12 401(k) Retirement Mistakes Investors Make

Whether retirement is right around the corner or years away, there’s no better time than the present to start preparing for it.

According to the Report on the Economic Well-Being of U.S. Households in 2019, featuring Supplemental Data from April 2020, a majority of non-retirees are worried about making retirement mistakes.

The study revealed:

- One-fourth of non-retirees indicated that they have no retirement savings.

- Fewer than 4 in 10 non-retirees felt that their retirement savings are on track.

- Nearly 6 in 10 non-retirees with self-directed retirement savings expressed low levels of comfort about making retirement decisions.¹

According to a 2019 Go Banking Rates survey, “Sixty-four percent of Americans are now expected to retire with less than $10,000 in their retirement savings accounts, versus the 42% reported back in January. Yet, the people at risk of a stormy retirement don’t seem to see it that way — nearly half of all survey respondents were not concerned about the size of their retirement savings accounts.”²

It’s a big mistake to think you are ready to retire simply because you have a retirement account and regularly fund it.

Keep reading for an additional 12 retirement mistakes investors make and what to do instead to ensure you have a comfortable retirement.

#1 Not Having a Plan for Retirement

According to the National Institute on Retirement Security, “A large portion (40 percent) of older Americans rely only on Social Security income in retirement while only a small percentage of older Americans (seven percent) receive income from Social Security, a defined benefit pension, and a defined contribution account. Retirement income from these three sources is widely considered to be the ideal situation to ensure retirement security, particularly for the middle class. Retirees with these three sources of income are far less likely to face poverty and economic hardship.”³

Essentially, if you don’t have a retirement plan, you are probably not going to save enough to retire comfortably.

Some people fail to retire because they don’t think they have enough to even bother with it. Others think it is too late to start saving. And some only plan to let the government take care of them.

No matter your age, you need a plan now so you know exactly how much you need to save to retire comfortably.

Without a plan, this won’t happen.

Or worse, you’ll end up with so little saved that you might have to struggle to survive.

#2 Having a Plan, but Underestimating the Real Expense of Retirement

Unfortunately, one of the most common retirement mistakes people make is underestimating the real expense of their retirement years.

Many retirees expect to continue their same lifestyle, but have not saved enough to maintain it.

Additionally, medical expenses tend to go up during the retirement years.

Healthcare is expected to be one of the largest retirement expenses–with an estimated $285,000 (after tax) in medical expenses needed in retirement for the average couple over 65 in 2019, according to Fidelity Retiree Health Care Cost Estimate.⁴

Many retirees haven’t adequately prepared for the cost of Medicare premiums, deductibles, and out-of-pocket costs or long-term care.

[Related Read: The Real Cost of Retirement: 4 Most Underbudgeted Retirement Expenses]

#3 Not Regularly Reading 401(k) Statements

Some people treat their 401(k) statements like junk mail, tossing them into the trash without even opening them.

This is one of the worst retirement mistakes people make.

They simply hope they have enough saved for retirement in their 401(k), but how will they know if they don’t read it?

When your 401(k) statement arrives, take time to review it.

Opening and reviewing your statements helps you determine whether or not you’re on track to meet your financial goals.

However, understanding your 401(k) statement is more important than simply opening it.

Check out our 2-part video series on how to read and understand your 401(k) statement.

#4 Not Being an Engaged Investor

If you aren’t engaged with your investments, no one else will be. It’s your money. Your accounts. Your financial future.

In other words, don’t set it and forget it.

In addition to reviewing your monthly 401(k) statements, get involved. Educate yourself.

Here are some of the ways to educate yourself and be an engaged investor:

- Continue reading blogs like this.

- Attend seminars and online trainings.

- Read books on the subject.

- Consult a third-party expert.

Being a successful investor isn’t as hard as people assume.

The more people educate themselves and get engaged with their investments, the more confident they feel about their retirement future.

[Related Read: How to Maximize 401(k) Retirement Savings at Any Age]

#5 Not Knowing Your Rights as a 401(k) Investor

When you sign up for a 401(k) plan, you are given a packet of information all written in industry jargon you may not understand.

However, that doesn’t mean you should just ignore it.

Ignoring it is a problem because it prevents you from knowing your rights as an investor.

Think about it. Your 401(k) account is likely one of your largest assets, so it is wise to know your rights as an investor.

For example, many people don’t understand their rights regarding vesting.

Vesting is your legal right to keep what your employer contributes as a company match. Each employer has its own requirements for vesting.

No matter what, once you become fully vested, the money is yours to keep, even if you change jobs.

Knowing your rights regarding vesting schedules may prevent you from missing out on money you are due.

Your vesting schedule should be clearly spelled out in the information packet provided when you signed up. If you don’t see it, make sure to ask your plan representative or HR department.

[Related Read: What Are My Rights as a 401(k) Investor?]

#6 Not Saving the Maximum Contribution Limit

A common question we hear from investors is, “Am I on track for retirement based on my current savings and age?”

According to an Ameritrade Road to Retirement study in 2020, “Most Americans hope to retire by age 67, and more than half have a plan to do so.”

However, the same study reports, “Despite planning, nearly 2/3 of 40 year olds have [less than] $100K saved for retirement.”⁵

With healthcare costs rising and tax rules being unknown in 5, 10, 20 years, investors should do what they can to maximize retirement savings now.

Let’s say you had almost $300,000 average balance at retirement age, and you were making $60,000 per year at your job when you retired. Will this give you the retirement you truly desire?

For most, the answer is No.

That’s why advisors tell clients to contribute the maximum amount in any given year.

Even if you have waited to start saving, contributing the maximum amount to your 401(k) may greatly impact how much you have at retirement.

The annual contribution limit for 2020 is $19,500 for employees who participate in 401(k), 403(b), most 457 plans, and the federal government’s Thrift Savings Plan.

For employees age 50 or older in the plans listed above, the additional contribution limit for 2020 is $6,500. This means the annual contribution limit is $26,000 for those 50 or older.

Look for ways to contribute more than you are now to maximize savings.

Your future self will thank you for it!

[Related Read: Should I Stop or Increase My 401(k) Contributions Right Now?]

#7 Not Putting In Enough to Get the Full Company Match

If you can’t max out the annual contribution, at least put in enough to get the full company match.

Not utilizing the company match is a commonly made retirement mistake.

According to Vanguard’s How America Saves, only 12% of employees with retirement plans at work saved the then-maximum 401(k) contribution limit of $19,000 in 2019.

And only 15% of those 50 or older took advantage of plans offering catch-up contributions.⁶

We cannot stress enough how important it is to contribute at least the minimum of what your company will match.

Because it’s basically like getting free money.

[Related Read: How to Quickly Catch Up on 401(k) Savings]

#8 Relying Only on Target Date Funds

While target date funds have become extremely popular with 401(k) participants in the past few years, it is essential that you diversify your account, and not rely solely on these financial vehicles.

Why?

Because target date funds are based on the date of retirement, they fail to take into consideration that not all investors are created equal.

If you’re younger and plan to retire in 2060, you’re told to select a 2060 fund. If you’re wanting to retire in 2030, you’d select a 2030 target date fund.

What this means is that investors are grouped solely based on their expected retirement date–location, age, profession, salary, risk tolerance, goals, and objectives are NOT taken into consideration.

Because everyone has different goals and objectives for the future, there is no one-size-fits-all way to invest in a 401(k) plan.

In addition, target date funds do not appropriately manage downside risk.

They may often underperform in good markets and do a poor job of managing downside risk during tough markets.

If you are currently in a target date fund, we suggest moving away from this option and better utilizing all the options available in your workplace retirement plan.

Check out our guide 5 Ways Target Date Funds Fail to Live Up to Their Promise.

#9 Not Rebalancing

Contrary to what some investors believe, a 401(k) plan or other workplace retirement plan is not a “set it and forget it” program.

And, just like driving cross-country, if there is a roadblock or other obstacle preventing you from reaching your destination, you need to make the appropriate changes in order to stay on course.

A lot of people we speak with think their employer is taking care of their 401(k) for them.

But it’s not true.

It’s your money. It’s your account. It’s up to you to make changes.

Because of this belief, few people rebalance their 401(k) accounts, and even those who do fail to manage risk through proper asset allocation.

In fact, 80% of 401(k) investors fail to rebalance.⁷

Rebalancing only the percentages of current holdings does not consider current market and economic conditions. The stock or mutual fund that you chose last year–or even last quarter–may or may not necessarily still be going in the right direction for you.

Not rebalancing also often results in more significant losses during bad markets.

With that in mind, properly allocating and rebalancing your retirement account–based on your specific objectives–can be extremely advantageous.

Knowledgeable 401(k) investors rebalance their account allocations every quarter, or four times a year…and we recommend you do the same.

[Related Read: What Every Investor Needs to Know about Rebalancing a 401(k)]

#10 Not Keeping Up to Date with New Legislation

Legislation can and will affect retirement security. That’s why it is critical to stay up to date with legislation.

For example, the SECURE Act, otherwise known as Setting Every Community Up for Retirement Enhancement, passed on December 20, 2019, when it was signed into law by President Trump. It went into effect January 1, 2020.

The SECURE Act aims to make it easier for people to access their retirement savings and avoid running out of money during retirement.

But it also changes how and why you can withdraw retirement savings and transfer money upon death, as well as other changes.

The SECURE Act legislation changes will not affect everyone the same way.

Regardless, it is wise to understand the new legislation, so you can make wise decisions for your retirement strategy.

Check out our guide 10 Ways the SECURE Act Is Changing the Future of Retirement.

#11 Not Rolling Over Old 401(k)s

If you change jobs, don’t assume your previous employer is taking care of you and your 401(k).

This is one of the costliest retirement mistakes people make.

If you leave your 401(k) behind with your past employer, you run the risk of losing out on better retirement savings or facing penalties.

A better option would be to roll your old 401(k) into your new employer’s 401(k) plan, providing it’s allowed, or roll it into an IRA.

[Related Read: Avoid These 4 Irreversible and Costly 401(k) Rollover Mistakes]

#12 Not Seeking Professional Guidance

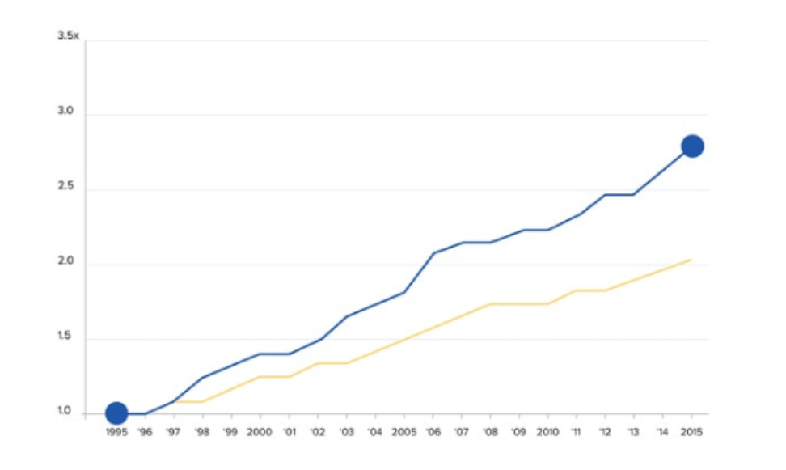

A May 2014 study conducted over a 6-year period compared those who had Help with managing their 401(k) and those who did not. The study revealed…

“On average, the median annual returns for participants in the study who got Help were more than 3% (332 basis points, net of fees) higher than people who didn’t get help.”⁸

From the graph above, you can see getting professional help with your 401(k) or other workplace retirement account can be beneficial to life at retirement.

Think of it this way…You wouldn’t make major health decisions without the advice of a doctor.

So, why turn what could be your largest financial asset over to chance?

If you’d like to take control of your financial future and have more income at retirement, we strongly suggest getting third-party advice.

If you’re hesitant to reach out for advice because you think your account balance isn’t big enough, or you think you’re too close to retirement to get help, don’t let that stop you!

401(k) Maneuver provides professional account management to help you grow and protect your 401(k).

Our goal is to increase your account performance over time, manage downside risk to minimize losses, and reduce fees that harm your account performance.

There are no time-consuming in-person meetings and nothing new to learn, and you don’t have to move your account.

Simply connect your account to our secure platform, and we regularly review and rebalance your account for you, when necessary.

If you have questions about your 401(k) or if you need help, we’re here for you. Click below to book a complimentary 15-minute 401(k) Strategy Session with one of our advisors.

Book a 401(k) Strategy Session

Sources

- https://www.federalreserve.gov/publications/files/2019-report-economic-well-being-us-households-202005.pdf

- https://www.yahoo.com/lifestyle/survey-finds-42-americans-retire-100701878.html

- https://www.nirsonline.org/reports/examining-the-nest-egg/

- https://www.fidelity.com/viewpoints/personal-finance/plan-for-rising-health-care-costs

- https://s2.q4cdn.com/437609071/files/doc_news/research/2020/road-to-retirement-survey.pdf

- https://institutional.vanguard.com/ngiam/assets/pdf/has/how-america-saves-report-2020.pdf

- “Over 90% of Americans make this 401(k) mistake”, Mauri Backman, The Motley Fool

- AON Hewitt “Help in Defined Contribution Plans: 2006 through 2012” Published May 2014