should Regularly Make Changes to Your Investments

Contrary to what some investors believe, a 401(k) plan is not a “set it and forget it” program.

Because of this belief, few people rebalance their 401(k) accounts, and even those who do fail to manage risk through proper asset allocation.

In fact, 80% of 401(k) investors fail to rebalance.¹

Rebalancing only the percentages of current holdings does not consider current market and economic conditions. The stock or mutual fund that you chose last year–or even last quarter–may or may not necessarily still be going in the right direction for you.

Failing to rebalance also often results in more significant losses during bad markets.

With that in mind, properly allocating and rebalancing your retirement account–based on your specific objectives–can be extremely advantageous.

Rebalancing is one of your rights as a 401(k) investor.

We recommend rebalancing your account allocations every quarter, or four times a year.

This will ensure you regularly course correct and stay on track to meet your retirement goals.

Your Employer Can Automatically Enroll You in Target Date Funds

More and more companies’ 401(k) plans use target date funds (i.e., 2020, 2030, 2040 funds) as their default option, or Qualified Default Investment Alternative (QDIA).

They can legally do this thanks to the Pension Protection Act of 2016, which enabled employers to direct plan participants’ assets into a target date fund and not be liable–should the employee not select an investment.

According to the Department of Labor, 97.6% of retirement plans in 2016 had a target date fund as their QDIA.

Marketwatch states, “About 70% of U.S. companies automatically enroll employees into 401(k)-type plans, and more than 86% of these firms now direct people’s money by default into ‘target-date funds’ (TDFs).”²

Average investors are advised to invest in target date, or lifestyle, funds because they are supposed to automatically adjust account allocations throughout life.

If you’re younger and plan to retire in 2060, you’re told to select a 2060 fund. If you’re older and wanting to retire in 2030, you’d select a 2030 target date fund.

Investors are grouped solely based on their expected retirement date.

Target date funds do not take into consideration an investor’s…

- Location

- Profession

- Salary

- Risk tolerance

- Retirement goals and objectives

What target date funds say is that if you are retiring in 2040, you’re just like every other investor planning on retiring that year and, therefore, should have the same investment strategy.

We advise against investing in target date funds because they do not take into consideration changes in economic and market trends or other things that could change, such as tax or trade policy.

They also may not make adjustments for any of these driving factors that affect investment performance.

A recent article indicated that, on average, target date funds invested 75% in common equity, generating average losses of over 30% during the 2008 financial crisis.

Investors planning to retire in 2010 suffered significant losses because 2010 target date funds increased their common equity exposure in 2007.³

The reality is that target date funds will often underperform in good markets and do a poor job of managing downside risk during tough markets.

According to Morningstar analyst Jeffrey Holt in March 2018…

“In the long run, the biggest risk in target-date funds is that they won’t meet investor expectations for avoiding losses.”⁴

Due to the lack of education for investors, many people might not know they have another choice.

The fact is, you do have a choice where you invest your money.

You Can Withdraw Money Early, But It Will Cost You

You must be at least 59½ years old if you want to take distributions from your 401(k) without paying penalties to the IRS.

Ideally, you wouldn’t take a withdrawal until you retire.

If you do withdraw money before 59½ years old, you will have to pay income tax on the amount you withdraw plus a 10% early withdrawal penalty.

Depending on your tax bracket, this can almost cut your withdrawal in half after penalties and taxes.

You’ll need to ask your plan representative or someone in HR to see if your 401(k) plan allows hardship withdrawals. Not all plans offer this option.

If your 401(k) plan allows for hardship withdrawals, here are the criteria you must meet if you want to withdraw early:

- Burial or funeral expenses

- Unexpected medical expenses

- Costs associated with purchasing a new home

- Expenses for repair or damage to your home

- Tuition and educational fees and expenses

- Payment to prevent eviction or foreclosure on your home

Meeting one of the criteria above does not mean you’re exempt from paying penalties.

It’s also important to know that, should you take a hardship withdrawal, you are not allowed to make contributions to your 401(k) plan for 6 months.

You will have to pay income taxes on and have to pay the 10% penalty, unless you meet one of the following early withdrawal penalty exceptions:

- If you are “separated from service.” If you lose or leave your job at age 55 or later and no longer work for the sponsoring employer, you won’t have to pay the 10% penalty from the 401(k) associated with the job you recently left.

- If you become disabled.

- If you withdraw an amount less than is allowable as a medical expense deduction.

- If you are required by a court order to give the money to your divorced spouse, a child, or a dependent.

The above exceptions still require you to pay income tax on the amount withdrawn, just not the 10% penalty.

Your 401(k) Is Protected from Creditors and Bankruptcy

If you are experiencing financial troubles and are considering bankruptcy, don’t cash out your 401(k) plan or take a 401(k) hardship withdrawal.

Why? Because the money in your 401(k) account is protected from creditors and from bankruptcy.

It’s advisable to borrow money rather than paying taxes plus penalties for a hardship withdrawal. Or work out a payment plan with creditors before you tap into your hard-earned retirement savings.

You Must Take Distributions at 70½ to Avoid Penalties

If you’re over 70½ years old, you are required to take the required minimum distributions from your 401(k) plan.

While you can withdraw money anytime, you must withdraw your full required minimum distribution by December 31.

If you do not take the required minimum distributions, you’ll face serious tax penalties of 50% on the amount not withdrawn.

You Have the Right to Independent Advice

Utilizing an expert for help with investing and allocating your 401(k) could change the performance of your account from good to great.

If you think you’re too close to retirement or don’t have enough money saved, don’t let that stop you from seeking third-party advice.

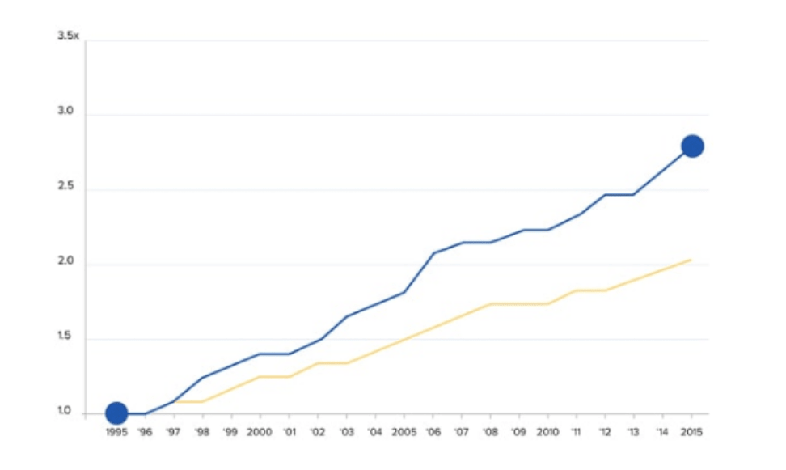

In a 2014 Morningstar report, David Blanchett, CFA, CFP, and Head of Retirement Research, stated that participants that received expert guidance had as much as 40% more income during retirement versus those who received no help at all.⁵

Another 2014 study conducted over a 6-year period compared those who had help with managing their 401(k)s and those who did not.

The report showed that “on average, the median annual returns for participants in the study who got Help were more than 3% 7 (332 basis points, net of fees) higher than people who didn’t get Help.”⁶

Add that up over the years, and 3% 7 higher annual returns just by getting expert help can add up to tens of thousands of dollars you could potentially earn.

Wouldn’t you say that’s worth reaching out for help?

If you’d like more 401(k) tips, download our no-cost guide How to Supercharge Your 401(k) Performance Today.

Sources:

- “Over 90% of Americans make this 401(k) mistake”, Mauri Backman, The Motley Fool

- MarketWatch, Opinion: Target-date funds are more expensive and less effective than this simple investment plan, February 20, 2019

- The Global Financial Crisis and the Performance of Target-Date Funds in the United States – October 1, 2011

- Special Report: Fidelity puts 6 million savers on risky path to retirement, Reuters.com March 5, 2018

- David Blanchet, Morningstar Analyst 2014, “The Impact of Expert Guidance on Participant Savings and Investment Behaviors”

- AON Hewitt “Help in Defined Contribution Plans: 2006 through 2012” Published May 2014

- http://www.aon.mediaroom.com/new-releases?item=136959