5 Things 401(k) Investors Can Do in 3rd Quarter to Maximize Retirement Savings

We’re halfway through the year…a time when many investors wonder what they can do in 3rd quarter to maximize 401(k) retirement savings.

Which makes it a perfect time to review your 401(k) or other workplace retirement plans…and any other savings goals you set for yourself in 2019.

If you’re on target, great! If you’re behind, not to worry.

Keep reading to find out what you can do in 3rd quarter to maximize your 401(k) retirement savings.

#1 See If You Can Contribute More to Your 401(k)

If you’ve had to pause regular 401(k) contributions for any reason in the first 6 months of this year…

If you received a raise…

Or if you finally paid off that credit card or healthcare bill and have more money each month…

Review your budget and see if you can increase your salary deferral percentage by 5 – 10% each paycheck for the rest of 2019.

The more you can save now, the better off you’ll be closer to retirement because your money has longer to work for you.

Even if you only increase your salary deferral by 1% per paycheck, it will make a difference in your income at retirement.

The new contribution limit for employees who participate in 401(k) plans in 2019 is $19,000, up from $18,500 in 2018. And $25,000 for those 50 and older.

Review your budget and see what you can do to maximize your 2019 contribution, or get closer to it than you currently are.

#2 Rebalance Your 401(k)

The next thing you can do in the 3rd quarter to maximize your 401(k) retirement savings is to rebalance your account.

Savvy 401(k) investors rebalance their account allocations every quarter, or four times a year, because they understand it’s not only important what they earn in return, but what they keep that has a big impact on their future account value…

And their ability to have the retirement lifestyle they desire.

They know that the stock or mutual fund they chose last year–or even last quarter–may or may not necessarily still be going in the right direction due to a change in consumer behavior or tax policy changes that could affect a business.

What was hot six month ago may not be as desirable today, and your investments should mirror those changes as best they can.

That said, few people rebalance their 401(k) account.

In fact, 80% of 401(k) investors fail to rebalance.¹

If it’s so important to rebalance each quarter, why do so few investors do it?

In the past, many of us were told that if we’re a traditional investor, we should follow a buy-and-hold strategy with our 401(k) or other workplace retirement accounts.

But a recent Morningstar study shows that, as investors, it may not be wise to be a buy-and-hold type of investor when it comes to your 401(k).²

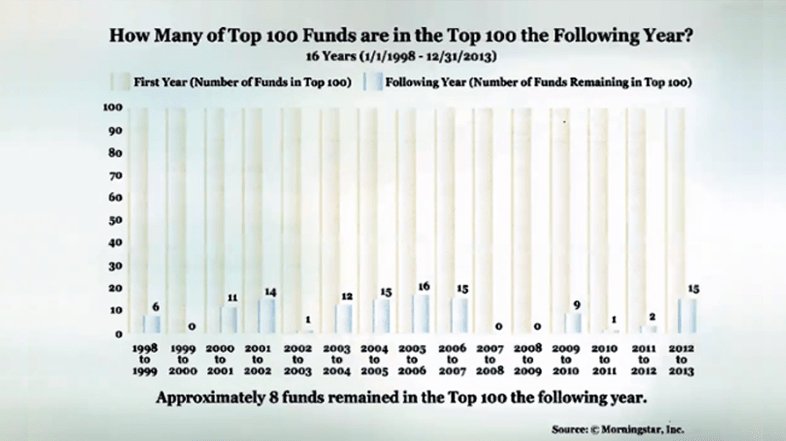

The study monitored the top 100 best-performing mutual funds between January 1, 1998, and December 31, 2013.

It revealed that in any given year of top best-performing 100 mutual funds, in the next year, about ½ of the time, 8 out of 100 remained in the top 100 the very next year!

If you aren’t rebalancing your account allocations, you may be missing out on earning more and keeping more of your hard-earned retirement savings.

Because unmanaged allocations may experience much larger losses in down markets and may miss the opportunity for growth during good markets.

We recommend reaching out to an expert for third-party advice for help with rebalancing because those who do rebalance on their own often fail to manage risk through proper asset allocation.

Discover why account balancing and allocation may affect 401(k) performance. Download your no-cost guide today.

#3 Roll Over Old Workplace 401(k) Plans

If you have changed employers in the last few months and had a 401(k) plan with them, we recommend you roll it over to your current 401(k), if you have one, or to an Individual Retirement Account (IRA) for optimal growth.

Allowing a 401(k) to sit with a previous employer does not mean they are taking care of it for you.

Also, rolling over an old 401(k) into one account will help you better track your investment growth.

Just make sure to choose a plan with the lowest, most manageable fees. Or seek third-party advice to help you make the best rollover decision possible.

Avoid these 5 irreversible and costly 401(k) rollover mistakes. Click here to download your free guide.

#4 Avoid Investing in Target Date Funds

Average investors are told the set-it-and-forget-it strategy is their best option for growing their retirement savings.

Which is why target date funds have risen in popularity over the years. However, according to Rob Arnott, chairman of the board of Research Affiliates, they are “a trillion-dollar industry based on ideas that were never tested.”³

Target date funds, also referred to as lifestyle funds and retirement date funds (you may know them as 2030, 2040, and 2050 funds), are structured to automatically reallocate as you move through different life stages.

So as you age toward retirement, the funds shift toward more conservative investments.

On the surface, target date funds take the pain out of how to choose the right investments for investors. You simply choose a single target date fund, set it, and forget it.

Investing in target date funds and sitting back and not actively managing your retirement account is like saying there’s a one-size-fits-all investment strategy that works for everyone.

This doesn’t mean target date funds aren’t more beneficial for some investors than others.

But for a majority of investors, there can be a downside.

Target date funds fail to take into consideration that not all investors are created equal.

Individual investors are placed into the same asset allocation regardless of their salary and savings history, risk tolerance, past investment performance, lifestyle, and goals.

Secondly, the reality is that target date funds will often underperform, and do not do a good job of managing downside risk during tough markets.

According to Morningstar analyst Jeffrey Holt in March 2018, “In the long run, the biggest risk in target-date funds is that they won’t meet investor expectations for avoiding losses.”⁴

If you are currently in a target date fund, we recommend you rethink this strategy.

Or, at least look inside your fund’s portfolio and make sure the portion of stocks to bonds is at a level you’re comfortable with, and you’re comfortable with the level of risk you’re taking.

If you aren’t sure what you’ve invested in, open up your statement and check, or reach out to your plan representative. In either case, we recommend seeking expert third-party advice on how to best allocate your assets.

Download our guide 5 Ways Target Date Funds Fail to Live Up to Their Promise.

#5 Reach Out to an Expert for Third-Party Advice

One of the best things you can do in the 3rd quarter to maximize your 401(k) retirement savings is to reach out to a third-party expert. Most people have no idea it’s possible to get third-party help.

Although you might have basic investment knowledge, utilizing an expert to do the in-depth market research could change the performance of your account from good to great.

In fact, David Blanchett, Head of Retirement, CFP, CFA of Morningstar reported that participants that received expert guidance had as much as 40% more income during retirement versus those who received no help at all.⁵

Even though your 401(k) is employer-sponsored, it does not mean they’re taking care of your 401(k) for you.

It’s your money. It’s your account. And you’re responsible for your financial future.

If you’re hesitant to reach out for advice because you think your account balance is too small and you need more money saved, don’t let that stop you from getting help!

This is your future we’re talking about.

The sooner you seek expert advice, the higher the probability you’ll be better off in retirement.

We provide private, third-party advice to guide America’s employees on how they may properly rebalance and reallocate their 401(k) investments each and every quarter.

Download our GUIDE How to Supercharge Your 401(k) Performance Today to learn more.

Sources

- “Over 90% of Americans make this 401(k) mistake”, Mauri Backman, The Motley Fool

- Morningstar, 2013

- MarketWatch, Opinion: Target-date funds are more expensive and less effective than this simple investment plan, February 20, 2019

- Special Report: Fidelity puts 6 million savers on risky path to retirement, Reuters.com March 5, 2018

- David Blanchet, Morningstar Analyst 2014, “The Impact of Expert Guidance on Participant Savings and Investment Behaviors”